Upside for equities but choose stocks wisely

Interest rates increased rapidly during two periods in 2018, both of which preceded or coincided with an equity market sell-off. The yield on the 10-year US Treasury rose by roughly 50 basis points (bps) from the beginning of the year through mid-February and roughly 40 bps from late August to early October. We believe investors are underestimating the potential for rates to make a similar move in 2019, taking the yield on the 10-year US Treasury as high as 4.0%.

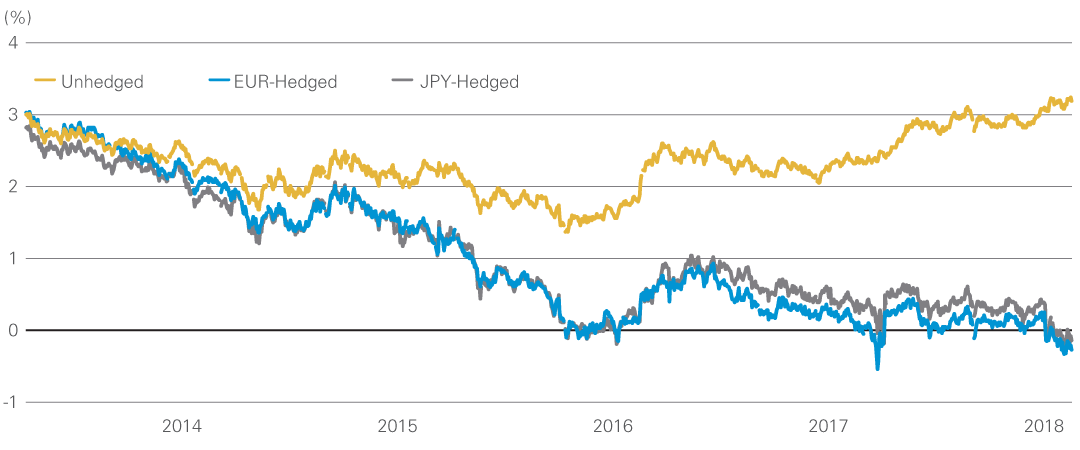

In the United States, fed funds futures reflect just three more Federal Reserve rate hikes of 25 bps in the next two years, while the FOMC is projecting five. In recent years, markets were correct to anticipate that the FOMC would ultimately need to be more dovish than its projections. However, that has not been the case in 2017 and 2018, and recent comments by FOMC members suggest that they feel the need to lean against fiscal stimulus from tax cuts and an expansionary budget. Furthermore, while rates outside the United States remain very low due to continuing accommodative monetary policy—37% of euro zone and 63% of Japanese government debt still has a negative yield—they are no longer the same anchor on US rates. Due to rising currency-hedging costs, hedged yields on US Treasuries are now negative for many foreign investors.

After FX Hedging, US Treasuries Have Negative Yields

Yield on US 10-Year Treasury Note at Constant Maturity

As of 9 November 2018. FX hedging cost calculated based on three-month forward rates. Source: Haver Analytics, Reuters, Federal Reserve

We believe investors should expect more volatility in 2019

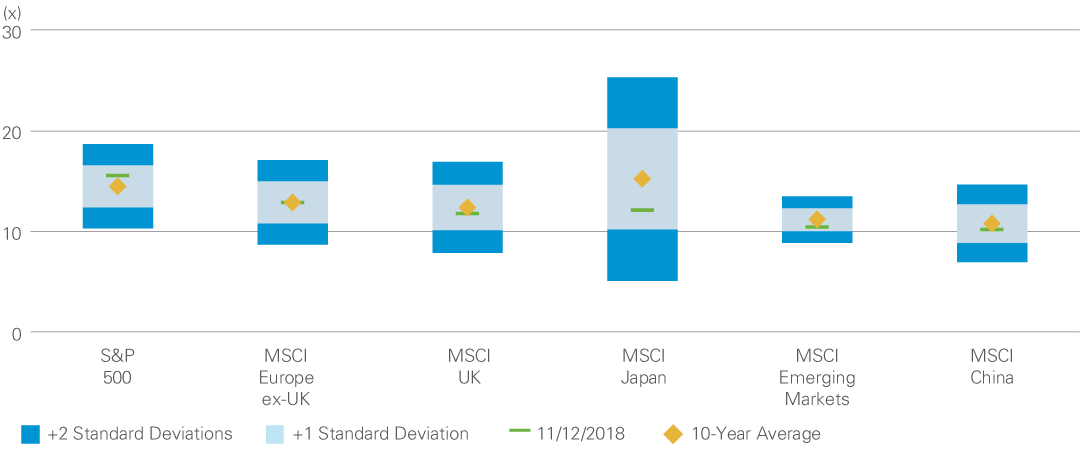

Equity Valuations Are No Longer Expensive

Forward P/E (Next 12 Months), Past 10 Years

As of 12 November 2018. Average and standard deviations calculated based on month-end values. The figures above represent expected returns. Expected returns do not represent a promise or guarantee of future results and are subject to change. Source: FactSet

While we remain cautiously optimistic about the economic prospects for 2019, particularly in the United States, we see a number of important risks on the horizon, several of which have potential for either negative or positive outcomes.

This economic backdrop has a number of important implications for investors, including that, with growth decelerating in many major economies, more market volatility is likely.

Furthermore, while the recent sell-off has made equity market valuations more attractive, returns are likely to be more muted than in past years and primarily driven by earnings growth. In this context, we believe investors should reexamine their equity holdings to ensure they are invested in companies that have high sustainable returns on capital, strong balance sheets, and shares that trade at attractive valuations. These companies, which we call Compounders, tend to participate well in rising equity markets while defending well in falling markets.

In fixed income, long duration, developed market sovereign debt remains unattractive as do bonds issued by risky companies, in our view. Typically, fixed income diversifies risk in portfolios by offsetting equity risk. However, in 2019, we are concerned that rising bond yields could be the cause of equity price declines, implying that the two asset classes could be positively correlated. In light of this risk, avoiding long-duration bonds could be a good choice. However, if the 10-year yield does indeed reach levels near 4%, it could present an excellent opportunity to reallocate capital to long duration, high quality credit instruments in anticipation of gains in the next easing cycle. Alternatively, an allocation to liquid real assets could be attractive, both for their diversifying and inflation-protection properties. Liquid real assets are not risk free, but could offer a different option for investors seeking current income and capital appreciation potential.

Conclusion

In summary, the market outlook for 2019 is murkier than the economic picture. We remain cautiously optimistic on risk assets including equities, but see numerous storm clouds looming on the horizon including tightening financial conditions, protectionism, European political challenges, and the difficulties of rebalancing China’s economy. Fortunately, equity valuations globally are generally in line with or cheap relative to the last decade. The US market is an exception, but even the S&P 500 Index is only 0.5 standard deviations more expensive relative to the last ten years.

Taking stock of the situation, we see upside for equities given the outlook for earnings growth and valuation levels. However, we would caution that at this point in the cycle, investors should take opportunities to upgrade the quality of their holdings with a focus on valuation and strong security-specific fundamentals such as high returns on capital, strong balance sheets, and robust cash flow. Likewise, in debt markets, with US short-term rates finally approximating inflation, investors have an alternative to extending out the risk curve in terms of credit or duration and should take a more defensive approach until the risk/reward trade-off is more compelling.

The above wire is an extract from our 2019 Outlook Series. You can read our full in depth analysis here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Ronald Temple is the Chief Market Strategist for Lazard’s Financial Advisory and Asset Management businesses. In this role, Ron provides macroeconomic and market perspectives to Lazard’s investment teams on a firmwide basis and works closely with Lazard’s Geopolitical Advisory group to assess economic and market implications of key geopolitical issues globally. Ron also advises clients of Lazard’s Asset Management businesses regarding macroeconomic and market considerations that are important to achieving their objectives. Previously, Ron was the Head of US Equity and Co-Head of Multi-Asset Investing for Lazard Asset Management. In this role, Ron was responsible for overseeing the firm's US equity strategies, Multi-Asset investing, as well as several global equity strategies. He was also a Portfolio Manager/Analyst on various US and global equity teams.

Featuring

.png)

Ronald Temple,

Lazard Asset Management

Ronald Temple is the Chief Market Strategist for Lazard’s Financial Advisory and Asset Management businesses. In this role, Ron provides macroeconomic and market perspectives to Lazard’s investment teams on a firmwide basis and works closely with Lazard’s Geopolitical Advisory group to assess economic and market implications of key geopolitical issues globally. Ron also advises clients of Lazard’s Asset Management businesses regarding macroeconomic and market considerations that are important to achieving their objectives. Previously, Ron was the Head of US Equity and Co-Head of Multi-Asset Investing for Lazard Asset Management. In this role, Ron was responsible for overseeing the firm's US equity strategies, Multi-Asset investing, as well as several global equity strategies. He was also a Portfolio Manager/Analyst on various US and global equity teams.

.png)

.png)

Ronald Temple is the Chief Market Strategist for Lazard’s Financial Advisory and Asset Management businesses. In this role, Ron provides macroeconomic and market perspectives to Lazard’s investment teams on a firmwide basis and works closely with...

Expertise

Comments

Comments

Sign In or Join Free to comment