What could a recovery look like?

Matt Reynolds

Capital Group

What does the world look like in 2022? It’s a guidepost that’s driving Capital Group Vice Chairman Rob Lovelace as markets remain volatile and the world copes with COVID-19.

“You have to stop and think about what will be different, as well as what will be back to normal, in 2022,” says Lovelace, who started his investment career at Capital in the mid-1980s.

“When you are able to focus on how much will be the same and see the other side of the valley, that’s really reassuring. It was a much different situation during the 2008 financial crisis because we couldn’t see the other side of the valley and how we were going to reach it. But this time is different, and that gives me hope. While the global economy and financial markets are going to be challenged for some time and government leaders will have to make tough decisions, I believe we will make it through this.”

In a recent call from his home office, Lovelace shared his perspective on Capital’s response to the virus, the company’s business operations, his outlook for global markets and investment opportunities.

What is your outlook for global markets?

The impact of COVID-19 will be with us for some time, certainly into 2021, but will have a diminishing effect over time.

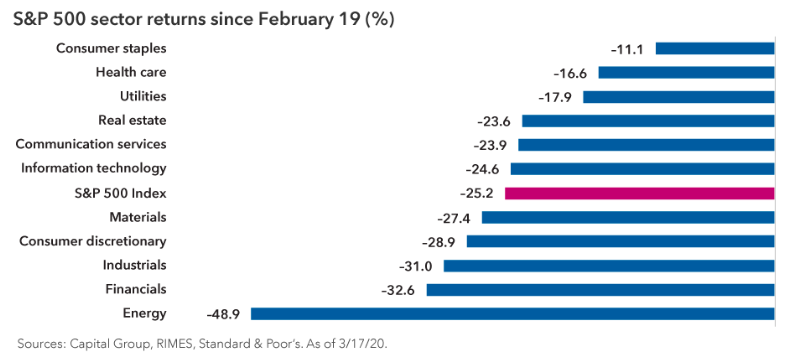

What we learned from China is that we need to act quickly, decisively and with discipline. Chinese equity markets have been relatively stable since they got their situation under control. For instance, Chinese stocks are down 15.9% from 19 February (the beginning of this particular bear market) to 17 March, compared with a decline of 25.2% for the U.S., 21.6% for Japan and 31.4% for Europe.

There’s a bifurcation around the world in terms of the response to COVID-19.

If governments take swift action, it’s still a very big economic shock, but then you have a recovery like we’ve seen in China.

If those actions aren’t taken, you’ll likely wind up with a larger human shock and prolonged economic stress; that appears to be happening in Italy, Spain, the U.K., France and some other countries.

In the U.S., we are trying to decide which way we will go. We’ve done the initial moves, but if we don’t get increasingly locked down and really nip this in the bud, it will move faster and have a bigger impact. It makes it hard to know how wide the valley is. There will be a recession. The question is for how long, and that’s what’s unsettling the market.

The markets are recognizing that the different types of responses from governments will lead to different outcomes in the stock market. Either way, I believe we will get through this and end up in a better place 24 months from now. As long-term investors at Capital, that’s what we already see. It’s just the terrain along the valley floor that we don’t quite know yet.

What are you seeing within specific sectors?

Pharmaceutical companies are obvious beneficiaries, particularly in the U.S. and a few other companies around the world that are working on promising vaccines. And we have companies with excess capacity in their manufacturing lines so they can produce these vaccines if successfully tested and developed.

The consumer staples and food industries have been holding up in this environment, as are beverage makers. The real estate market should benefit from lower rates, but we could see some impact on the commercial side due to a potential hit to small businesses. Increased internet traffic helps phone and communications companies that benefit from higher data usage, and utilities benefit from lower rates. The positive trend for communications and utilities is most pronounced in markets outside the U.S.

Another interesting pattern I’d point out is that quality growth companies in the technology and internet spaces with strong cash flows and strong balance sheets have been holding up.

