Upcoming bank results should cheer investors

Three of Australia’s biggest banks – Westpac (ASX: WBC), ANZ (ASX: ANZ) and NAB (ASX: NAB)– are about to report, and we think there’s plenty of reasons to be optimistic. A turnaround in the trajectory of net interest margins, and good news on bad and doubtful debts, should leave investors happy in the run-up to Christmas.

Heading into the half year results in May, the market’s expectations were high due to the belief that mortgage repricing would push net interest margins (NIM) higher. This optimism turned into disappointment as mortgage back book repricing was offset by higher funding and capital costs. This was due to the increase in competition for deposits in August 2016 combined with the need to lengthen the duration of wholesale funding ahead of the implementation of APRA’s net stable funding ratio (NSFR) requirements from January 2018.

So, what is the outlook for NIM in the second half of FY2017?

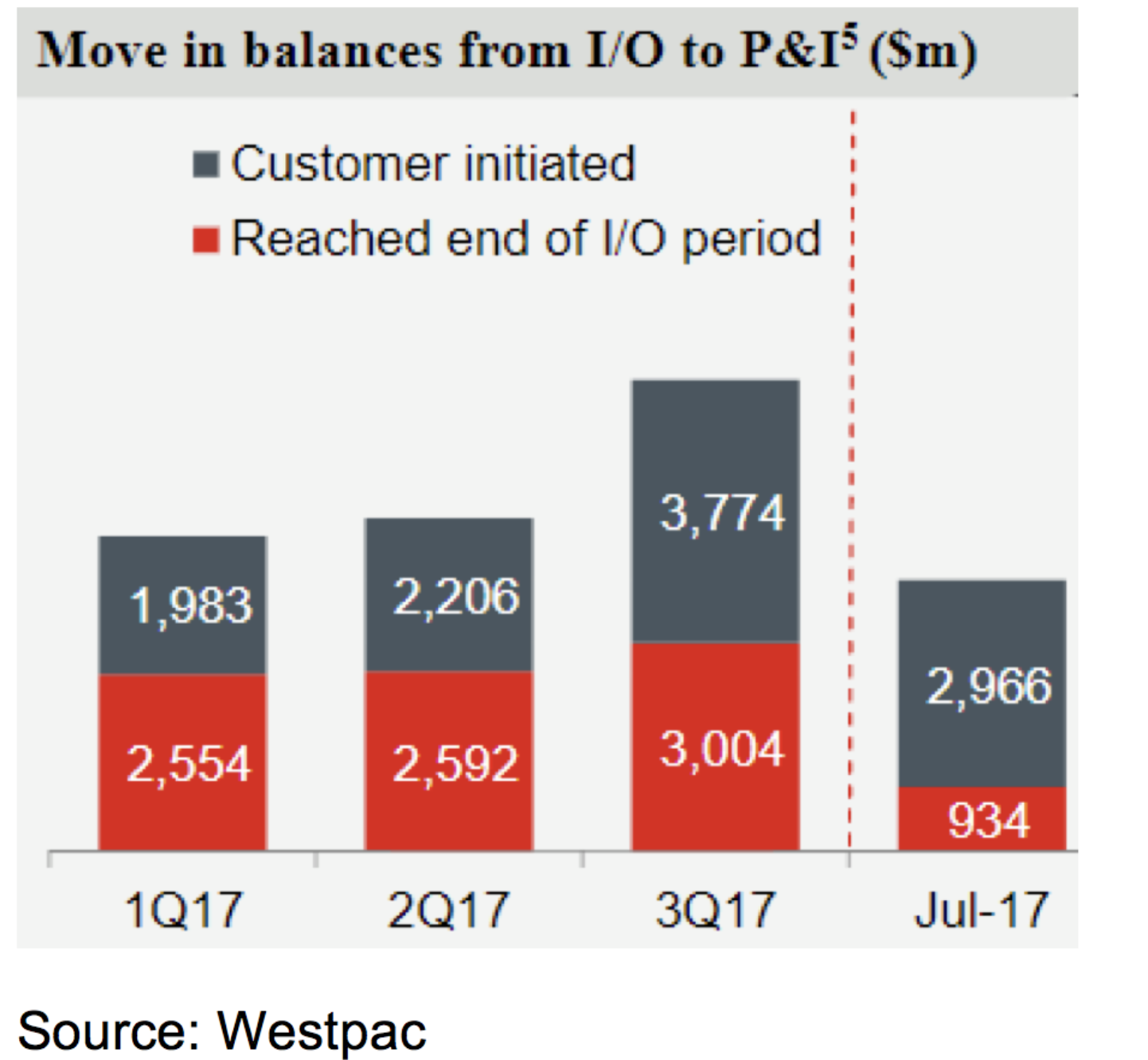

While there remains some need to continue to lengthen the duration of wholesale funding books, deposit spreads appear to have stabilised or even fallen slightly over the last six months. This should result in a more neutral to positive impact of funding costs on NIM in the latest 6 month period. Lower Committed Liquidity Facility (CLF) balances should continue to act as a drag on NIM. At the same time, almost the full impact of mortgage back book repricing should flow through to these results. Mix is likely to be a bit of negative as consumers start switching from higher rate interest only mortgages to lower rate principle and interest products. WBC noted in its June quarter