Three Lessons from the First NPL Securitisations in China

Two non-performing loan (NPL) securitisations totalling CN¥534 million have just been completed in China. These should be the first of many as part of a CN¥50 billion program. The idea of NPL securitisations has been rubbished by some, but based on the results of the first two sales the process has merit in helping clean up the bad loans made by Chinese banks. Whilst the sample size is small, there’s three key lessons that can be drawn from the process so far.

The process works

The most important part of the NPL securitisation process is to break up, price and transfer the risk of non-performing loans. The first two securitisations did exactly this. Loans were marked-down significantly, transferred into a structure with tranches sold to a range of buyers.

By marking down the loans the selling banks were forced to realise losses. On their balance sheets, the book value of their assets and equity was reduced by the amount of the mark-down. Whilst the initial securitisations were very small, they have laid out the pathway for proper asset valuations and greater transparency for Chinese banks. Two banks have taken losses and gotten rid of some of their NPLs, others can now do the same.

The number of buyers is not known, only that they were all Chinese banks and asset managers. The Chinese banks are interested in the senior tranches which were given a AAA rating by the Chinese rating agencies. The asset managers, which could be more aptly described as restructuring managers, are interested in the junior tranches. Whilst it is not clear whether the buyers got a bargain in this process, the loan mark-downs were steep so there’s a reasonable chance of a profit for the buyers.

There is a legitimate question whether the buyers did sufficient due diligence and bought willingly, or whether they were coerced. It’s also difficult to know how deep is the appetite for buying more of these deals. We’ll find out over time more on those two questions as more deals are brought to market.

Recovery rates could be awful in China

In western countries recoveries on senior secured lending averages 50-80%. Recovery rates typically fall in times of crisis, particularly when there is significant excess capacity. Notable examples of poor recovery rates include property in Ireland and Spain after the financial crisis and the US oil and gas sector in the last year, where recoveries of single digit cents on the dollar are not uncommon. In the Bank of China securitisation, the loans were marked down to 24% before being transferred into the structure. This is an awful recovery rate for bank lending and if it is indicative of Chinese NPLs it has huge ramifications for Chinese lenders and the various levels of Chinese governments.

It should be noted that the loans came from the province of Shandong, which is a major steel producing region. Steel is one of the industries known to have the greatest overcapacity issues and thus recoveries on these loans from Shandong might be lower than would generally be expected. Without substantial additional details, it is difficult to form a view whether this small sample is representative of what wider recovery rates will be.

