The phantom resource bear market of 2018

What a difference a year makes. This time last year, the stock market was cheering the global synchronised growth story. Now, it is downbeat, fixated on tariff wars that could derail global growth, especially China. In our view, the tariff war is a sideshow to what is happening in China. The Chinese economy peaked in mid-2017 and since then has been slowing. Global synchronised growth was a false narrative.

Slowing Chinese activity

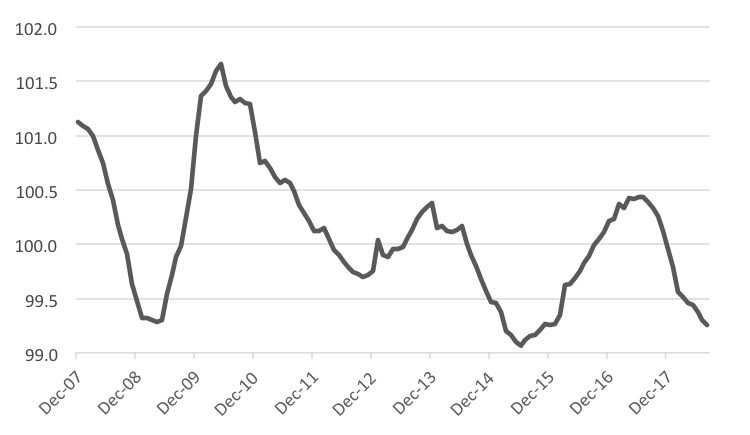

We track more than one hundred data series to get a better pulse of Chinese economic activity. Like the Li Keqiang Index created by The Economist to measure economic activity in China, we have created the Vertium China Index (VCI). Specifically, VCI is a composite index that captures changes in currency and demand deposits, domestic loans, electricity production, rail and water freight, property sales, automobile sales and mobile phone production.

Figure 1. VCI tracks the Chinese economic cycle, including the downturn of 2018

Source: Vertium

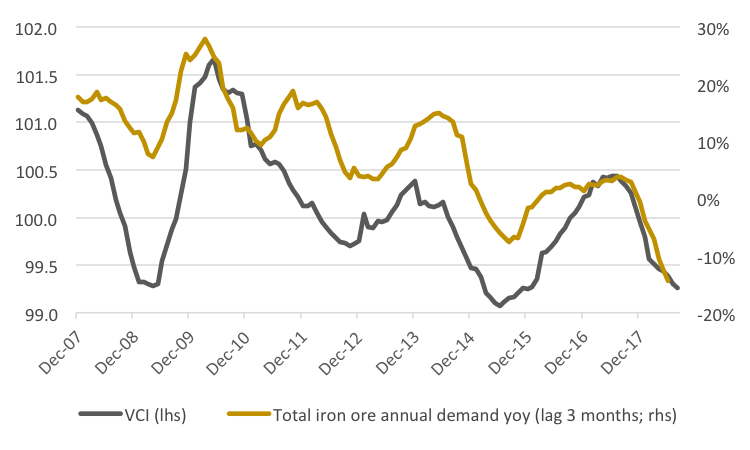

There have been four distinct economic downturns (2009, 2012, 2015 and 2018) in China over the last decade, which had significant impact on the demand for commodities. For example, VCI precedes China’s total iron ore demand (proxied by domestic production and imports) by about 3 months. Currently, the downturn in Chinese activity has resulted in the lowest iron ore demand growth for over a decade.

Figure 2. Chinese iron ore demand is extremely weak in 2018

Source: National Bureau of Statistics, General Administration of Customs, Vertium

One would expect that when Chinese commodity demand is weak resource stocks perform poorly. However, the behaviour of resource stocks in the current downturn is very different to previous cycles. When Chinese activity was close to its lows in 2009, 2012 and 2015 the Australian Resource sector’s rolling annual performances were -31%, -28% and -33% respectively. Contrast those periods to the current slowdown when the resource sector’s annual performance has delivered a perplexing +29%.

Figure 3. Resource sector performance historically followed Chinese economic activity

Source: Iress, Vertium

Is the resource sector about to collapse and catch-up with weak underling Chinese demand? Or is there something else that is driving its performance?

This cycle is different

In 2016, Chinese authorities pushed supply side reform as their main economic policy framework as they were concerned about zombie companies in overcapacity sectors such as coal and steel. The severity of the problem was highlighted by The Economist, which estimated that it would take the Chinese coal and steel industries 91 years and 74 years, respectively, to pay back total debt based on 2015 figures.

