The Red Pill or Blue Pill: Navigating the Matrix of Fixed Income

In the film The Matrix, the hero of the story Neo has been unwittingly living in a dreamworld his entire life. He believes what he sees is reality when in fact it is actually a computer simulation. He is eventually given the opportunity to free himself by Morpheus who offers him two pills: a red pill, which will allow him to learn the truth about the Matrix, or a blue pill, which would allow him to stay in his current life and believe whatever he wants to believe. As we all know Neo chooses the red pill and must face the harsh reality of the world.

Past strategies unlikely to work in future

We at Daintree believe this is a fitting analogy to the world of fixed income investing. Fixed income investors have been living in a certain world for a very long time, but that reality has now changed and investors are facing a tough decision: take the blue bill and continue on as if nothing has changed or take the red pill, accept the new normal, and learn to navigate a changed fixed income landscape.

Investors in fixed income products generally fall into two categories. The first group are those that invest in the products because they want some level of income, modest capital return and capital protection. There are a range of products to choose from to target your specific objectives and risk tolerance. The second group are those that buy these products because they believe these assets will perform well when there are corrections in their risk assets (mainly listed equities) which will help to reduce their overall portfolio volatility. This second approach has worked reasonably well for the last 20 years or so, but we believe it is highly unlikely to work as well over the next decade or longer.

Understanding volatility and duration

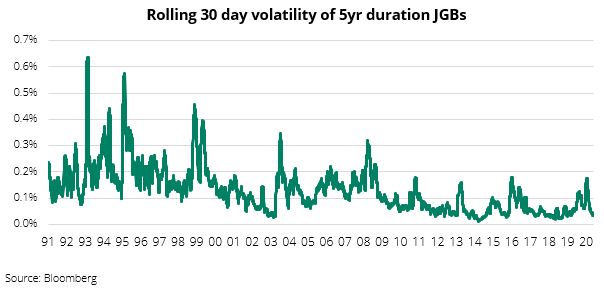

The chart above looks at the volatility of the Japanese government bond (JGB) market. You can clearly see volatility has been steadily declining as the absolute level of yields has remained low and the local central bank has continued to increase its ownership of the market. We believe the US and many developed markets will increasingly look like this over time.

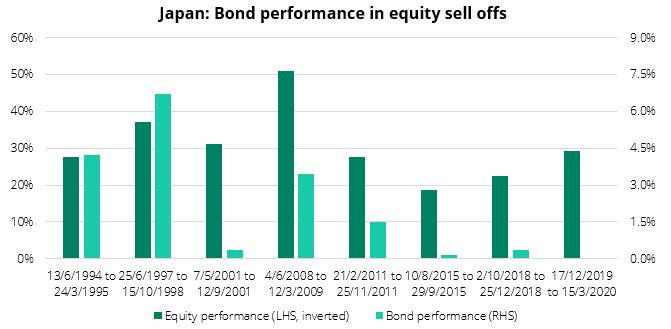

The chart below looks at eight significant corrections in the Japanese equity market over the last 25 years. We have roughly divided them into periods of higher interest rate volatility (pre 2010) and lower interest rate volatility (post 2010). What the chart shows is that in a low volatility world the effectiveness of interest duration to hedge out equity volatility is substantially reduced. In the higher interest rate volatility environment, bonds on average rallied 3.7% when equities sold off 37%, but in the lower rate and volatility periods yields rallied on average only 0.5% while equities sold off 24%.

