U.S. Fed's market interventions...it now owns the recently bankrupted Hertz

Zach Riaz

Banyantree Investment Group

The U.S. Fed's unprecedented market interventions was recently on display. If you are trying to work out why there is such a difference between Main Street and Wall Street, the example below may provide some clues.

As of 12 May 2020, the U.S. Fed has started to purchase ETFs as part of its emergency program known as the Secondary Market Corporate Credit Facility (see below), which we have previously written about in our weekly credit report and in our multi-asset strategy quarterly. Part of these purchases have included high yield ETFs, which hold the bonds of Hertz Global Holdings Inc (HTZ). You may have seen the news recently that Hertz has filed for bankruptcy in the U.S. Bankruptcy proceedings in the U.S. can be drawn out and complex, but there is a chance the U.S. Fed could end up holding equity in Hertz as part of some restructure. We are not entirely sure the U.S. Fed's playbook has a strategy to deal with this type of outcome.

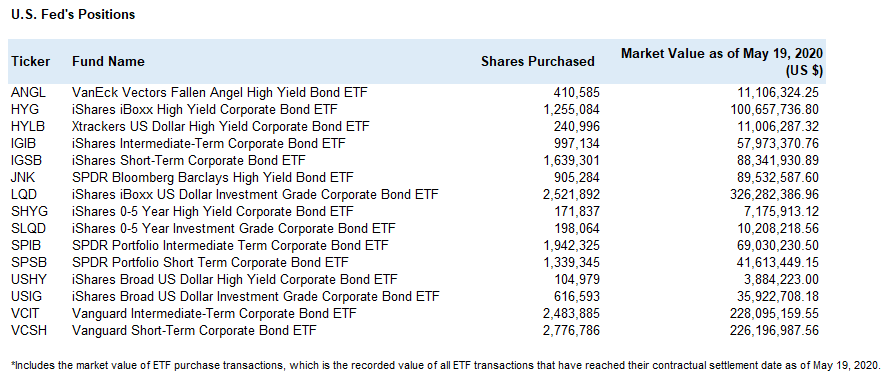

The U.S. Fed's positions disclosed. Whilst the bulk of the U.S. Fed’s ETF purchases are geared towards investment grade, the Fed also purchased high yield ETFs including iShares iBox High Yield Corporate Bond ETF (HYG) and SPDR Bloomberg Barclays High Yield Bond ETF (JNK). Both ETFs hold the bonds of Hertz Global Holdings Inc (HTZ), which has around US$20.6bn in debt. The table below provides U.S. Fed’s disclosures of its ETF purchases.

Source: U.S. Federal Reserve

Background. The U.S. Fed set up several key initiatives to combat COVID-19, which include:

(1) Secondary Market Corporate Credit Facility (SMCCF) with an initial size of US$250bn. The Fed will purchase non-bank corporate bonds in the secondary market which are rated Baa or higher, with remaining maturities of 5 years or less. Further, the facility will also buy Ba-rated bonds if they were downgraded after March 22 – that is, fallen angels. The facility will also buy investment grade ETFs (iShares iBoxx Investment Grade Corporate Bond ETF) and some high-yield ETFs (iShares iBoxx High Yield Corporate Bond ETF). They will limit owning a maximum of 10% of any firm’s debt and owning a maximum of 20% of any ETF.

(2) Primary Market Corporate Credit Facility (PMCCF) with an initial size of US$500bn. The Fed will purchase newly issued non-bank corporate bonds in the primary market issued at Baa or higher, with maturity of 4 years or less. The Fed will buy Ba-rated bonds if the issuer was downgraded after March 22. Part of the deal will allow firms to borrow up to 130% of outstanding debt. What this means is that investment grade firms can refinance all debt and be able to take on additional debt. Firms can use proceeds from new issuance to refinance existing obligations.

(3) Main Street New Loan Facility (MSNLF) and Main Street Expanded Loan Facility (MSELF) with an initial size of US$600bn. The facility will purchase 95% of eligible loans from the banks. This will allow the banks to free up more capital which can be recycled back into the economy. Eligible new loans must keep borrower’s debt-to-EBITDA below 4.0x. Eligible expanded loans must keep borrower’s debt-to-EBITDA below 6.0x. Loans cannot be used to refinance existing obligations.

