The slippery slope of forecasting oil prices

Group think is dangerous. At the major turning points in markets the majority view is often an incorrect one. Both WTI and Brent crude prices have declined dramatically in the last few months despite the near consensus view that they should rally. The common view that oil should shortly trade above $70 per barrel led us to an examination of global supply and demand dynamics.

Global consumption has increased by around 10.8% over the last decade. The 34 OECD countries have, collectively, seen a fall in consumption of 8.8% over this period. Slow growth, ageing and stagnant populations, the rise of alternative fuels and increasing energy efficiency are cited as reasons for the decline. Non-OECD countries have witnessed growth of just over 40% through the course of the decade, such that in 2014 non-OECD countries out-consumed the OECD group for the first time in recorded history. Recent evidence suggests that economic growth in the emerging markets has declined, which may prevent strong growth in global consumption in the coming years.

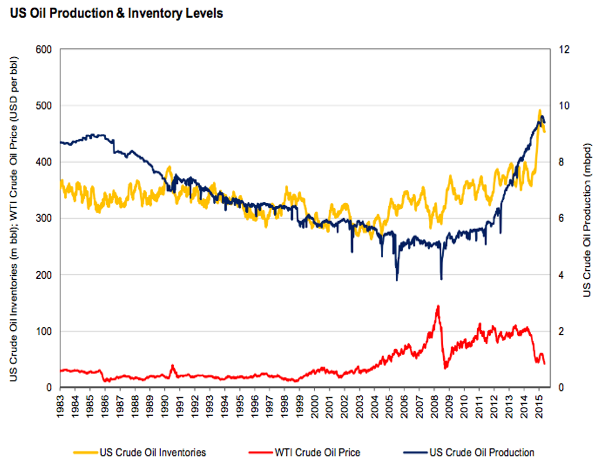

Global production growth has slightly outpaced global demand, with growth of 11.6% over the decade. The increase in US oil production has been remarkable, with a 60% increase in supply over the last ten years. This compares to an increase in OPEC supply of just 8.6%.

For demand and supply to fall back into balance in the short term, we need to see a fall in production. For any fall in supply to be meaningful enough to stabilise prices, it most probably needs to come from OPEC or the US. As it currently stands, OPEC appears focused on increasing, not reducing, their output. Meaningful near term rebalance will most probably require a fall in US crude production. Theory suggests that a recently declining oil rig count would lead to a decline in production, however history suggests that the rig count is not always a reliable indicator of future production levels. In the early 1980’s the rig count peaked in 1982; only for production to peak in 1985.

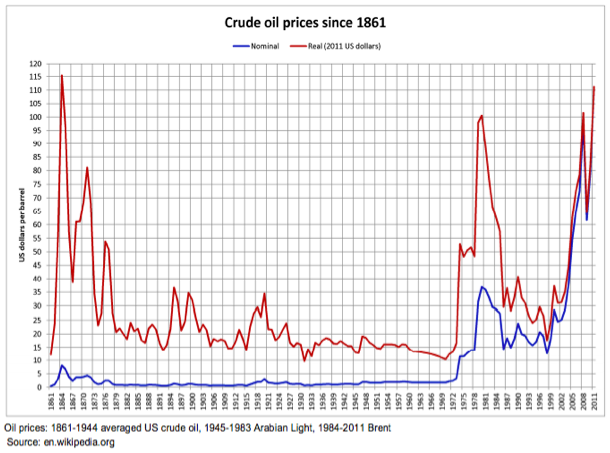

The increase in oil production in the US is not being matched by increasing US consumption. US crude oil inventories have been rising rapidly over recent years. History suggests that sensible long-term price assumptions may well be lower than current spot prices. In fact, analysing 150 years of data suggests that current prices, in inflation adjusted terms, are still above the historical price range.

The danger of group think is obvious often only in hindsight, anticipation of materially higher oil prices in the near to medium term does not seem supported by the evidence. We find that independent assessment of the facts reduces the risk that our cognitive biases and tendency toward group think will lead us into making erroneous investment decisions. To access the full newsletter and accompanying charts, please click the (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Auscap Asset Management is a value based, active Australian equities investment manager established in 2012. Auscap Asset Management is the Responsible Entity and Investment Manager for the Auscap High Conviction Australian Equities Fund and Auscap Ex-20 Australian Equities Fund. The Funds target solid risk-adjusted returns, looking to invest in companies that generate strong cash flows and are trading at attractive prices.

1 topic

Auscap Asset Management

Auscap Asset Management is a value based, active Australian equities investment manager established in 2012. Auscap Asset Management is the Responsible Entity and Investment Manager for the Auscap High Conviction Australian Equities Fund and...

Expertise

Auscap Asset Management

Auscap Asset Management is a value based, active Australian equities investment manager established in 2012. Auscap Asset Management is the Responsible Entity and Investment Manager for the Auscap High Conviction Australian Equities Fund and...

Expertise

Comments

Comments

Sign In or Join Free to comment