Warning lights in earnings season

While we remain generally bullish on global stock markets, we’ve noted some concerning movements this earnings season that are causing us to take a more cautious position. We have not been scared by the shopping list of geopolitical excitements which are ever-present in international markets and thought the market recovery through the new year was sensible. However, as the earnings season started, we noticed some concerning trends start to appear. We have been looking for evidence of rising costs from commodity inflation and wage rises, which can typify the late stages of an economic expansion. Cost pressures then hit profit margins, which can lead to reduced investment, less hiring, price rises and inflation – all resulting in lower economic activity. We’re seeing hints of these issues coming through now, but we are only at the halfway mark of Q4 reporting season and the evidence does not appear compelling enough

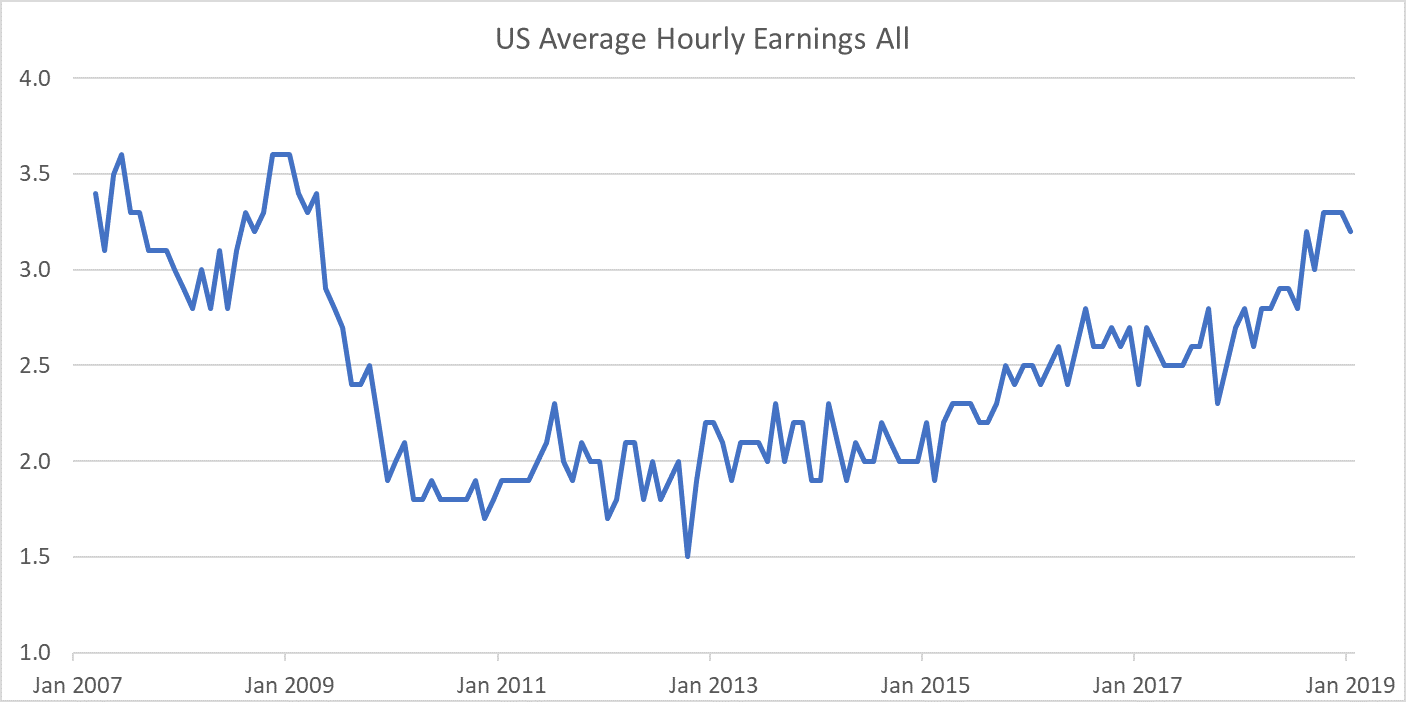

Wages are strong

The latest Bureau of Labor Statistics Employment Situation reported low unemployment at 4.0% and strong hourly earnings up 3.2% to $27.56. Hourly earnings growth has exceeded 3.0% for the last six months, after being below 3.0% since April 2009. We saw these concerns voiced by McDonalds which, in its Q4 earnings call, said “wage pressures … contributed to higher labor cost”. Since then, McDonalds has guided continued labour headwinds in 2019. Wages have been weak for some years, so this stronger growth is positive for consumers and should flow through to companies. Stronger wages in themselves are a good thing, but we look for any evidence that this is hitting margins too much, or that companies are either cutting their workforce or cycling the wage increases into higher prices and inflation.

