The Small Ords has surged 10% over the past 3 months… so what’s driving it?

The S&P/ASX Small Ordinaries Index (ASX Small Ords) has surged by over 10% in the last 3 months on a seemingly new upward trajectory despite what was a fairly mixed reporting season. For the month of October alone, the Index delivered a gain of 6.0%.

While the return looks impressive, closer analysis shows that this 3-month surge in the Small Ords has been led mainly by concept and momentum stocks, it has been based on a rather narrow foundation. Leading the charge upwards has been the small cap Resource sector, several technology stocks and ‘soft commodity’ plays with exposure to China – what we would like to refer to as ‘concept ‘stocks.

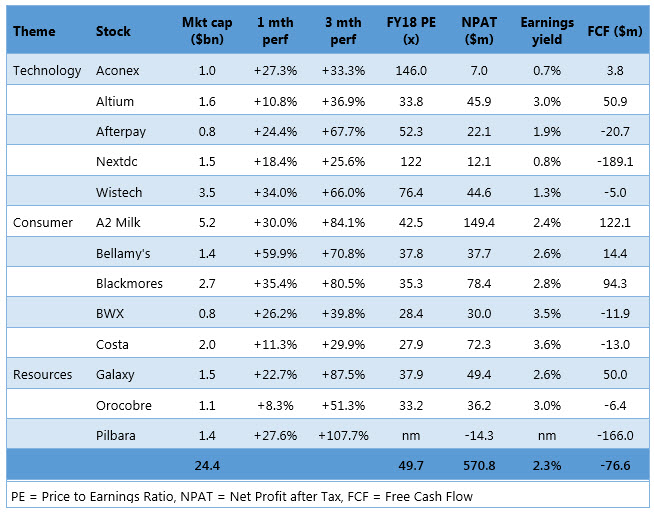

Table 1 highlights the valuations, free cash flow produced as well as these ‘concept’ stocks’ contribution to the Small Ords performance over the last three months.

Table 1: Recent key movers on the S&P/ASX Small Ordinaries Index (Small Ords)

Based on share prices at 31 October 2017

Based on share prices at 31 October 2017

Some interesting facts that are evident from the table above:

- The grouping of stocks above drove over half the performance of the Index over the last 3 months. While the ASX Small Ords was up 10.3% for the three months to 31 October 2017, these 13 stocks accounted for over half of that return

- This group accounts for $24.4 billion of market capitalisation. This market cap is expected to generate an aggregate of $571 million of reported profit in FY18e - on average a PE of over 40 x forecast 2018 earnings and a forecast dividend yield of 1%.

- In addition, these companies whose market value in total is $24.4 billion are expected to generate an aggregate Free Cash Flow of MINUS $76.6m or a free cash yield of MINUS 0.3%.

What does this mean for the rest of the market and for prudent long term investors?

It appears that in the current market, fundamentals have taken a back seat to momentum, unbounded optimism and the fear of missing out on the next big thing.

On the other hand, quality well established quality companies that may have any sort of short-term earnings concerns are being sold down regardless of value. While this is creating great opportunities to buy quality stocks at very attractive prices, it is hurting the performance of fundamentally based portfolios such as IML’s, particularly given our distinct preference for stocks that meet our quality and value criteria as opposed to concept type stocks.

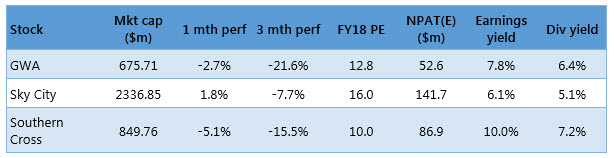

In the table below are examples of long established, good quality companies and their fundamentals. The share prices of these companies have actually gone backwards in the last 3 months while many of the ‘concept’ stocks surged forward:

Based on share prices at 31 October 2017

Based on share prices at 31 October 2017

At IML, we believe it is essential for investors to remain focussed on the long term and not to get caught up the latest market fad – particularly at times like this, when clearly momentum and optimism has taken hold of some sections of the Australian sharemarket.

We continue to be true to our investment philosophy of holding quality stocks trading at attractive valuations and continue to focus on investing in companies that demonstrate strong competitive advantage, recurring revenues, with long term growing earnings and that are trading at reasonable prices. This is the way IML has delivered consistent investment returns for our investors since our inception in 1998 and how we plan to do this over the longer term going forward.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Investors Mutual Limited (IML) is a specialist Australian equities fund manager and was established in May 1998 by Anton Tagliaferro. Based in Sydney, the IML team applies a conservative value-based investment style with a long-term focus.

Investors Mutual Limited (IML) is a specialist Australian equities fund manager and was established in May 1998 by Anton Tagliaferro. Based in Sydney, the IML team applies a conservative value-based investment style with a long-term focus.

Expertise

Investors Mutual Limited (IML) is a specialist Australian equities fund manager and was established in May 1998 by Anton Tagliaferro. Based in Sydney, the IML team applies a conservative value-based investment style with a long-term focus.

Expertise

Comments

Comments

Sign In or Join Free to comment