To hedge or not to hedge? That is the question.

To hedge or not to hedge international equities has been a perennial question for Australian investors for decades, with conventional wisdom dictating that hedging against foreign currency moves is good risk management and reduces volatility.

However, Credit Suisse Private Bank’s analysis over the last 20 years reveals that for Australian investors, whose portfolio value is calculated in Australian Dollars (AUD), hedging international equities may have a detrimental outcome, adding to volatility without improving returns.

Why is this the case? It is because of the pro cyclical behavior of the Australian economy and the AUD. Being a commodities focused economy, the AUD moves up and down with the price of commodities. Strong global growth, which of late has been led by China and the US, translates into higher demand for raw materials. When demand for commodities is strong, the Australian economy is generally stronger, and so is the AUD. Conversely, when the global economy is weak, demand for manufactured goods and commodities is also weak and so puts downward pressure on the AUD.

How this translates into stock market prices is interesting. When global growth is weak, stock markets tend to be weak as well, but we also know that under this scenario the AUD tends to depreciate against foreign currencies. If for example US shares are falling, the AUD is falling at the same time. Thus when the value of those US shares is translated back into AUD, the loss in value is smaller. The movement in the AUD/USD acts as a buffer for returns.

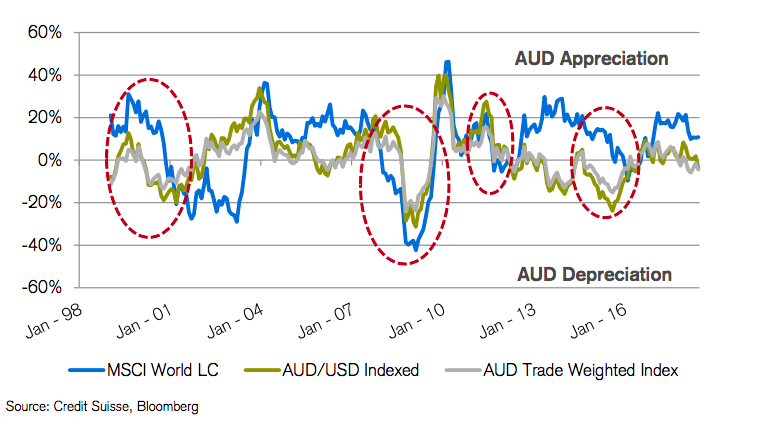

Statistically speaking, our mapping of the relationship between global stock markets and the AUD shows a positive correlation – they move in the same direction more often than not. This relationship is shown in the following graph. The dotted red circles highlight those periods when the MSCI World Index suffered its biggest falls. You will note the depreciation in the AUD/USD and AUD Trade Weighted Index (TWI) that occurs concurrent with each correction.

The conclusion is that not hedging FX on international shares over the long term will reduce volatility.

However, when we turn to the bond market and ask the same question – should Australian investors hedge FX risk on foreign currency denominated bonds? The answer is the opposite – yes, they should.

Analysis of the same 20 year data set, shows a reverse relationship between the AUD/USD and the direction of bond prices. The AUD generally appreciates with weak bond prices, which is usually concurrent with stock market strength. If international currency bonds aren’t hedged to AUD, the bond price fall is exaggerated when translated to AUD. In a low bond yield environment, the move in the currency can completely offset the yield from bonds, driving bond returns into negative territory. On the other hand, if bond prices are rising, as investors seek certainty in a volatile market for global growth, the AUD is likely to be depreciating, exaggerating the return on the upside.

Although this is a positive during an uncertain environment – such as the present - we need to consider the overall risk return characteristics created by an unhedged position. The point to note here is that bonds are in a portfolio to provide income and portfolio stability. In a fully unhedged position, the bond returns, and stability of those returns, may be overwhelmed by the movement in the currency. This changes the risk profile of a bond allocation from one of stability to one that resembles a more volatile risk asset, which is undesirable from an overall portfolio perspective.