Pillar III filing presentation that A$6.8 billion of mortgage balances had moved from interest only to principle and interest in the 3 months to June. This was a 49 per cent increase on the volume that shifted in the 3 months to December 2016. The monthly rate of switching continued to accelerate in July 2017.

The trends indicated in the June quarter trading updates noted more stable funding costs, while the benefits of loan repricing continued to flow through. This resulted in an improvement in NIM in the quarter for NAB, while ANZ’s NIM stabilised after falling 4bpts in the 6 months to March. After falling in the 3 months to March, CBA reported that its NIM improved 2bpts for the 6 months to June 2017 before Treasury & Markets impacts.

Bank of Queensland (ASX: BOQ) has just reported its results for the 12 months to August 2017. This result showed a 5bpts improvement in NIM in the second half of its financial year.

These data points flag a turnaround in the trajectory of NIM in the last 6 months. As such, the coming results are likely to show an improved performance from this key metric.

The other factor that remains a positive for near term reported earnings is bad debt charges. While already low from a historical perspective, bad and doubtful debt charges are likely to have continued to fall given the non-repeat of collective provision overlays and writebacks. The quarterly results from NAB and ANZ and the CBA 2H17 result flagged that falling bad debt charges are likely to have continued to boost reported earnings growth in the 6 months to September. This was further supported by the 22 per cent reduction in loan loss expenses in BOQ’s result for 2H17.

