Unintended consequences of ultra-low interest rates

Have low interest rates in the major developed world economies caused asset bubbles in the emerging economies around the globe? What might the consequences of this be? Can leverage ratios continue to increase to support growth? What will happen if interest rates rise? How should this affect our thinking about investing? These are questions that are currently on the minds of many. While we do not purport to know any of the answers as to how the future unfolds, and do not invest on the basis of macroeconomic views, we can analyse the leverage data to potentially draw some sensible conclusions.

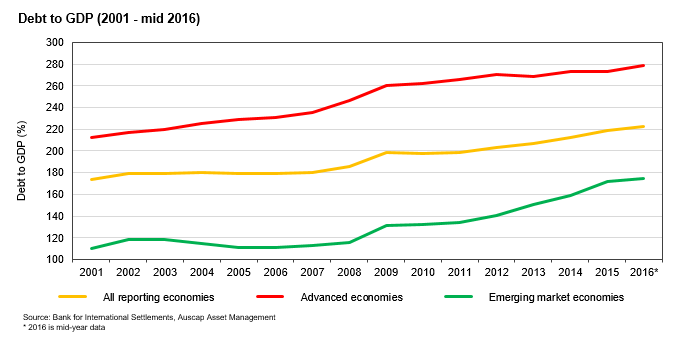

The world has a lot of debt. And leverage has continued to increase post the Global Financial Crisis. The average national economy now has a debt to Gross Domestic Product (GDP) ratio of almost 223%. It is higher for advanced economies at 279%, and lower for emerging market economies at 175%. Albeit emerging market economies’ debt levels are growing faster, with a 65% increase in their debt to GDP ratio since 2001 compared with 49% for advanced economies.

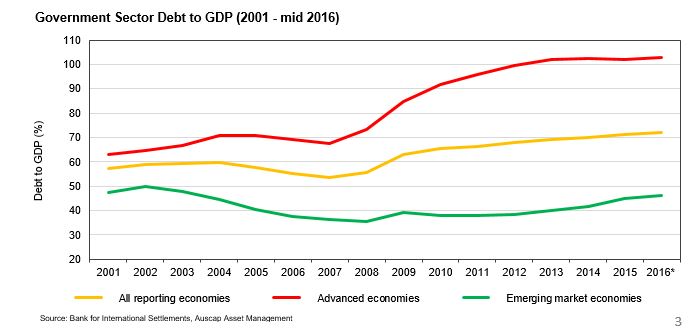

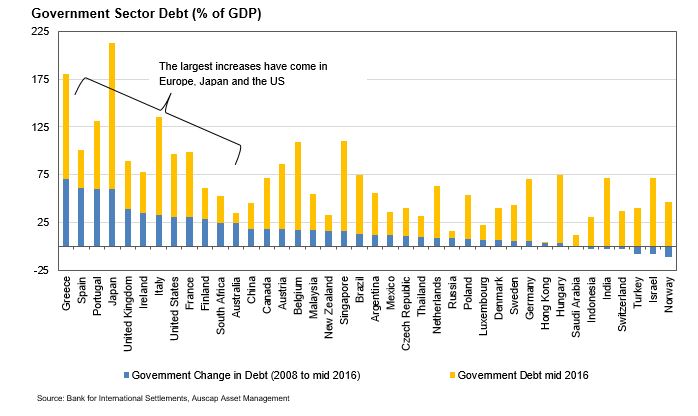

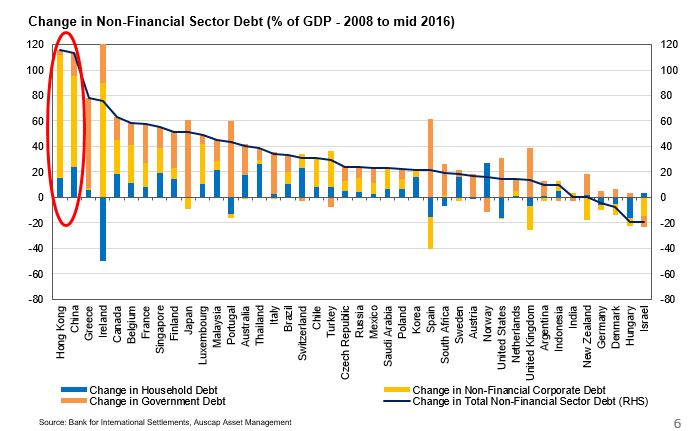

Almost all of the growth in debt in advanced economies in recent years has come from an increase in Government debt. It is probably no surprise that Government debt has increased most quickly in countries within Europe and in Japan and the United States, being those most affected by the Global Financial Crisis. Governments increased spending and took on considerably more debt to reduce the severity of the crisis.

