Watch out for stock valuations when QE ends

Central banks could soon end their bond buying activities, thereby unwinding quantitative easing. Should this occur, real interest rates would again be driven by the normal forces of supply and demand. And this could affect stock valuations.

The basic three components of any company valuation are:

- Earnings growth

- The rate of return a company generates on incremental capital invested to grow earnings, and

- The investor’s risk adjusted required rate of return on their investment.

At Montgomery, our investor education spends a lot of time discussing the first two of these components in terms of assessing the quality and prospects of a business.

However, changes in the market’s perception of the risk adjusted required rate of return is something that can influence both the direction of the market as well as the relative attractiveness of companies given different growth and risk characteristics.

The starting point for the required rate of return is the rate of return required on riskless assets. A premium is then added to compensated the investor for taking on the risks associated with that particular investment. The proxy generally used by markets to approximate the rate of return on riskless assets is the yield to maturity on long duration government bonds.

Government bond rates have been falling for the last 30 years, providing support for equity valuations. However, not all sources of bond yield movements are created equally in terms of their impact on valuations.

Bonds are nominal securities. This means that the return post purchase is not adjusted for inflation rate changes. Consequently, if the outlook for inflation increases after an investor buys a long bond, the total return does not change, but their real or inflation adjusted return falls. In other words, the proportion of the return generated by the investor that is absorbed to maintain the purchasing power of the amount invested increases leaving a lower amount of net return that benefits the investor.

The yield to maturity on bonds can be divided into two components:

The real or inflation adjusted return/yield

Inflation expectations

Equities on the other hand are real securities. If inflation increases, the rate of earnings growth is generally expected to increase, offsetting the impact of higher future inflation on the real rate of return.

Given this offset to any change in inflation expectations, it is the movements in the underlying real yield on bonds that has the most significant impact on equity valuations.

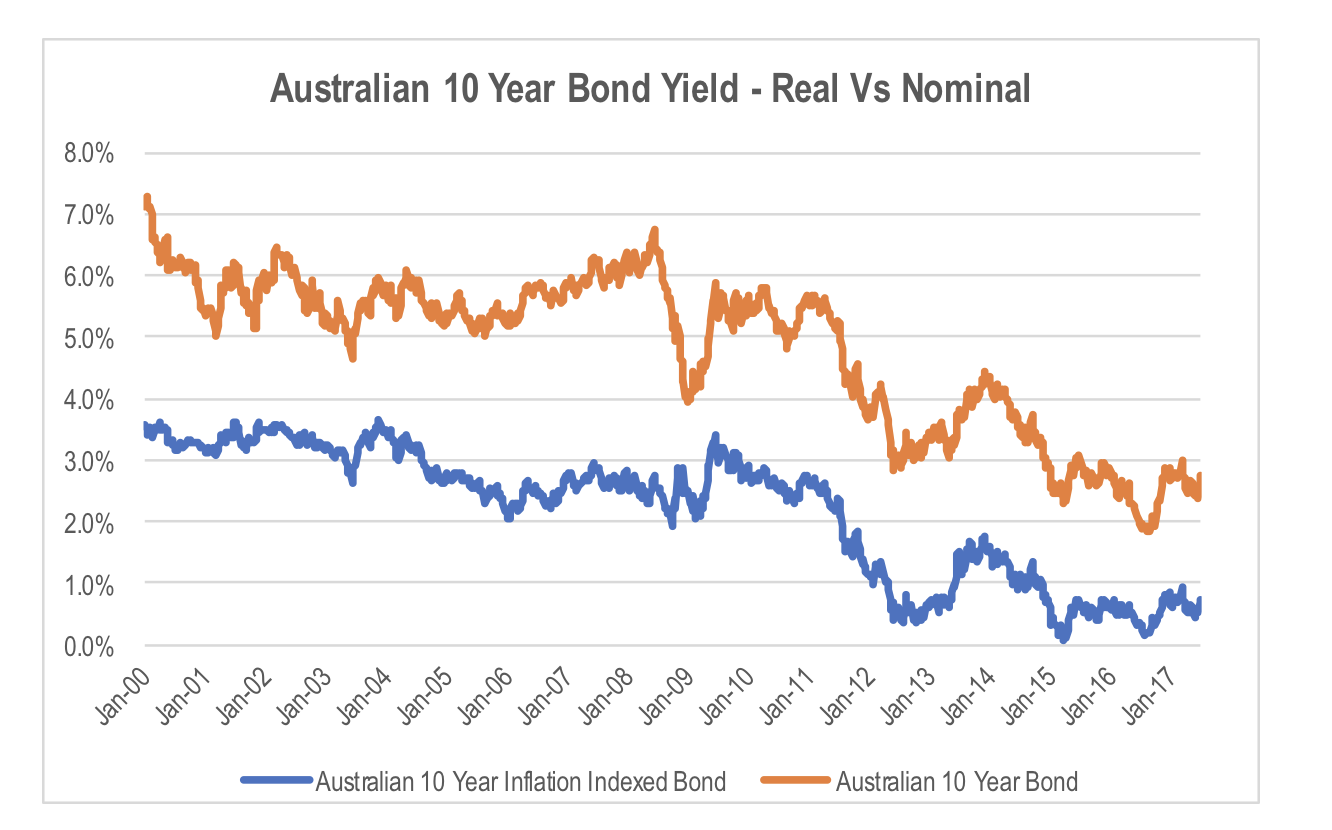

If we compare the yield to maturity on Australian Government Inflation Indexed 10 year bonds to the Australian Government 10 year bond rate, this provides an indication of the market’s estimate of the split of the nominal bond yield between the expected rate of inflation and the real rate of return for the next 10 years.

Both the nominal and inflation linked yields to maturity have fallen significantly, however the inflation linked bond yield has fallen more significantly since 2010.

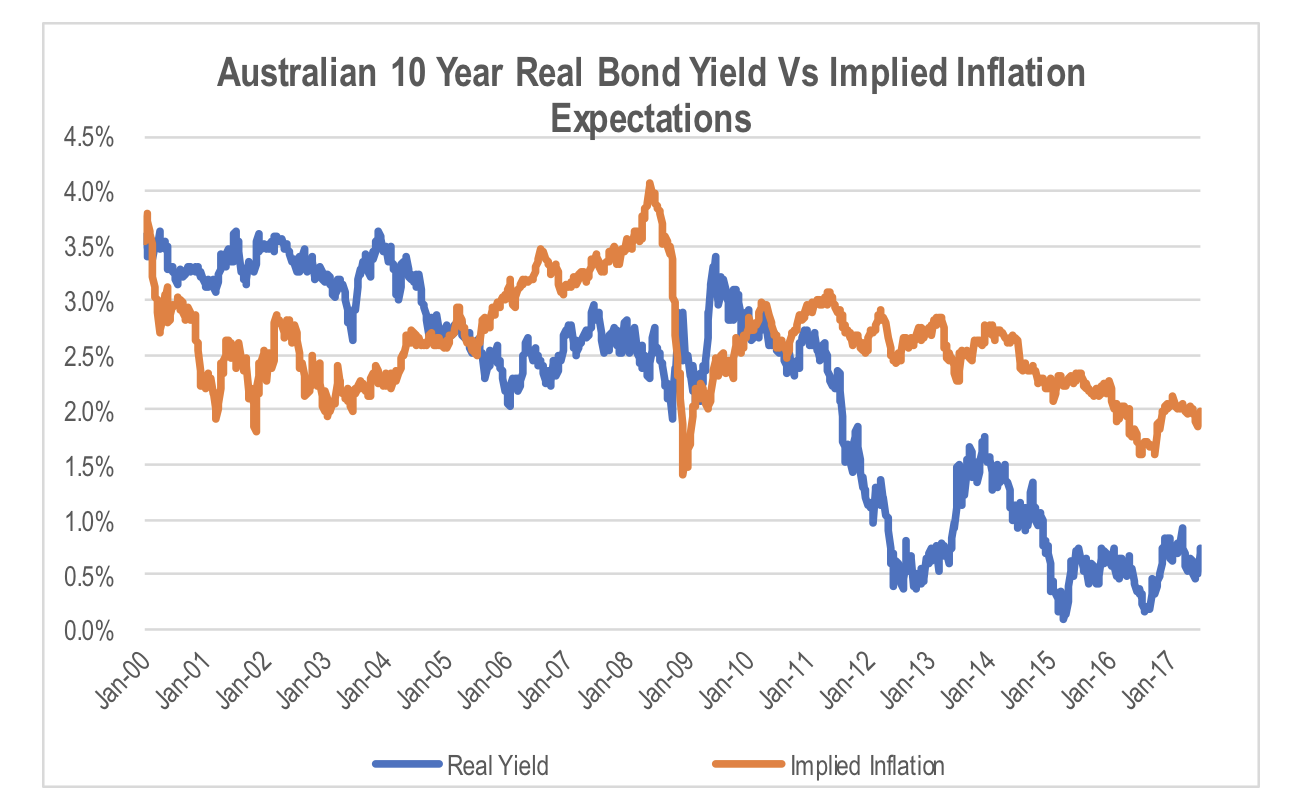

If we split the nominal bond yield between the real yield (as indicated by the inflation linked yield) and inflation expectations (the residual), it shows that while inflation expectations have fallen since 2009, it has generally stayed within the RBA’s target band of between 2% and 3%.

