The road ahead is ‘U’ shaped

Frank Uhlenbruch

Janus Henderson

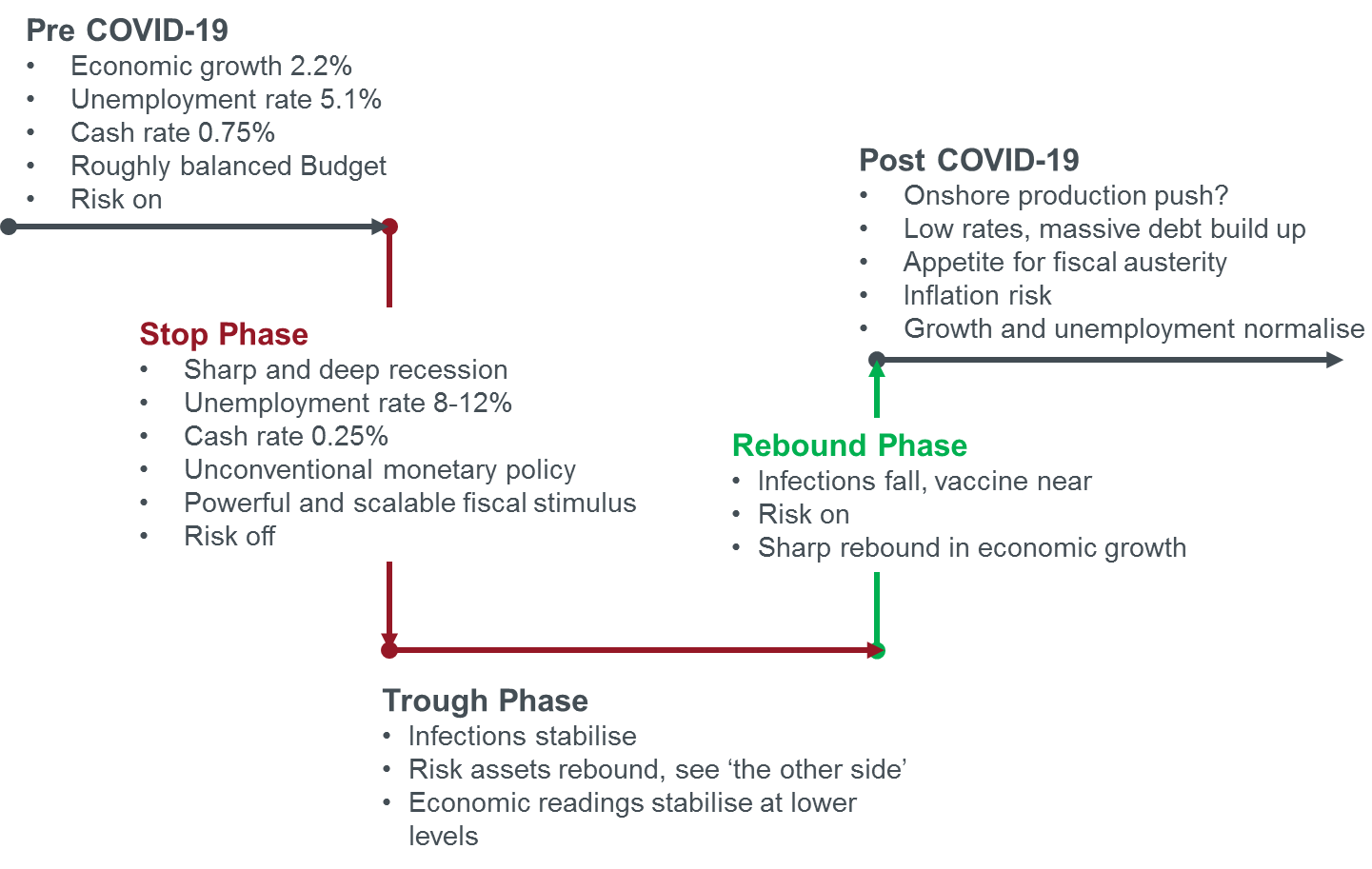

The Australian economy is currently in the ‘stop’ or freefall phase of the ‘U’ depicted in Chart 1 below. Bushfires and the evolution of the COVID-19 pandemic are likely to result in a moderate fall in economic growth in the March quarter.

However, as ‘lockdown’ measures only began to be ramped up during March, expectations are for a massive fall in output over the June quarter as most of the hit to the economy will be taken then. Economic growth could fall by as much as 10% over the first half of the year. A sharp lift in the unemployment rate into the 8% to 12% range appears in store and has elicited a swift, dynamic and powerful fiscal and monetary policy response as policymakers seek to build a bridge to the other side of the U.

It is important to emphasise that this COVID-19 shock is finite and that when we are all allowed to resume our normal lives, activity will begin to normalise. This appears to be happening in China where social mobility measures are being wound back and activity is recovering towards pre-COVID-19 levels.

Chart 1: The Australian economy’s U shaped outlook

Source: Janus Henderson Investors, Australian Bureau of Statistics.

Time spent at the bottom of the ‘U‘ will be a function of how well countries manage the spread of the virus and will test citizens’ and governments’ resolve and societal cohesion.

A range of challenges wait at the other side of the ‘U’. Policy accommodation will have to be unwound at some stage, with little appetite for post-GFC austerity measures. Countries will most likely question supply chain vulnerabilities and there could be a further retreat of globalism. ‘On-shoring’ the production of goods and services, while providing a national security benefit, will result in a decrease in welfare. For debt holders, the blurring of monetary and fiscal policy increases longer term inflation risk.

Stay up to date with our latest insights by clicking the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

1 topic

Frank Uhlenbruch

Janus Henderson

Expertise

Frank Uhlenbruch

Janus Henderson

Expertise

Comments

Comments

Sign In or Join Free to comment