Hertz is no small company. With a 100-year history, Hertz is one of the U.S.' largest car rental companies and a global brand. According to Bloomberg, the Company has debt of around US$20.6bn on its balance sheet and due to COVID-19 approximately 700,000 cars are not in use. However, Hertz troubles are not all down to COVID-19, it has been facing stiff competition from other car rental companies, but also from disruptors such as Uber and Lyft. This has seen Hertz adjusted net income fall from US$293.8m in FY11 to US$81.4m in FY19.

Potentially more to come? As of 28 May-20, iShares iBox High Yield Corporate Bond ETF (HYG) had over 1,000 positions (including Hertz). How many more could potentially file for bankruptcy in the coming months?

What is the takeaway from Hertz experience? The U.S. Fed (or any central bank for that matter) can continue to pump liquidity into companies and create easy financial conditions (including refinancing), but the Fed cannot improve a company's operating cash flows and revenue. Invariably only the strong business models will thrive (or at least survive) in the end.

Get investment ideas from industry insiders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Investment Manager and Director at Banyantree Investment Group, with responsibilities across equity and multi-asset strategies. Zach has over twelve years’ experience including portfolio management and sell-side investment research.

........

The material in this document may contain general advice or recommendations which, while believed to be accurate at the time of publication, are not appropriate for all persons or accounts. This document does not purport to contain all the information that a prospective investor may require. The material contained in this document does not take into consideration an investor’s objectives, financial situation or needs. Before acting on the advice, investors should consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. The material contained in this document is for sales purposes. The material contained in this document is for information purposes only and is not an offer, solicitation or recommendation with respect to the subscription for, purchase or sale of securities or financial products and neither or anything in it shall form the basis of any contract or commitment. This document should not be regarded by recipients as a substitute for the exercise of their own judgement and recipients should seek independent advice.

The material in this document has been obtained from sources believed to be true but neither Banyantree nor its associates make any recommendation or warranty concerning the accuracy, or reliability or completeness of the information or the performance of the companies referred to in this document. Past performance is not indicative of future performance. Any opinions and or recommendations expressed in this material are subject to change without notice and Banyantree is not under any obligation to update or keep current the information contained herein. References made to third parties are based on information believed to be reliable but are not guaranteed as being accurate.

Banyantree and its respective officers may have an interest in the securities or derivatives of any entities referred to in this material. Banyantree does, and seeks to do, business with companies that are the subject of its research reports. The analyst(s) hereby certify that all the views expressed in this report accurately reflect their personal views about the subject investment theme and/or company securities.

Although every attempt has been made to verify the accuracy of the information contained in the document, liability for any errors or omissions (except any statutory liability which cannot be excluded) is specifically excluded by Banyantree, its associates, officers, directors, employees and agents. Except for any liability which cannot be excluded, Banyantree, its directors, employees and agents accept no liability or responsibility for any loss or damage of any kind, direct or indirect, arising out of the use of all or any part of this material. Recipients of this document agree in advance that Banyantree is not liable to recipients in any matters whatsoever otherwise recipients should disregard, destroy or delete this document. All information is correct at the time of publication. Banyantree does not guarantee reliability and accuracy of the material contained in this document and is not liable for any unintentional errors in the document.

The securities of any company(ies) mentioned in this document may not be eligible for sale in all jurisdictions or to all categories of investors. This document is provided to the recipient only and is not to be distributed to third parties without the prior consent of Banyantree

Zach Riaz

Investment Manager / Director

Banyantree Investment Group

Investment Manager and Director at Banyantree Investment Group, with responsibilities across equity and multi-asset strategies. Zach has over twelve years’ experience including portfolio management and sell-side investment research.

Expertise

Zach Riaz

Investment Manager / Director

Banyantree Investment Group

Investment Manager and Director at Banyantree Investment Group, with responsibilities across equity and multi-asset strategies. Zach has over twelve years’ experience including portfolio management and sell-side investment research.

Expertise

Comments

Comments

Sign In or Join Free to comment