'Old-world' versus the 'new-age’

The ASX 20 has been a consistent underperformer in recent years leading some to conclude that after persistent underperformance, a reversal is due to take place between the ‘big’ end of town, and the ‘smaller’ business that sit outside those largest 20 companies on the ASX.

We’d caution against jumping into such lazy analysis. Looking overseas to the US and the exact opposite have been true. The larger, FAANG stocks (Facebook, Apple, Amazon, Netflix and Google) as they’ve been termed, have all continued to deliver outperformance. It is therefore our view that it's not a case of ‘Big’ vs ‘Small’, rather more an issue of ‘Old-World’ Vs ‘ New-Age’.

It just so happens that the larger businesses in Australia tend to be more mature older style operations, while in the US it is true to the contrary. For that reason, we believe that the recent underperformance of Australia larger capitalisation businesses (ASX 20) is likely to persist in the main for the periods that lay ahead.

Macquarie Research summed it well recently when it stated that the gap between the more innovative corporations and the laggard ‘old-world’ business continues to widen. They compare today's modern era with historical periods of great progression such as those experienced with the emergence of railroads in the 1880’s, and arrival of the Automobile led by Henry Ford in 1920’s.

As eluded to in the same research note, a recent OECD study highlighted the productivity of the top 5% of firms in any industry is now growing 4-5 times faster than it is for these lagging organisations. It is therefore no surprise that in these periods of significant disruption, an increasing proportion of the ‘winnings’ are going to a decreasing proportion of companies.

Investment decisions should be guided by this undeniable trend. We will continue to focus our attention on the those ‘New-age’ sectors that we believe will offer the greatest chances of success.

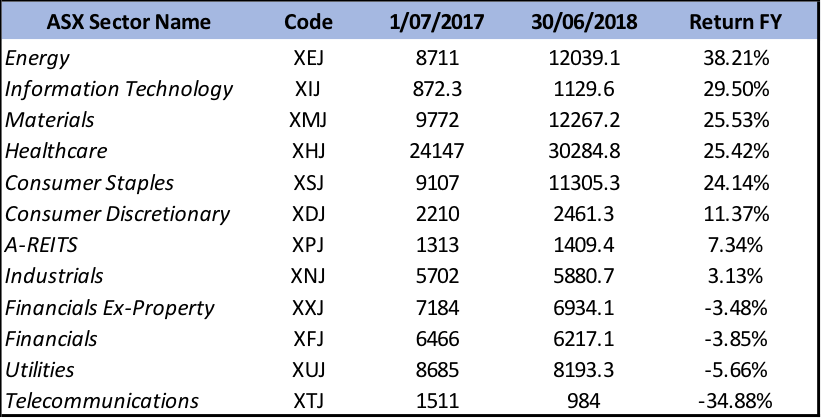

New versus old on the ASX

Looking back at the financial year just past and many of these trends are illustrated amongst the best and worst sector performers.

Amongst the best performers are the cyclical energy and materials sectors who are typically either amongst the best or worst performers each year depending on the underlying commodity prices.

Consumer staples have also had a return to form of the back of resurgent Woolworths and a Wesfarmers ironically being rewarded for ditching their ‘old-world’ business Coles in favour of refocusing on ‘New-Age’ growth prospects.

Once again Healthcare and Information Technology ranked amongst the best performers (Best performers calendar year 2018) for reasons that have time and again been covered across numerous mediums.

The 6th best performing sector for the financial year was the Consumer Discretionary space. Many subconsciously write-off this sector given the perception that it is made up of the traditional clothing and homewares retailers being hit hard by low wage growth, high household indebtedness and increased competition.

There is an element of true to those beliefs with the sector constituents including the likes of Premier Investments and Harvey Norman, however the Consumer Discretionary space is a broad church including many ‘New-age’ disruptors offering compelling growth stories. For instance, it is in this sector that you’ll find:

- Travel disruptors: Webjet (ASX: WEB), Flight Centre (ASX: FLT) and Corporate Travel (ASX: CTD),

- Leading education provider IDP education (ASX: IEL) and

- global gaming wizard Aristocrat Leisure (ASX: ALL).

With that in mind investors still need to be cautious when looking at opportunities in these growth sectors. Investors need to careful not to get caught up in momentum at the expense of earnings, and ensure they continue to look for growth at a reasonable price.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

5 stocks mentioned

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

Expertise

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

Expertise

Comments

Comments

Sign In or Join Free to comment