Looking for a turning point

Governments and society have chosen a rapid slowdown in economic growth to save lives. A health crisis has become an economic crisis. Covid 19 has taken hold in Europe and proper testing has only just begun in the US. Prepare for more bad news in terms of new cases globally.

On the positive side, China, South Korea, Japan, Singapore and Hong Kong are showing what works. Quarantining, hygiene, extensive testing and acting early can slow the spread. Although, vigilance must continue as there has been some deterioration in the most recent data from Singapore and Korea. The situation is complicated by the oil war between Russia and Saudi Arabia. Both countries are pumping oil as fast as they can which is pushing the price down – who will blink first? There is concern in credit markets as to which oil companies will fail if any. This drives risk aversion in all markets. However, ultimately a low oil price is good for the global economy.

Looking For A Turning Point

The oil situation has been pushed to the background and the focus is on the new daily case data for Covid 19. The experience with SARS is that markets did not trough until a week after new cases had peaked, which was in late April. When Covid 19 will peak is any one's guess. The experts appear to generally agree the situation should improve as warmer weather approaches in the Northern Hemisphere, as it did for SARS, swine flu and MERS. Mathematics can be used to try and come up with a more accurate timetable.

Australia is approaching winter but has the advantage of a strong health system, learning from Asia and less population density. Using the percentage of people infected in Hubei province (1.15%) as a starting point and assuming the current mathematical measure of the trajectory of infection in Australia continues, one estimate sees a peak in new daily cases in Australia by the end of May (Source: Shaw Stockbroking, “Trying to Get to Grips”, 20th March 2020)

Premier Andrews of Victoria has modelling to suggest it may be mid-June (Source: The Age, 19th March 2020). Of course, we aren’t experts in epidemiology, and this analysis involves many assumptions. While we wait for the outcome, there is a global effort to develop a vaccine. No one seems to question a vaccine will be created, but it will take months. In the meantime, there are promising treatments for the virus being tested with positive anecdotal evidence from the use of a particular combination of a malaria drug and antibiotic.

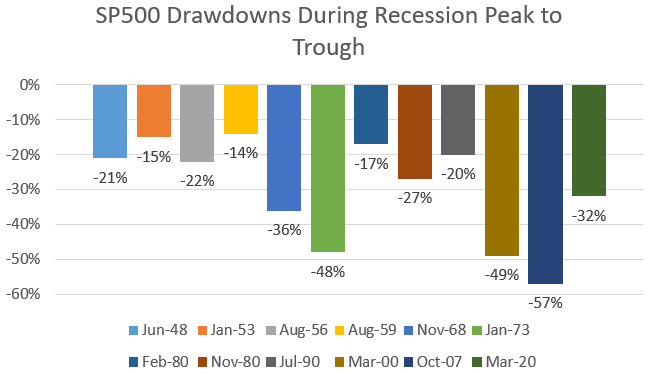

How Much Is Factored In?

So what sort of economic slowdown have markets factored in? Share markets are off around 30% from their peaks. Looking at history, this is about what one would expect for a recession a little more severe than average. During the GFC, global markets fell around 55% peak to trough. This is what you would expect for a severe and prolonged recession. Below is how the current drawdown compares to previous recessions in the US.

Source: Bloomberg, Credit Suisse (Note: Past performance is not an indicator of future performance)

If you assume the fallout will be as bad as the GFC, then stock markets will ultimately fall 57% this year, or another 25% from the peak. Our base case is not a GFC type recession. We believe that as the health crisis eases, the massive and coordinated monetary and fiscal easing around the world will lead to a recovery in the second half of the year and with that a recovery in markets.

Governments and central banks are trying to build a funding bridge for the coming difficult months to ensure businesses and individuals are in a position to restart production and work quickly. That said, markets are likely to get worse before they get better as the virus develops in the US, Europe and in Australia. Even so, we know from past event-driven sell-offs like this one, when the market recovery does start it moves very rapidly. For SARS, a significant amount of the market recovery occurred in the 2 weeks post a peak in cases.

Protecting Portfolios

Our client portfolios are positioned defensively until we are confident a turning point has been reached.

- A full allocation to cash with the large majority of that in US Dollars (USD) has added return given the Australian Dollar (AUD) has weakened by 20% since the start of the year. The AUD appears to have bottomed and we are switching USD to AUD gradually.

- Hybrids and high yield, high risk fixed income funds have become more correlated with equities as markets have sold off as we expected. We do not consider them as providing stability to a portfolio in times of crisis.

- Clients are underweight equities and in particular Australian equities.

- International equities are completely unhedged at this stage, benefitting from our baseline philosophy that it is generally better for Australian investors to be unhedged, given the AUD tends to fall in times of stress, buffering the returns achieved in AUD. Equity portfolios are quality and large-capitalisation biased.

- In Australian equities, we have favoured USD earners such as the miners and healthcare stocks. We have also made some changes to reduce exposure to those sectors most likely to be hurt by lower spending and difficulty refinancing debt.

- In alternatives, the hedge funds we favour are producing uncorrelated returns, helping to stabilise portfolios. For clients including gold in their portfolios, we have added to exposure.

What If We Are Wrong?

If we are wrong, we shall see a fall in shares at least equal to the GFC, another 25% or so from the peak with no recovery before the end of the year. A “balanced” portfolio containing a moderate mix of defensive and risk assets and achieving market returns for each asset class, would have fallen approximately -17% in calendar year 2008, the worst of the GFC.

One could expect a similar return this year under this scenario, unfortunately negating the strong returns of 2019. There are some difficult days ahead, for how long we don’t know. What we do know, is that the best defense for such a situation is a multi-asset class portfolio managed to control risk.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in Australia. He is also Head of Investment Solutions and Products.

Andrew has been investing on behalf of clients for over 24 years and was the founder of the Credit Suisse Discretionary Portfolio Management service in Australia. He has managed single and multi asset class portfolios for major superannuation funds, institutions, ultra-high net worth individuals, not for profits and private clients and is Chairman of the Australian Investment Committee.

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in...

Expertise

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in...

Expertise

Comments

Comments

Sign In or Join Free to comment