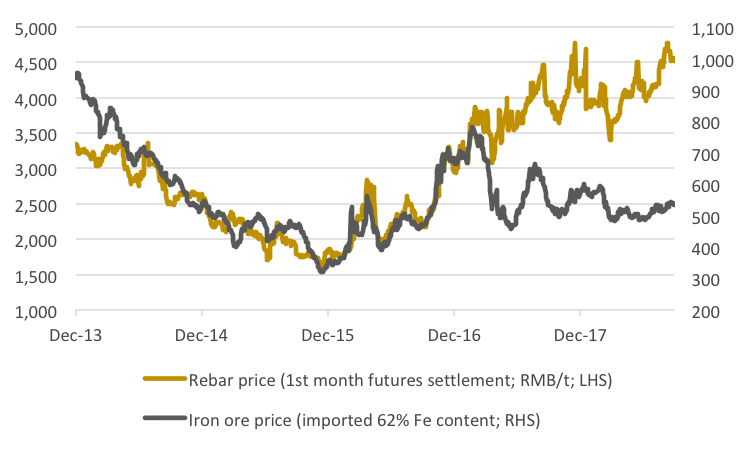

The heart of the supply side reform is reining in corporate debt and authorities aim to reduce State Owned Enterprises (SOEs) ratio of liabilities to assets by 2% over the next couple of years. Combining the supply side reform with China’s ‘war on pollution’ that started a few years earlier, authorities have announced several measures to eliminate excess capacity and deleverage corporate balance sheets. Key industries targeted include steel, coal, coke and cement. For example, about 150 million tonnes of steel was eliminated in China, which reduced global steel supply by about 6%. The enormous cuts to steel supply, combined with environmental policies that encourage the use of scrap metal, has resulted in the steel price decoupling from the iron ore price.

Figure 4. Steel and iron ore prices have decoupled due to supply side reform

Source: Shanghai Futures Exchange, China Iron and Steel Association

Cutting overcapacity allows China to simultaneously achieve their twin objectives of reducing pollution and high levels of corporate debt. Engineering supply cuts in targeted industries, boost commodity prices and allows heavily indebted corporates to de-gear their balance sheets at a faster rate. The process roughly works like this:

- Government orders the entire industry to cut capacity, which reduces pollution

- Commodity price rises (offsetting falling volumes) lead to rising profits

- Profits are used to reduce debt.

- Once debt is manageable, the Government forces larger companies to swallow up smaller peers to drive greater operational efficiencies.

There is no other country in the world that can execute this type of strategy given the Chinese authorities iron grip on their SOEs. Under a free market in an industry with excess capacity, it may take years before supply cuts have a material impact. Under Government direction in China, it happens within months.

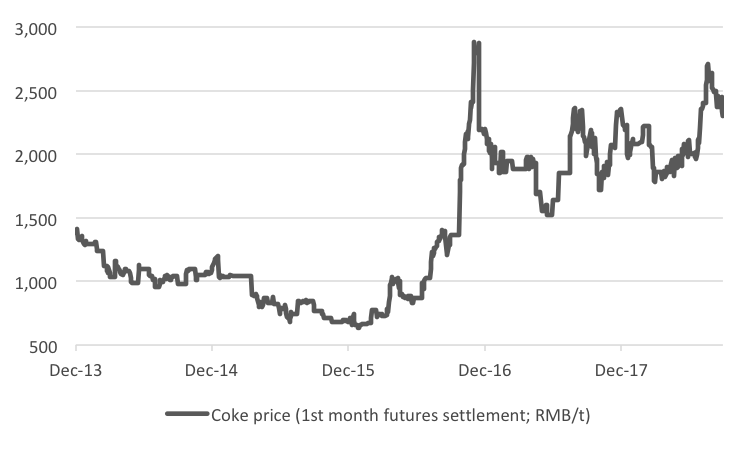

Chinese authorities also understand the very delicate balancing act required to reduce pollution and help SOEs deleverage. Changes in supply for one commodity has multiple consequences across the commodity supply chain. For example, supply cuts in coke (derived from coking coal), an essential ingredient for steel and a significant contributor to carbon emissions, has caused a price spike to record levels. Without supply cuts in steel to engineer high steel prices, profit margins would collapse from high coke costs. Thus, steel companies would be unable to deleverage.