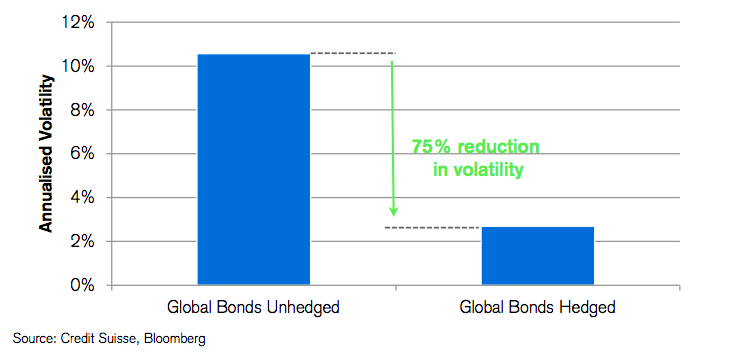

We graphed the impact on volatility of hedging global bonds to AUD, the reduction in volatility is dramatic.

The alternative to hedged foreign bonds is to own AUD bonds. In fact, we recommend to our Australian clients to have a bond portfolio dominated by AUD bonds. The yield on AUD bonds is generally higher than other developed markets, and provides a stable flow of AUD income. It also provides a more direct counter weight to volatility in Australian biased equity portfolios. But to be clear, investors can add value by hedging or not hedging at particular times, they just have to get it right, and need to be aware that picking short term foreign currency moves is notoriously difficult. An Australian investor that wants insurance against weaker global growth and a falling AUD, may consider holding unhedged US Treasuries now for instance.

Our overall conclusion is the starting point for long term investors who expect to stay invested through the cycle, should be not to hedge international equities, but do hedge foreign currency bonds.

Disclaimer

The information and opinion expressed in this report were produced by Credit Suisse as of the date of writing and are subject to change without notice. The report is published solely for information purposes and does not constitute an offer or an invitation by, or on behalf of, Credit Suisse to buy or sell any securities or related financial instruments or to participate in any particular trading strategy in any jurisdiction. Information pertaining to price, weighting, etc. of particular securities is subject to change at any time. While Credit Suisse has made every effort to ensure that the information contained in this document is correct as at the time of publication, Credit Suisse can make no representation or warranty (including liability to third parties) either expressly or by implication as to the accuracy, reliability or completeness of the said information. Credit Suisse shall not be liable under any circumstances for any direct, indirect, contingent, special or consequential loss or damage suffered as a result of the use of or reliance on this information or in connection therewith or by reason of the risks inherent in financial markets. Nothing in this report constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to individual circumstances, or otherwise constitute a personal recommendation to any specific investor. Any reference to past performance is not indicative of future results. Credit Suisse recommends that investors independently assess, with a professional financial advisor, the specific financial risks as well as legal, credit, tax and accounting consequences. The attached report is distributed in Australia by Credit Suisse AG, Sydney Branch (“Credit Suisse”) (ABN 17 061 700 712 AFSL 226896), Credit Suisse does not guarantee the performance of, nor makes any assurances with respect to the performance of any financial product referred herein. Global Bonds Unhedged Global Bonds Hedged

Neither this document nor any copy thereof may be sent to or taken into the United States or distributed in the United States or to a US person. In certain other jurisdictions, the distribution may be restricted by local law or regulation. The entire content of this document is subject to copyright (all rights reserved). This report may not be reproduced, referred to, transmitted (electronically or otherwise), altered or used for public or commercial purposes, either in whole, or in part, without the written permission of CREDIT SUISSE.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in Australia. He is also Head of Investment Solutions and Products.

Andrew has been investing on behalf of clients for over 24 years and was the founder of the Credit Suisse Discretionary Portfolio Management service in Australia. He has managed single and multi asset class portfolios for major superannuation funds, institutions, ultra-high net worth individuals, not for profits and private clients and is Chairman of the Australian Investment Committee.

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in...

Expertise

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 2 standout ASX names for FY26

Livewire Markets

Commodities

Central banks are doubling down on gold - should you?

Livewire Markets