By comparison, real bond yields have fallen significantly, with the main reductions occurring since the start of 2011.

Given that the value of a company’s stock is determined by the discounted value of its cash flow into perpetuity, the price of a stock tends to be more impacted by a change in the discount rate used than the price of a 10 year bond. As an indication of this sensitivity, a one percentage point change in the discount rate will tend to change the valuation of a stock by between 20% and up to as much as 40%.

To the extent that this reduction in real long term interest rates has been passed through to lower required risk adjusted rates of return (ie the cost of capital used in determining the value of stocks), this would explain a lot of the significant re-rating of the market since 2011. Since 1 Jan 2011, the ASX 300 has returned 19.8%. Over the same period, the re-rating of earnings by the market, or in other words the increase in the value the market puts on each dollar of earnings, saw the average PE multiple for the market based on 1 year forward earnings forecasts increase by 21.6%. This means that more than 100% of the increase in the ASX 300 price index was due to increased average PE multiples, with one year forward earnings forecasts falling over this period.

While some of this re-rating of earnings could be the result of a more optimistic outlook for longer term earnings growth, it is also at least partially the result of falling discount rates used in valuing stocks on the back of using lower real risk free rates of return due to lower real bond yields.

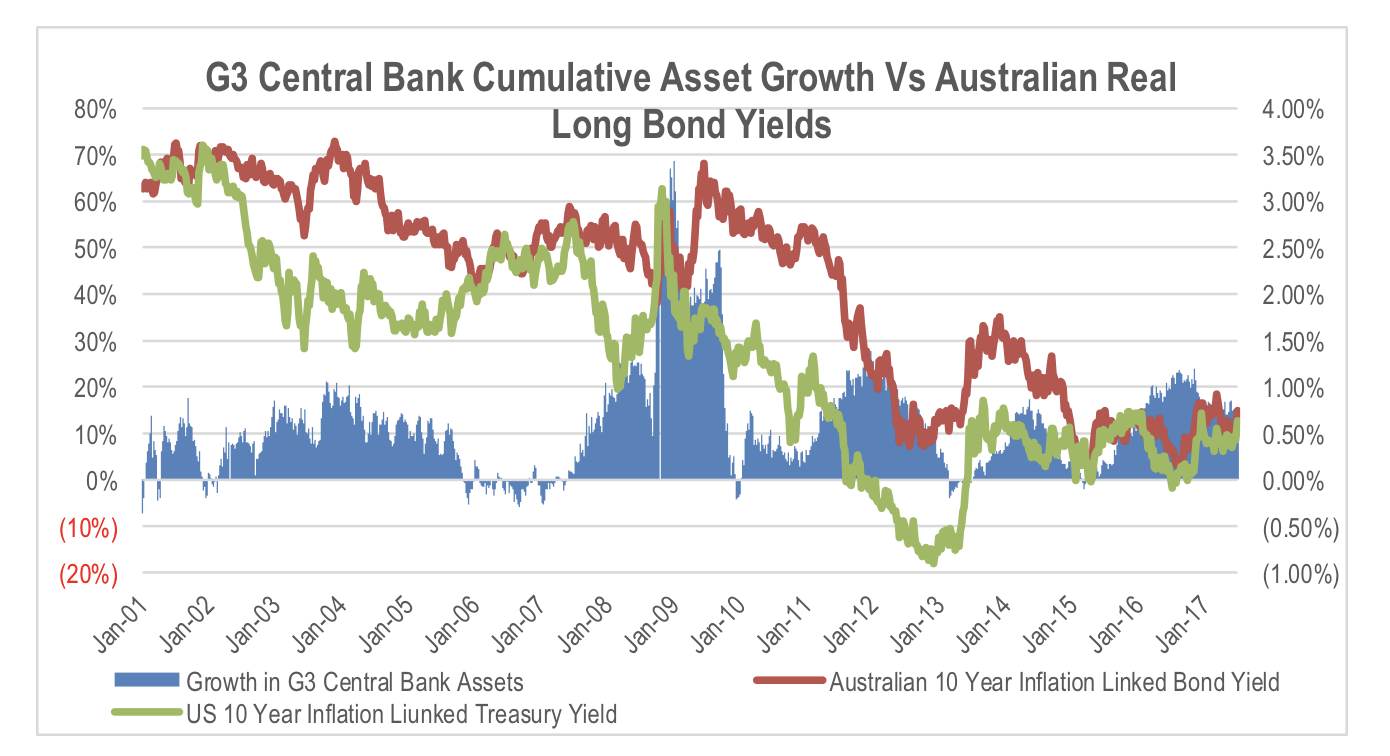

And this is where the problem lies. Real long bond rates have been distorted by central bank buying of bonds. This is known as Quantitative Easing or QE. By buying long dated bonds, central banks drive down long bond yields and monetise government debt used to fund fiscal deficits. There have been a number of periods of strong central bank asset growth since the GFC, which have coincided with periods of significant falls in real bond yields.