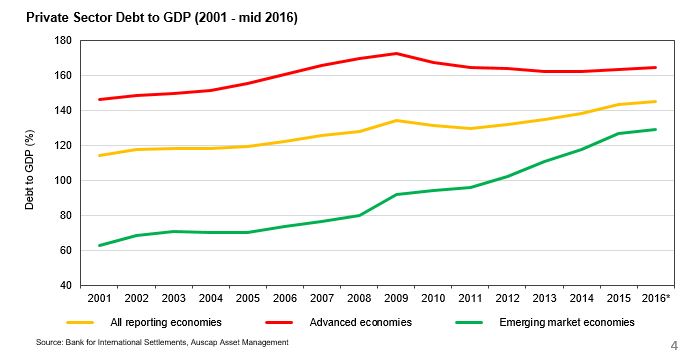

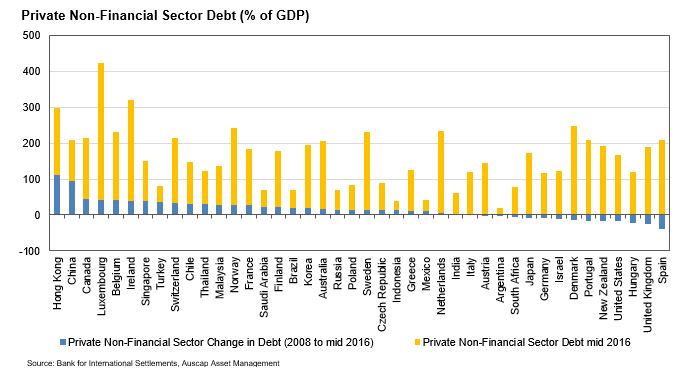

In that same period many advanced economies saw limited private sector debt growth, although the variance at the country level is quite significant. Emerging markets by contrast continued to embrace private sector leverage, with ratios now quickly approaching levels seen in the advanced economies.

While increases in private sector leverage have been most apparent in Hong Kong and China, increases in private sector leverage have not been restricted to emerging market economies. Many advanced economies that are beneficiaries of emerging market growth have also seen a material increase in private sector leverage, including Canada and Singapore.

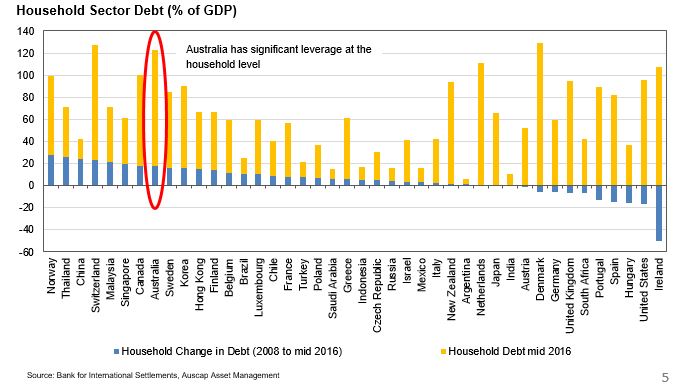

The nature of the accumulated private sector leverage is quite different across different countries. In Australia the increase in private non-financial sector debt has been entirely driven by the household sector, with corporations carrying less leverage today than in 2008.

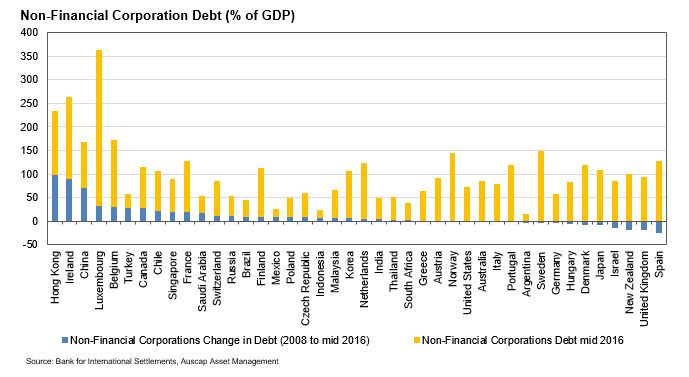

In China and Hong Kong the increase in debt has been broad based, but driven in particular by a significant increase in corporate leverage. This increase in leverage has provided a meaningful boost to economic growth. China currently has one of the highest levels of corporate sector debt in the world.

Indeed the increase in global leverage since 2008 has been most pronounced in China and Hong Kong. Both Hong Kong and China have seen an increase in their non-financial sector debt to GDP ratios of over 100%.

What the future consequences of this accumulation of debt will be is unclear. We do not attempt to make forecasts or predictions about the events that might follow from high leverage in the same way that we do not pretend to have any insight into the direction of equities markets, bond markets, currency markets or the impact of President Trump, Brexit or any other unforeseen event. We would never make an investment based on a macroeconomic view that is more opinion than fact. Trying to work out the consequences of excessive leverage is a very difficult exercise and has left many a forecaster red-faced.

We focus more on what the data might be telling us to do and, sometimes more importantly, what not to do. We avoid markets, industries, sectors, companies and occasionally material exposure to entire economies that have too much debt. In this way, if leverage becomes an issue, while it might impact sentiment and, over time, the broader economy, it does not put our investments directly at risk of a shortage of credit or a sudden rise in interest rates that could affect the viability of the businesses we have shared ownership in. Sometimes the data speaks most clearly in telling us what to avoid, particularly in relation to the macroeconomic data. While we try to avoid predicting unknowable outcomes, we do focus on maintaining discipline with respect to minimising exposure to significant risks as identified through our analysis.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Auscap Asset Management is a value based, active Australian equities investment manager established in 2012. Auscap Asset Management is the Responsible Entity and Investment Manager for the Auscap High Conviction Australian Equities Fund and Auscap Ex-20 Australian Equities Fund. The Funds target solid risk-adjusted returns, looking to invest in companies that generate strong cash flows and are trading at attractive prices.

Auscap Asset Management

Auscap Asset Management is a value based, active Australian equities investment manager established in 2012. Auscap Asset Management is the Responsible Entity and Investment Manager for the Auscap High Conviction Australian Equities Fund and...

Expertise

Auscap Asset Management

Auscap Asset Management is a value based, active Australian equities investment manager established in 2012. Auscap Asset Management is the Responsible Entity and Investment Manager for the Auscap High Conviction Australian Equities Fund and...

Expertise

Comments

Comments

Sign In or Join Free to comment