Figure 5. Coke prices are high due to pollution controls

Source: Dalian Commodity Exchange

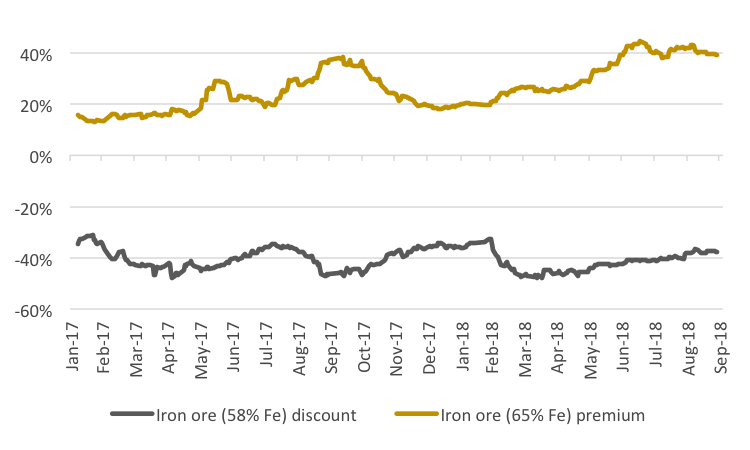

The high price of coke also indirectly affects the demand for different iron ore grades. Coke now makes up around 40% of a steel mill’s costs compared to a typical range of 20-25%. To reduce the consumption of coke in blast furnaces, the demand for high grade iron ore has increased significantly because every 1% increase in iron ore grade reduces coke required by 2%. Hence, since the introduction of supply side reforms, the prices for different iron ore grades has diverged significantly. High grade iron ore (65% Fe content) trades at a significant premium to the benchmark medium grade iron ore (62% Fe content) while low grade iron ore (58% Fe content) trades at a significant discount.

Figure 6. Demand for low grade iron ore is weak due to supply side reform

Source: SteelHome

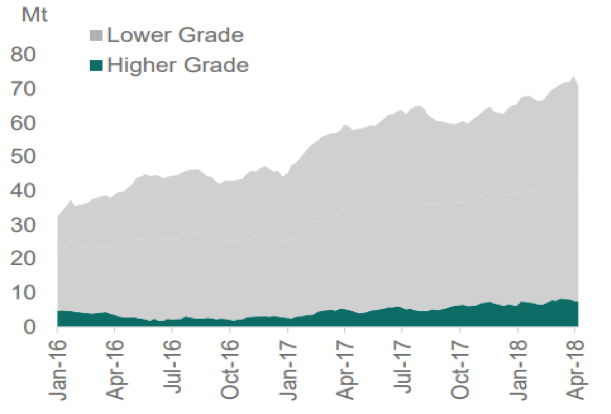

Weak demand for low grade iron ore is also evident in other Chinese data. For example, iron ore port inventories are at record levels because they are predominantly comprised of low-grade iron ore imports.

Figure 7. Chinese iron ore port inventories are at record levels

Source: Vale

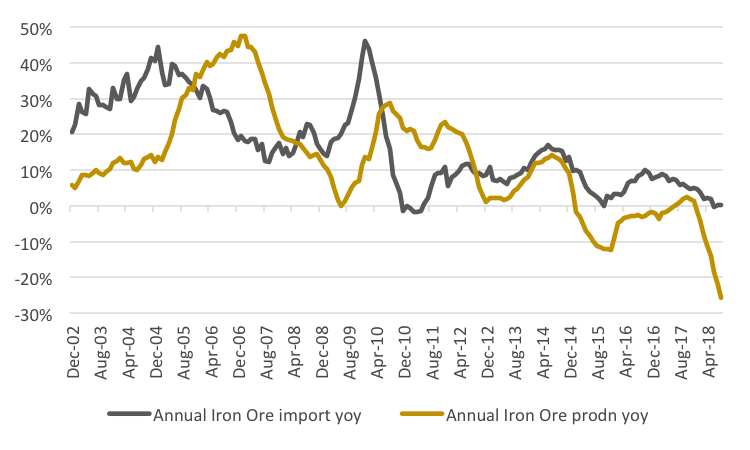

Furthermore, Chinese iron ore is low grade in nature and its annualised production has collapsed 26% to 1.03 billion tonnes. In comparison, iron ore imports, which has a combination of all grades of iron ore, has plateaued at an annualised rate of 1.07 billion tonnes.

Figure 8. Demand for domestic Chinese iron ore has collapsed

Source: National Bureau of Statistics, General Administration of Customs, Vertium

Given that Chinese iron ore accounts for a large portion of global iron ore production and the price of low-grade iron ore is weak, a volume weighted iron ore price on global production highlights a very clear bear market.

Fortescue Metals, a producer of low grade iron ore, has borne the brunt of the iron ore bear market and was one of the worst performing stocks on the ASX over the last year. However, the profits of resource giants, BHP Billiton and Rio Tinto, were saved because the demand for high- and medium-grade iron ore has been more resilient.

Conclusion

There is no doubt that Chinese economic activity is waning, and commodities were due for a bear market in 2018. But with China’s supply-side reform starting a couple of years ago, this turned out to be a phantom bear market for some commodities. If China maintains their supply-side reform, it might pull off the most beautiful deleveraging process in history but with profound ramifications across the commodity spectrum.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Comments

Comments

Sign In or Join Free to comment