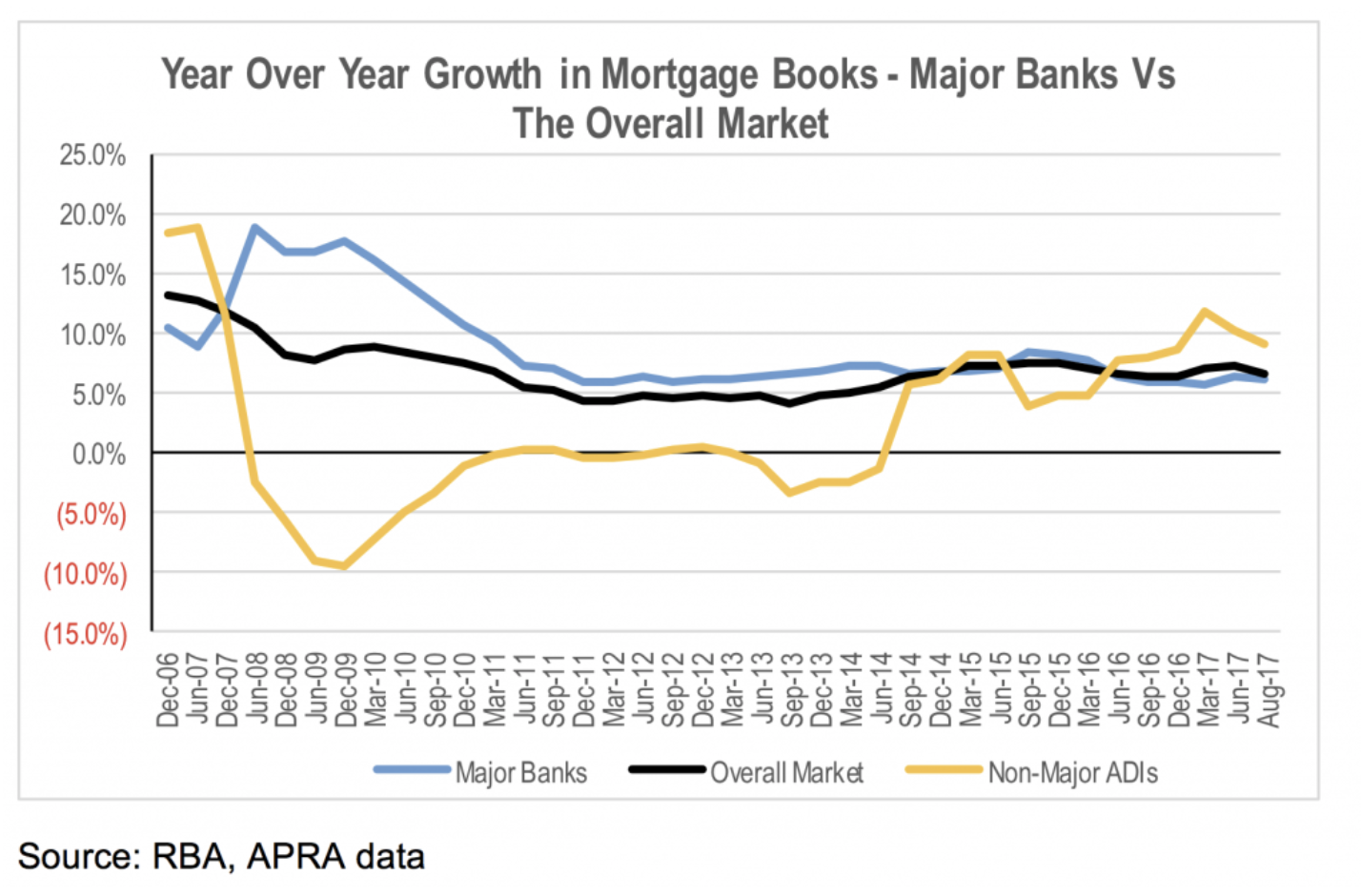

The main source of softness in the second half of FY2017 is likely to be from moderating loan book growth, with overall mortgage book growth slowing marginally, and weak trends in business lending for the major banks shown in the APRA and RBA monthly statistical releases. The data suggests that the major banks have started to lose share in mortgages to non-major lenders over the last 12 months.

After the disappointment from the first half results, the second half results are likely to show improving momentum in earnings growth.

The Montgomery Funds own shares in Commonwealth Bank and Westpac.

If you would like to read more articles by me, please click here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Prior to his departure in August 2022, Stuart was employed by Montgomery Investment Management for over seven years as a Senior Analyst and Portfolio Manager of The Montgomery [Private] Fund.

Senior Analyst and Portfolio Manager

Prior to his departure in August 2022, Stuart was employed by Montgomery Investment Management for over seven years as a Senior Analyst and Portfolio Manager of The Montgomery [Private] Fund.

Expertise

Senior Analyst and Portfolio Manager

Prior to his departure in August 2022, Stuart was employed by Montgomery Investment Management for over seven years as a Senior Analyst and Portfolio Manager of The Montgomery [Private] Fund.

Expertise

Comments

Comments

Sign In or Join Free to comment