Trade war escalation — time to trim some risk

This week US President Trump announced a second round of tariffs on USD 200 billion of imports from China. The two key issues for markets leading up to this announcement were:

- whether the tariff rate would be at 10% or a materially higher 25%; and

- whether there would be further escalation with a third round of tariffs that covered everything the US imports from China.

While the tariff rate was set at 10% from 24 September, the US announced an expedited automatic increase to 25% from the beginning of 2019 (just a few months away). It also signalled that any retaliation by China would result in a third round of tariffs covering everything China exports to the US (an additional USD 267 billion).

Is there a path to de-escalation?

The US continues to allow little room for China to negotiate. We do not view the US-China trade dispute as a short-term US election-focused tussle, but a more long-lived ideological dispute over global dominance. The path to de-escalation was already narrow, as we noted back in July. It has now turned into the eye of a needle.

This week’s announcement is a material escalation in the US-China trade war. There remains some chance that, post the US mid-term elections, negotiations will limit further escalation and constrain the tariff rate to 10%. However, on balance, we expect the tariff will rise to 25%. As UBS has noted this week, “neither side seems especially eager to take [the de-escalation] path. If that path is eschewed, we see a multi-lane expressway to further escalation and substantive negative economic effects to both countries.”

Adjusting our tactical asset allocation

We are now choosing to trim some risk. This is not inconsistent with our ongoing desire to stay cautiously engaged with markets through the maturing phase of the cycle—this global growth cycle has further to run. It is about recognising shifting circumstances. While markets have taken the latest escalation in their stride, we believe the more aggressive-than-expected US tariff decision and the potential negative growth impacts that could follow for both China and the US through 2019, argue for some caution. The likelihood that US monetary policy may ‘step back’ as a consequence, given still low inflation, also impacts today’s decision.

For some time, we have focused on two primary risk developments to our tactical asset allocation positioning.

1. An acceleration in global wage and inflation pressures that leads central banks to tighten more rapidly and, over time, bring the cycle to its end.

2. Developments which cause the global growth cycle to prematurely falter, such as a trade war escalation.

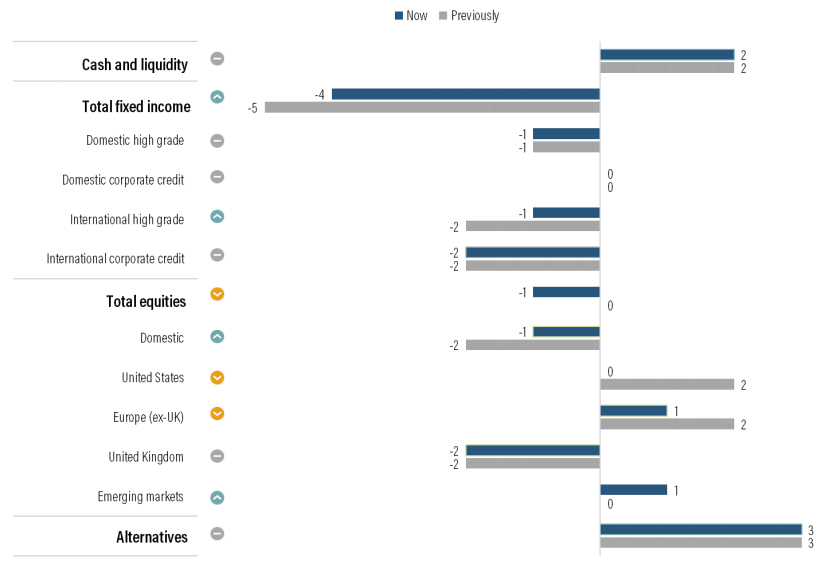

Reflecting this, we are trimming some risk (see chart below):

In particular, we are moving slightly underweight equities from neutral and choosing to add that allocation to international government bonds (moving less underweight as US 10-year yields again reach seven-year highs). Recent tariff decisions now appear more likely to take the edge off global growth, while any potential tariff-driven cost increases in the US are also likely to both increase inflation and weigh on corporate margins in 2019.

We are taking the opportunity to close our overweight US equities position, held since the start of July, reflecting the 9% rise in US markets (in Australian dollars) since we made that decision. Some risk of weaker global growth could also weigh on the market’s demand for growth-orientated investments (which are now expensive) over value-orientated investments. This could benefit European equities (which we are trimming but keeping overweight) and domestic equities (which we are moving less underweight post recent weakness).

We are also moving tactically to overweight emerging market equities. We acknowledge that our decision to edge overweight here may be premature and is not without some risk. However, emerging market equities have fallen 20% in US dollar terms, and this provides a hedge should trade de-escalate or the US Federal Reserve (Fed) pause and the US currency stall its recent upward trend.

We continue to encourage overweight positions in cash and liquidity as well alternative assets, which can reduce volatility and downside risk for a portfolio.

Tactical asset allocation changes—now and previously

Later cycle investing demands caution—not a disengagement from risk

We continue to monitor developments. The upcoming Fed meeting on 26 September and the potential of further US-China negotiations post the US mid-term elections are likely to provide additional clarity and an opportunity to reassess tactical positions.

As always, later-cycle investing demands caution. This means not being overweight risk but still engaged with it. Allocations to risk assets should be close to neutral (or normal), not aggressively overweight. They should also be focused on regions and sectors where growth is strong or valuations more compelling. This involves understanding returns are likely to be more moderate and more volatile than earlier in the cycle and keeping a weather-eye on the macro-economic signals for when the growth cycle is truly shunting meaningfully weaker.

Protecting capital through maturing cycles is also key. Investors should ensure ample liquidity. Seeking out high-quality uncorrelated alternative assets (such as hedge funds) that can protect capital when forecasts are wrong is paramount. When the economic cycle turns, the market’s ability to look through many of the geo-political risks that now confront us will undoubtedly be challenged. This should also be the point investors gather comfort from a diversified portfolio and can put to work liquidity into accumulating high-quality assets at attractive prices

Further Insight

Crestone Wealth Management provides wealth advice and portfolio management services to high-net-worth clients and family offices, not-for-profit organisations and financial institutions. Find out more

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Private wealth advice for high-net-worth and ultra-high-net-worth families, family offices, and for-purpose organisations.

LGT Crestone

Private wealth advice for high-net-worth and ultra-high-net-worth families, family offices, and for-purpose organisations.

LGT Crestone

Private wealth advice for high-net-worth and ultra-high-net-worth families, family offices, and for-purpose organisations.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The undiscovered quality stock in the ASX

Blackwattle Investment Partners