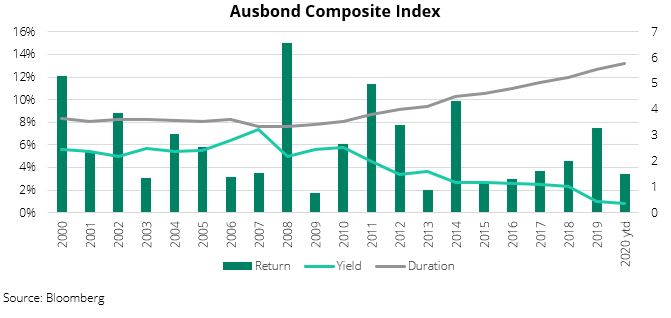

The problem with most places outside of Japan is the future is not going to look like the past. We have moved into an environment of exceptionally low government bond yields and in many cases negative real interest rates. There are some parts of the world where even nominal interest rates have gone slightly negative. Unfortunately, that new reality is likely to be with us for a long time to come. We believe government bond yields around the world have reached, or are very close to reaching, a lower bound. In other words, it is going to be difficult for individual long duration government bonds or funds to generate returns anything like they have in the past. The chart below is a good depiction of the challenges faced by people investing in these products:

This chart looks at the return, yield and duration of the Ausbond Composite Index which is the reference index/benchmark for most long duration fixed income products in Australia. There are three observations to make. Firstly, you can see the average yield on the index has dropped from around 6% in 2010 to around 0.80% today. Secondly, the average duration (or interest rate risk) in the index has increased from 3.5 years to around 6.0 years today, a 71% jump. Lastly, the drop in yields has led to many years of very reasonable performance with the index averaging 5.3% p.a. over the last 10 years. However, the only way that can continue is if bond yields drop another 5-6%, in other words if they drop to below negative 5%.

If you own funds that mirror long duration indices such as this one (regardless of whether the strategy is active or passive) and you have them in your portfolio to hedge out your equity risk, the conclusions are pretty obvious: your future expected returns will be much lower and there is a lot less protection against an equity correction at a much greater cost. It’s sort of like talking to your insurance company about your home insurance, “Well Mr Johnson 10 years ago we could offer you $1m of cover for $1,000 a year but now we can only offer you $200k of cover for $10,000 a year. Have a nice day and thank you for calling.” Clearly a much less attractive proposition.

Some groups are forced to buy government bonds for various reasons. For example, banks and insurance companies are often required to hold highly rated government bonds for liquidity and regulatory purposes. However, in this environment, it is very difficult to understand the argument for holding long duration government bonds in the average investor portfolio unless you are an extremely conservative investor that is happy to accept a negative real return and hold the bonds until maturity. We believe this is a relatively small subset of individual investors.

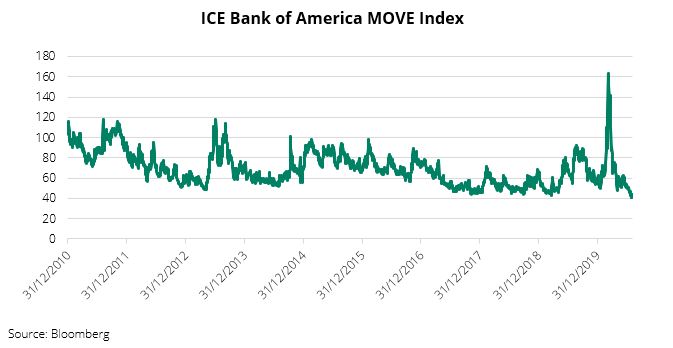

We know some people will say “Yes I know government bond yields are low, but my manager is good at punting duration, so she’ll make up for it that way.” In the past that may have been true, but it is going to be considerably harder to do that in the current environment. The chart below looks at the volatility of interest rate markets.

We can see the volatility of interest rate markets is at historic lows and given the unprecedented volume of purchases being undertaking by the world’s central banks we fully expect this to continue. To make money from trading you need to have volatility. If it is true that we are moving into a low volatility environment for government bond yields, this will represent a significant challenge for anyone trying to make money actively trading these markets or trying to time the market to increase/decrease the duration position of their fund. While passive fund management fees are lower, their performance will struggle just as much as active funds.

