The secret behind resilient performance

Qiao Ma

Cooper Investors

As life slowly returns to normal and businesses around Asia plan for the next phase post Covid-19, we found it a good time to reflect on the learnings over the past eight months.

Observations in 2020 have re-affirmed to us that performance is ultimately driven by management teams’ strategy and execution. We have long stated that we do not allocate capital based on ‘attractive geographies’ or ‘attractive industries’. We invest in the best management teams that we can find, and trust that they will navigate through the thick and thin of their industries. We are pleased to see that nearly all of our 40 portfolio companies gained market share within their own industries over the past few months.

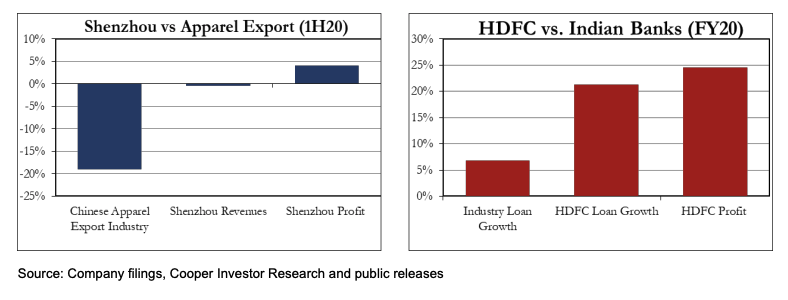

Investors who have followed us for a long time know that the Fund tends to outperform in down markets. This is not due to our allocation into ‘defensive industries’ – 2020 has proven to us that

they do not exist. The relative defensiveness comes from individual portfolio companies outperforming

their own markets and industries, especially during tough times. The charts below illustrate two

examples. There is nothing defensive about Chinese apparel exporters or Indian banks, yet both

Shenzhou and HDFC Bank’s individual performances are far more resilient than their respective

industries.

We are also pleased to see the strong cultures in our portfolio companies shine through and strengthen. Under stress, culture is the secret sauce behind swift actions, fast innovations, and caring for each other. Some of the notable examples of these cultural traits are:

- Never miss a beat on innovations and widened the technology lead (e.g. Tencent and TSMC)

- Sharpen singular focus (e.g., Techtronic, Dabur and Li Ning)

- Protect the long term reputation by putting the well-being of their customers and employees first (e.g., Yum China, Shenzhou and Apollo Hospitals).

Most of our top performing companies are not in the technology industry, yet innovation plays an important role in their recent strong performance nonetheless. Shenzhou and China Mengniu are two examples. Over the past few months, Shenzhou’s new product launches for its main Japanese client, Fast Retailing, fuelled an impressive 26% revenue growth from Japan. Similarly, China Mengniu’s fast shift to local eCommerce where sales force directly sold through Wechat groups helped cushion the blow of offline store closure during February and March. More importantly, fruits from these innovations did not stop as the pandemic passed. Both Shenzhou’s new products and Mengniu’s online initiatives should become sustainable drivers for the years to come. In the end, through the skilful execution of these management teams, even a global pandemic the scale of Covid-19 did little to alter their medium and long term prospects. Both companies are now solidly back on the growth path for the second half of calendar 2020 and beyond.

We continue to find a sweet spot in investing in companies with a quiet, proprietorial management, who operate in traditional and often fragmented industries.

The competitive advantage that comes from being led by a passionate and dedicated founder, who understands the industry and customers deeply, and invests in the long term future via technology and systems, is simply tremendous.

Besides

Shenzhou and China Mengniu, other portfolio companies such as Topsports, New Oriental, Huazhu,

and Yum China also fall into this category. The pattern remains the same – these companies have

already built scale over decades of superior and patient execution, they capitalised on their scale and

capital base during the Covid-19 crisis, deployed capital into the next generation, often proprietorial

technology tailored for their own businesses, and widened the gap further against smaller competitors

who simply cannot afford such systems.

Conclusion

We believe the management types that produce the most attractive investment opportunities in Asia are:

1) Founder-led, where the original founder aligns his/her interest with investors and remains committed to leading the business to bigger successes; or

2) owner operator, where the strong and

unique culture permeates the organisation, and ‘thinking like an owner’ becomes second nature to the

management team.

Invest with Management teams you can trust

At Cooper Investors we look for focused leaders that demonstrate a clear commitment, vision, authenticity, energy, passion and competency for the business/industry. Click the 'CONTACT' button below to find out more.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Qiao Ma joined CI in July 2017. Prior to this, she spent seven years investing in the technology and consumers sectors in Asia and the US. Most recently she was the Head of Asia for Jericho Capital, a multi-billion dollar global investment fund

Qiao Ma

Portfolio Manager

Cooper Investors

Qiao Ma joined CI in July 2017. Prior to this, she spent seven years investing in the technology and consumers sectors in Asia and the US. Most recently she was the Head of Asia for Jericho Capital, a multi-billion dollar global investment fund

Expertise

Qiao Ma

Portfolio Manager

Cooper Investors

Qiao Ma joined CI in July 2017. Prior to this, she spent seven years investing in the technology and consumers sectors in Asia and the US. Most recently she was the Head of Asia for Jericho Capital, a multi-billion dollar global investment fund

Expertise

Comments

Comments

Sign In or Join Free to comment