What if we get a vaccine?

Our global pharmaceutical team is confident there will be a positive Phase 3 testing result from at least one of the four major trials by the end of the year after analysing all the challenges associated with developing and distributing a vaccine.

However, widespread vaccine production will not occur until early Q3 next year. That may seem longer than the market expects, and could cause a retreat in global markets after a positive initial reception, but we would argue, the timing of a vaccine is less important for markets than the fact that one will be developed. There are three reasons why we believe this to the case.

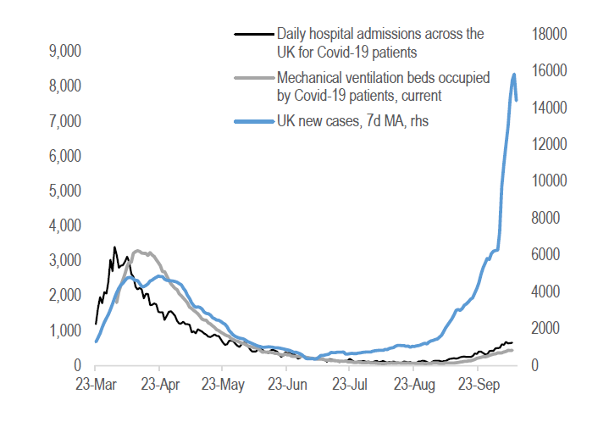

Firstly, it appears treatments have improved. The below graph shows the rate of hospitalisation in the UK versus new daily cases. It is clear that hospitalisation rates have risen much slower than new cases this time around. Dexamethasone, for example, was found to reduce the death rate by a third for those who are most seriously ill (FT, 16 Jun). Synairgen’s drug using interferon beta was found to cut the probability of COVID-19 patients developing severe disease by 79% (BBC, 20 Jul). Promising data, although we should acknowledge nearly half of those who have been infected in the UK are under 40, where the fatality risk is very small.

UK Daily Hospitalisations Versus 7 Day Moving Average New Cases

Source: NHS, Credit Suisse Research

Secondly, mortality is confined largely to the old and those with pre-existing conditions. This suggests that ultimately any widespread second lockdown would likely be age and health condition dependent.

Thirdly, the welfare cost of a second lock down could be high. In the US and the UK, there seems to be an acknowledgment that the welfare cost of a second lockdown (owing to weaker growth, increased stress, patients not seeking medical treatment for non-COVID-19 disease) may be greater than the welfare benefit. To be sure, if we do see another wave of infections, governments will want to ensure hospital systems are not overwhelmed. Restrictions will be imposed, but perhaps not as draconian as in the first lockdown.

At the market level, it is difficult to determine how much of a successful vaccine has been factored in.

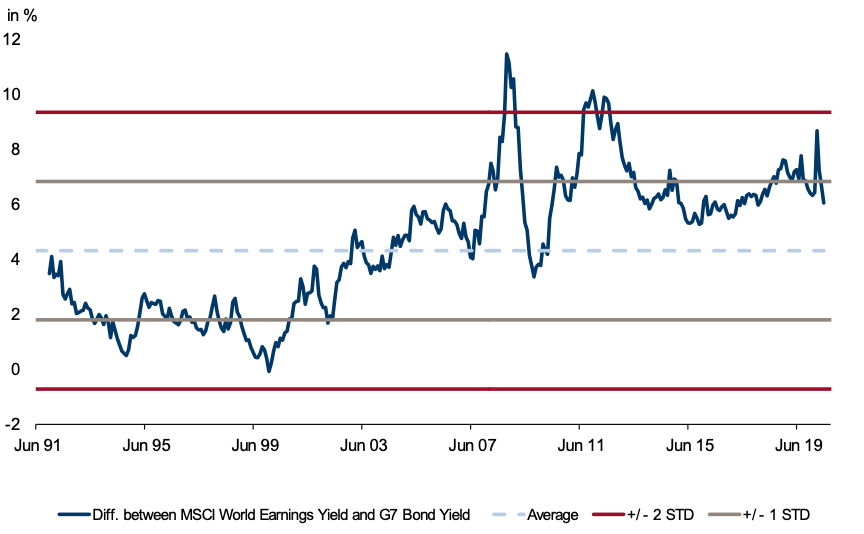

What we can say is that global equities, as measured by the MSCI World Index, in 12 month forward price to earnings multiple terms, is more than 40% above historical norms at 21.2x However, if you look at the relative attractiveness of equities to bonds, share markets still look reasonable value. If you believe central banks will keep bond yields low for the foreseeable future, as we do, and the full probability of a successful vaccine is not fully factored in yet, then you can argue the announcement of a successful vaccine should see equity markets move even higher.

Comparison of MSCI World Earnings Yield to G7 Bond Yield – Reasonable Value

Source: Data Stream, Credit Suisse

At the sector level it is a little easier to determine what will perform after an announcement about a successful vaccine. Globally, our strategists note an increase in spending on goods in developed markets, at the expense of services. Intuitively this makes sense. Banks, travel, airline and retail real estate stocks have suffered with lockdowns. Also, energy and mining stocks have lagged as industrial production momentum has slowed. Software, electronics, food and fashion, enabled by internet transacting and prompted by COVID-19 have done well. A vaccine should see this reverse. Interestingly, the correlation between positive performance of technology stocks and the current second wave has broken down, a sign that outperformance for technology stocks in the short term will be harder to come by.

Globally, we see value in the banks, miners and travel stocks when a vaccine is discovered.

In our Australian portfolios, we have moved banks up to neutral from underweight. Housing prices have held up and the tidal wave of bankruptcies that was expected has not eventuated. We are also overweight the big miners based on a continuously strong China and expected pick up in industrial production. Even if a vaccine is delayed, the lockdowns associated with the Northern Hemisphere second wave are likely to be more benign for economic activity. It remains to be seen by how much.

Learn more

Credit Suisse Private Banking specialises in asset diversification, holistic wealth planning, next generation training, succession planning, trust and estate advisory, philanthropy. Stay up to date with our latest insights by hitting the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in Australia. He is also Head of Investment Solutions and Products.

Andrew has been investing on behalf of clients for over 24 years and was the founder of the Credit Suisse Discretionary Portfolio Management service in Australia. He has managed single and multi asset class portfolios for major superannuation funds, institutions, ultra-high net worth individuals, not for profits and private clients and is Chairman of the Australian Investment Committee.

1 topic

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in...

Expertise

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in...

Expertise

Comments

Comments

Sign In or Join Free to comment