The simple 60/40 is facing extinction

The harsh reality of our new investment world is that everyone is going to have to re-examine the tools and strategies they are going to use to try to hedge out the riskier assets in their portfolios. The idea of running a simple 60/40 portfolio and “set and forget” is facing an extinction level event.

So, the logical question then is what CAN we do to hedge out our equity risk. Investors still want the higher returns that equities tend to provide over time but would also like to reduce the risk associated with the allocation. There are several options investors can consider in this environment. However, most of them are much less straightforward and more costly than allocating to simple long duration government bonds, including:

- More dynamic asset allocation – if you can anticipate big corrections in markets with any consistency it might make sense to quickly dial down your equity exposure if you think a large correction is coming

- Safe havens like Gold, Yen, and Swiss Franc- there are some safe haven assets and currencies that tend to perform well when equities are selling off. Unfortunately, the relationships don’t always hold, and you have to get your timing right

- Option/volatility strategies – there are a myriad of option strategies that can be employed each with its own pros and cons, but this approach can allow you to specify exactly how much protection you are likely to get for a given cost

- Short equity positions – a fairly simple approach whereby you either always have a short equity position in your portfolio or it can be something you initiate when you anticipate a meaningful correction

There are also options, such as private unlisted assets that are not marked to market, which have low volatility or relatively low correlations to listed equities. However, those options don’t fully hedge out your equity risk, rather they just reduce your overall portfolio volatility.

One approach we have discussed with a number of our clients is to think about significantly reducing their allocation to long duration government bond fund strategies and reallocating a portion of those funds into a low duration, investment grade credit fund. A portion of the additional income earned by that switch could then be spent on a much more targeted hedging strategy to help protect your equity exposure. A basic actively managed short duration Australian credit fund can easily earn 1-1.5% more than the Ausbond Composite Index without relying on yields moving lower to generate additional returns. This approach would allow you to have a higher expected return and use your “insurance premiums” in a much more effective way than sitting in simple long duration government bond strategies.

Fortunately, none of us live in The Matrix (at least I don’t think we do) so our choices are not as dire as Neo’s but we clearly need to change the way we look at the reality of the new investment landscape. Some of the data we have seen suggests that about 40-50% of the money invested in fixed income products in Australia is invested in traditional longer duration funds (both active and passive). These investors might want to re-evaluate if these types of products still make sense for them in this new low-rate, low volatility world. Hopefully, the red pill is not too bitter for us to swallow.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Mark Mitchell established Daintree Capital in January 2017 and has over twenty years industry experience both in Australia and the USA, specialising in fixed income securities analysis and portfolio management.

Prior to establishing Daintree Capital, Mark was the Head of Credit and Portfolio Manager for over seven years at Kapstream Capital. There, he was ultimately responsible for the development and implementation of the credit research processes and portfolio management until the time he left in October 2015. Over this time, Kapstream grew to over $10bn in assets under management.

Prior to his time at Kapstream, Mark was a Portfolio Manager/Senior Credit Analyst specialising in global credit securities at Colonial First State Global Asset Management between March 2001 and September 2008.

Before moving to Australia, Mark achieved nearly a decade’s work experience in the USA across a range sectors including high yield, bank loans, commodities, futures and listed equities.

Mark holds a Bachelor of Science (Finance) from the DePaul University (Chicago) and is a CFA Charterholder.

........

Please note that these are the views of the writer and not necessarily the views of Daintree. This promotional statement does not take into account your investment objectives, particular needs or financial situation.

Mark Mitchell established Daintree Capital in January 2017 and has over twenty years industry experience both in Australia and the USA, specialising in fixed income securities analysis and portfolio management. Prior to establishing Daintree...

Expertise

Mark Mitchell established Daintree Capital in January 2017 and has over twenty years industry experience both in Australia and the USA, specialising in fixed income securities analysis and portfolio management. Prior to establishing Daintree...

Expertise

Comments

Comments

Sign In or Join Free to comment