Source: Bureau of Labour Statistics

Prices raised later in the year and into 2019

In terms of consumer price rises, a number of companies have said they’ve raised prices – including Kimberly-Clark, which reported “about 2 points of positive pricing in the second half of the year” for its tissues and nappies and for 2019 “higher net selling prices of at least 3.0%”. Also included is Unilever, which reported that “price growth picked up at 2.1% [in Q4]” for its broad range of consumer staple products. Diageo suggested 4.0% of positive price/mix on its alcoholic spirits range, while McDonalds cited a menu price increase of 2.0%. This is all more bullish than official US CPI inflation, which fell during the second half from the high 2.0% range back to 1.9%, and it appears that companies are suggesting this could rebound back above 2.0%. This would run counter to the narrative central banks are currently pedalling.

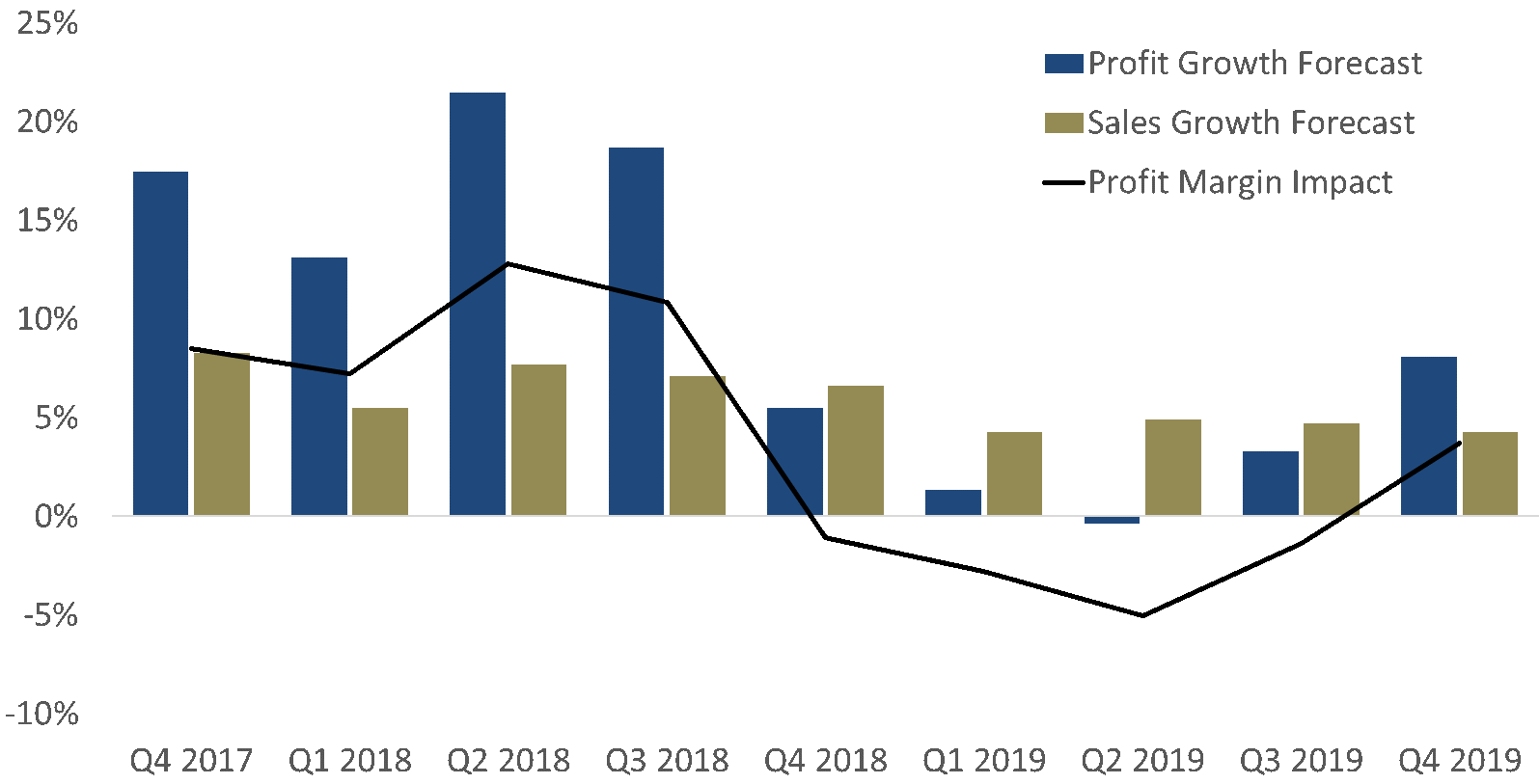

Profit margins

Profit margins expanded strongly in the first three quarters of 2018, but during the mid-point of Q4 earnings, margins appear to have flattened and the consensus is currently forecasting a margin decline through the next three quarters. The forecast weakness is across most major sectors ex-healthcare. Diageo warned that there were limited opportunities for margin expansion over the next six months due to commodity inflation and marketing spend. McDonalds noted US margins were under some pressure from higher labour and commodity costs. But generally, companies have not guided for lower margins over the coming quarters, which is at odds with consensus forecasts. Perhaps it is too early to be concerned since consensus forecasts can be both volatile and biased, but we think it’s worthwhile watching margins.

Around the grounds

There has been some regional variation in terms of revenue and profit growth. Approximately 66% of the S&P 500 have reported, with 6.5% revenue growth at 14.3% earnings growth in Q4 2018 so far. These are strong numbers, but the market is forecasting earnings to decline in Q1 2019, with declining margins in Q2 and Q3. We’ve seen less of Europe, with around a third of companies reporting so far – but earnings have been weaker, with profit margins declining compared to the previous year. Elsewhere, Japanese stocks have seen substantial earnings decline this quarter, after 75% of stocks reported.

Not ‘panic stations’ yet

There has been some conflict between the anecdotal stories from earnings updates and broader data. Companies have been positive on margins, but consensus has turned bearish. Companies have been bullish on pricing, but inflation data is muted. Even though official data supports companies’ claims of higher wages, central banks have been talking down wage pressures and discussed easing policy. The bearish scenario for markets is that wage growth is strong, which is flowing through to higher price inflation and lower profit margins. This should cause companies to cut costs and reduce economic activity, which could contribute to a recession and bear market . At this stage, we only see whispers of this scenario. Nonetheless, we remain bullish on the prospects for stocks, but are also cautious around recent data releases and will closely monitor the remainder of the earnings season.