Government capital will be needed to recapitalise the banks

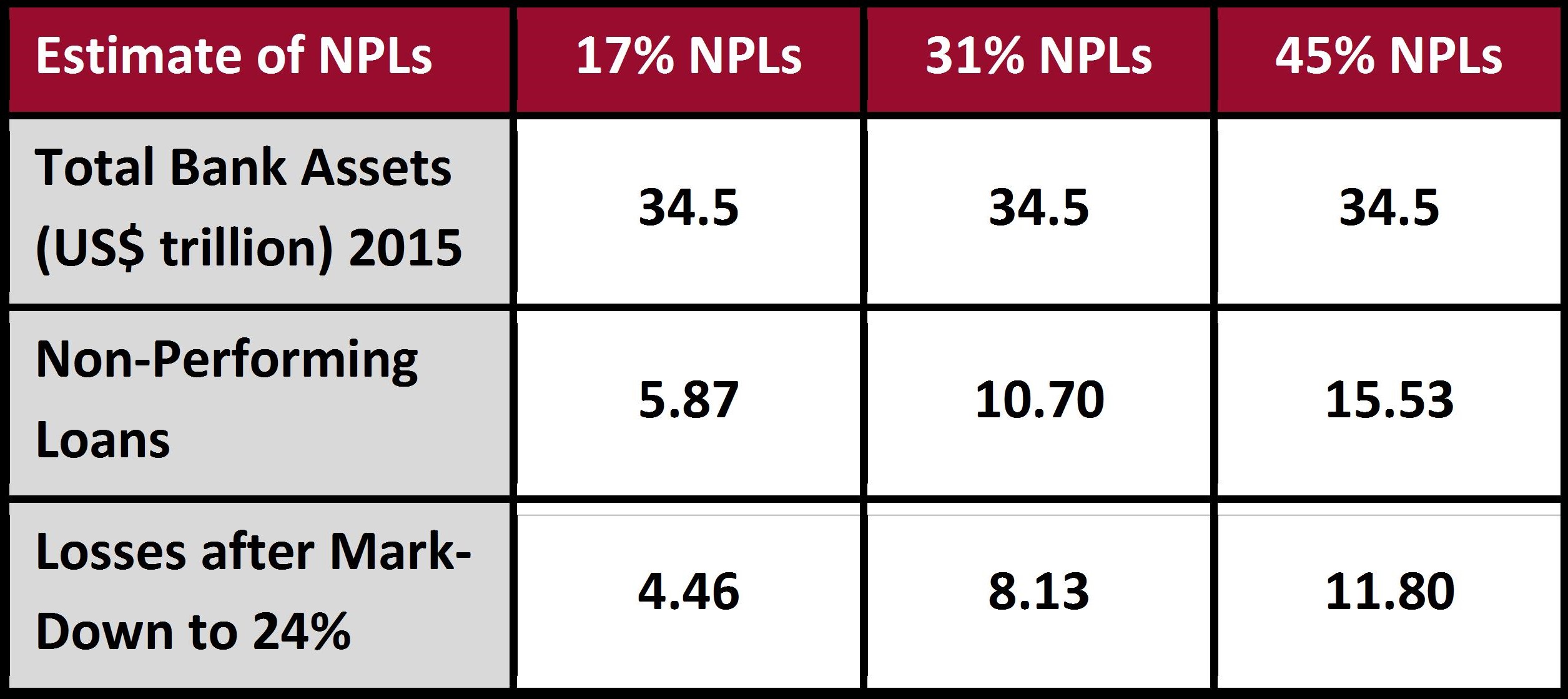

Official figures for March have Chinese NPLs at US$211 billion, which is 0.61% of total bank assets. Applying a recovery rate of 24% would see losses of US$156 billion. Outside of China no one believes the official data, with many estimating that NPLs are around 20% of loans. There’s three recent studies that help with estimating how big the NPL problem is.

Firstly, Natixis found that 17% of Chinese companies have an EBITDA to interest ratio of less than 1. Remember that you can’t pay interest with EBITDA; operating cashflow or EBIT is a more appropriate measure. Secondly, Macquarie found that 23% of bonds were issued by companies that don’t generate enough operating profit to cover their interest. Thirdly, Hua Chuang Securities found that 45% of new company debt is raised to pay interest on existing debt. Companies borrowing just to pay interest on existing debt are sometimes referred to as Ponzi companies. The table below uses 17% and 45% as the bookends, with an average of the two used as a mid-case scenario.

Regardless of which case is picked, the losses are estimated to be enormous and will overwhelm the US$2.6 trillion of core equity at Chinese banks. That leaves the Chinese government with the tricky situation of deciding whether to bailout their banking system. Japan has shown that not dealing with the problems of overcapacity and NPLs can lead to a decades long stretch of virtually no growth. Ireland showed that bailing out banks comes at the price of a huge increase in government debt levels, but GDP growth returned in 2011.

Conclusion

The good news for China is that the first NPL securitisations demonstrated that the process works with losses taken and the risk of the assets largely transferred away from the selling banks. The bad news was the mark-down to 24% of face value on the debt sold, which points to Chinese NPLs being particularly toxic. If that level is used as indicative of future recoveries, recent data points to US$4.46 to $11.8 trillion of losses, which will massively overwhelm current banking system core equity of US$2.6 trillion. The Chinese government is now left to decide whether it will force banks to purge their NPLs with government funds injected to recapitalise the banks like Ireland, or whether the NPLs will be left to fester as was the case with Japan.

Written by Jonathan Rochford for Narrow Road Capital on June 13, 2016. Comments and criticisms are welcomed and can be sent to info@narrowroadcapital.com

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

1 topic

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment