VXO (Original VIX) - Last night's large volatility pullback is a short-term negative for the S&P 500 Index

Andrew McCauley

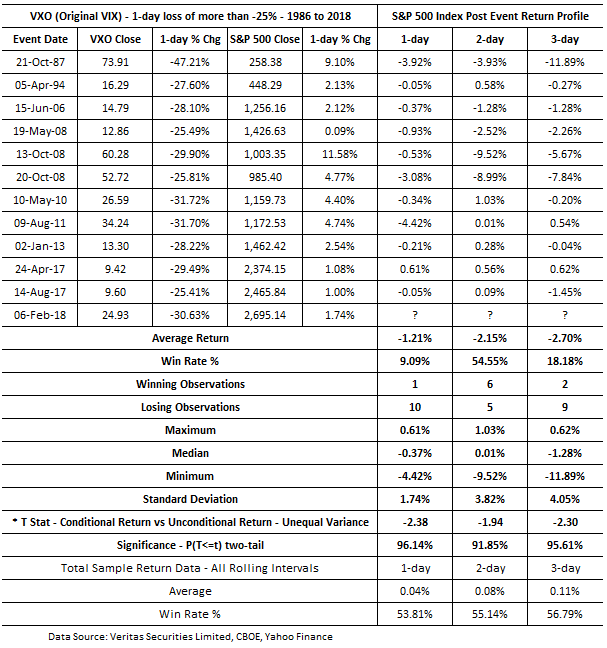

I note that last night the CBOE S&P 100 Volatility Index (VXO – Original VIX) fell by over -25%. Since the inception of the VXO (1986), 1-day falls on the southern side of -25% are very rare, having only occurred on 11 previous occasions. Interestingly, post these large VXO declines, the S&P 500 Index had a tendency to trend lower.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew has over 25 years’ experience in the Australian financial markets sector with extensive knowledge of both equity derivatives and statistical analysis (predictive techniques). Andrew is responsible for delivering evidence based market analysis to Institutional and High Net Worth clients. Andrew recently co-authored a paper on High Frequency Trading that was published in The Journal of Trading.

Andrew McCauley

Statistical Research & Data Analyst

Andrew has over 25 years’ experience in the Australian financial markets sector with extensive knowledge of both equity derivatives and statistical analysis (predictive techniques). Andrew is responsible for delivering evidence based market...

Expertise

Andrew McCauley

Statistical Research & Data Analyst

Andrew has over 25 years’ experience in the Australian financial markets sector with extensive knowledge of both equity derivatives and statistical analysis (predictive techniques). Andrew is responsible for delivering evidence based market...

Expertise

Comments

Comments

Sign In or Join Free to comment