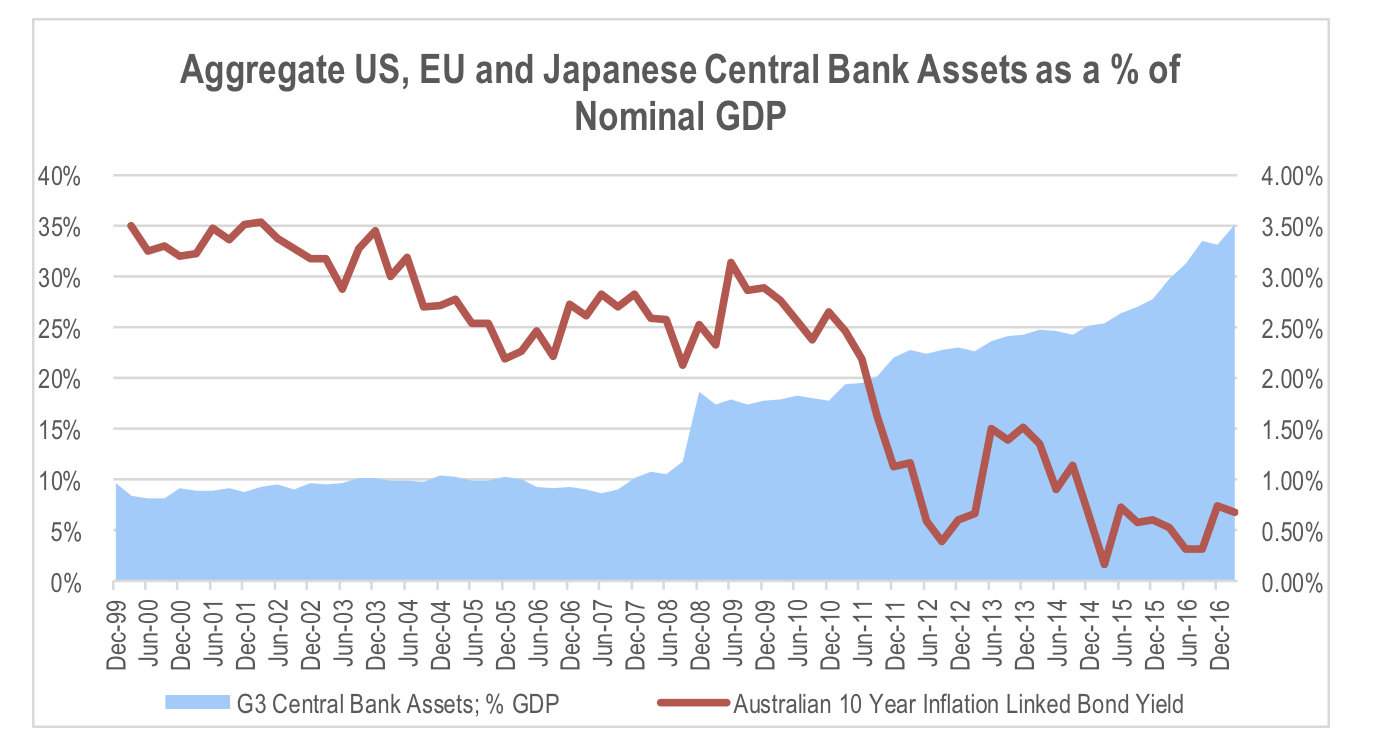

The extreme measures taken by the G3 central banks has seen their asset base expand to very large proportions of G3 GDP.

The point is that these central banks are now making noises about starting the process of reducing the size of their assets in the near term by ending their bond buying activities and no longer replacing bonds that mature, thereby unwinding QE. This will see real interest rates revert to being driven by the normal supply and demand forces of the market after a period of sustained price manipulation by the central banks of the 3 largest economies.

Mean reversion of real bond yields is likely to have a significant impact on stock valuations as this feeds into the cost of capital used by the market.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Prior to his departure in August 2022, Stuart was employed by Montgomery Investment Management for over seven years as a Senior Analyst and Portfolio Manager of The Montgomery [Private] Fund.

Senior Analyst and Portfolio Manager

Prior to his departure in August 2022, Stuart was employed by Montgomery Investment Management for over seven years as a Senior Analyst and Portfolio Manager of The Montgomery [Private] Fund.

Expertise

Senior Analyst and Portfolio Manager

Prior to his departure in August 2022, Stuart was employed by Montgomery Investment Management for over seven years as a Senior Analyst and Portfolio Manager of The Montgomery [Private] Fund.

Expertise

Comments

Comments

Sign In or Join Free to comment