Never miss an update

Stay up to date with the latest news from Walsh & Co by hitting the 'follow' button below and you'll be notified every time I post a wire.

Want to learn more about Walsh & Co? Hit the 'contact' button to get in touch with us or visit our website for further infomation.

The above is general information only and does not consider any particular investor’s circumstances. It is based on the opinion of the author alone and is not intended to be a research report. The information should not be relied upon to make an investment decision without seeking further information and/or advice from a financial adviser and considering whether any investment is appropriate in the circumstances.

This article may contain statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. The author does not make any representation as to the accuracy or likelihood of fulfilment of the forward-looking statements or any of the assumptions upon which they are based. Actual results, performance or achievements may vary materially from any projections and forward-looking statements and the assumptions on which those statements are based. Readers are cautioned not to place undue reliance on forward looking statements and assume no obligation to update that information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

BML's Chief Investment Officer, Ted Alexander, has been managing investment portfolios since 2008 in London and Sydney. Ted has been the lead Portfolio Manager on multiple funds with a cumulative AUM of over $1.6bn, covering equities and bonds in US, Europe, and Asia, and has led sector research on healthcare, technology, and telecoms.

Ted was the Portfolio Manager on the Orca Global Fund from 2018 to 2022. The fund invested using the same process as the BML Global Fund, with 30-40 stocks, and targeting uncorrelated alpha. The BML Global Fund was launched in 2023.

Ted holds a Master of Philosophy in Economics from the University of Oxford as a Rhodes Scholar and First Class Honours in Economics from the University of Tasmania.

1 topic

BML's Chief Investment Officer, Ted Alexander, has been managing investment portfolios since 2008 in London and Sydney. Ted has been the lead Portfolio Manager on multiple funds with a cumulative AUM of over $1.6bn, covering equities and bonds in...

Expertise

BML's Chief Investment Officer, Ted Alexander, has been managing investment portfolios since 2008 in London and Sydney. Ted has been the lead Portfolio Manager on multiple funds with a cumulative AUM of over $1.6bn, covering equities and bonds in...

Expertise

Comments

Comments

Sign In or Join Free to comment