On the flip side, value stocks continue to struggle in this environment. Oil is running on a dual track, with the economic slowdown and the geopolitical fight between the Saudis and Russians. I ask some of my colleagues: If you wouldn’t buy an oil stock here, where would you buy it? Part of this is politically motivated, and ultimately things do come back.

As investors, we need to focus on what’s permanently changed. The analogy we use is to look across the valley and see the other side. It may be a rough ride, but I know some companies are going to do well. That’s personally what I’m focused on, particularly on some of the internet companies and market leaders we’ve had in our portfolios for a long time.

There are those companies for whom the world has fundamentally changed, such as the cruise line operators. Our analysis is focused on whether patterns have permanently changed for some industries, or will business be back to usual once we get through this?

One other point I would make: There is likely be a global baby boom that emerges from the quarantines and social distancing.

How should we think about the Fed’s recent moves?

The Federal Reserve clearly signalled their concerns by cutting Fed Funds to near zero and instituting various extraordinary liquidity programs last used during the global financial crisis.

Providing liquidity to the system is important and absolutely necessary. We were hearing from our fixed income desks that liquidity has been challenging, even in U.S. Treasuries, typically the most liquid market in the world. To help improve liquidity, the Fed has restarted quantitative easing (QE) with a commitment to purchase $700 billion in Treasury and agency mortgage-backed securities. The Fed also restarted the Commercial Paper Funding Facility to help ensure access for companies to short-term liquidity.

Unlike the Great Recession, the banks are healthy, in part because of the restructuring post 2008. Companies are drawing down lines of credit, and we are watching that closely. In the U.S. we will likely see government assistance to the aerospace, airline and hotel industries, similar to TARP in 2009. I also anticipate aid for hourly workers who may have reduced hours or lose their jobs here, as well as other forms of government support. I would view these kinds of actions as a positive.

How is Capital Group positioned to deal with current challenges?

As a global business with offices in China and across Asia, we have dealt with these kind of market conditions and have overcome these challenges in the past. There was the SARS epidemic, which was regionally focused, and more recently we had the Hong Kong unrest. We learned a lot from those experiences. When the coronavirus emerged, we already had work from home protocols established in Asia and the technology to support our teams. As the situation worsened in Italy, we were in a position that enabled us to be days — and in some cases weeks — ahead of the industry and government directives.

Capital is built for bear markets and being a private company helps. We’re not focused on short-term quarterly earnings, and our associates are not worried about the company’s stock price or losing their job. That can be demoralizing, especially when your stock is losing value.

We have an incredibly strong balance sheet with no debt and a substantial amount of cash.

Another difference I believe that distinguishes us from publicly traded investment firms is we compensate our professionals the same way in down markets and up. This is particularly important for our investment group because our bonus pool is not based on our total assets under management, which can fluctuate depending on market conditions. We keep the formula exactly the same, emphasizing long-term results, and this helps our portfolio managers who may have been holding higher levels of cash and helps balance out the results in our funds.

Is COVID-19 affecting our research process?

As a global investment firm, our investment professionals frequently travel to different parts of the world, meeting with company management teams, government officials and suppliers. Many of us already spent much time out of the office, so working remotely is not a huge transition and we are accustomed to using video conferencing to interact.

Now we are all working from home, and that is giving us even more time to focus on analyzing the data and reflect on what's happening in the markets. We haven't even seen a dramatic drop-off in contacts with companies, because the companies themselves actually welcome video and phone conversations.

Company management teams are hunkered down at home too, and in some cases, they have reached out to our analysts to find out what we know about what is going on in the world and with their industry.

So, I would say our connections with management teams are as strong — or better than ever.

Position your portfolio to navigate through cycles

Capital Group believes in a smarter way of investing that combines individuality and teamwork into a tailored approach to help investors meet their goals. Find out more, by clicking 'CONTACT' below

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The University of Sydney. He also holds the Chartered Financial Analyst designation. Matt is based in Sydney.

1 topic

1 contributor mentioned

Matt Reynolds

Investment Director

Capital Group

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The...

Expertise

Matt Reynolds

Investment Director

Capital Group

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The...

Expertise

Comments

Comments

Sign In or Join Free to comment