Ignore the impacts of debt-fuelled stimulus at your peril

David Rosenbloom

ICN Consulting

Over the past decade both debt and equity markets have become increasingly disconnected from traditional measures of fundamental value. A sober examination leads to the conclusion that the culture of investors has become increasingly reliant on the notion of policymaker action in relation to stimulus and, more recently, direct intervention in markets. While objective data reveals the effect of stimulus is having a decreasing impact on the real economy, investors cheer on each new measure by bidding up risk assets, safe in the belief that they have become risk free; policymakers have their backs.

Interestingly, concerns of budget deficits and huge government debt which has paid for the stimulus have also been conveniently cast aside, safe in the bosom of the new economic paradigm named Modern Monetary Theory. Boiling it down, markets no longer appear captive to economic fundamentals. All they simply need is huge liquidity and the perception of good news.

This presents difficult choices for investors in a “TINA” world (There Is No Alternative) as the experience of the last ten years can overwhelm fundamental analysis. No one really knows if or when this experiment fails, but simply burying one’s head in the sand, ignoring the downside and blindly playing the momentum game without at least exploring the risks could prove a precarious strategy.

If I told you a year ago that in the face of a global pandemic, the largest contraction in the global economy since the Great Depression and rising geopolitical tensions (e.g. Hong Kong, trade war, etc.) that equity markets would be heading to new highs and credit spreads were heading back to pre-pandemic levels, well I’m pretty sure I know what you would’ve said.

Remember, things weren’t that crisp heading into this pandemic. It was only a year ago that growth surprisingly stalled and central banks did an about-face and renewed the flood of stimulus that began with the onset of the GFC. At the time of that crisis it was expressly acknowledged that several huge structural problems would likely arise from the debt-fuelled stimulus (including the possibility of runaway inflation), but the prevailing situation was much more dire than the aggregate of the future problems; we chose to kick the can down the road.

However, as time went by, no disaster outside the pandemic (as yet) occurred, though growth has been decidedly weak. In fact, world GDP growth has been slowing for decades coincident with increasing leverage, as well as other issues. Interestingly, the longest expansion in US history was also among the lowest in terms of annual growth. Then the black swan event, COVID 19, hits with the consequential stimulatory response, funded by huge government debt dwarfing that of the last decade.

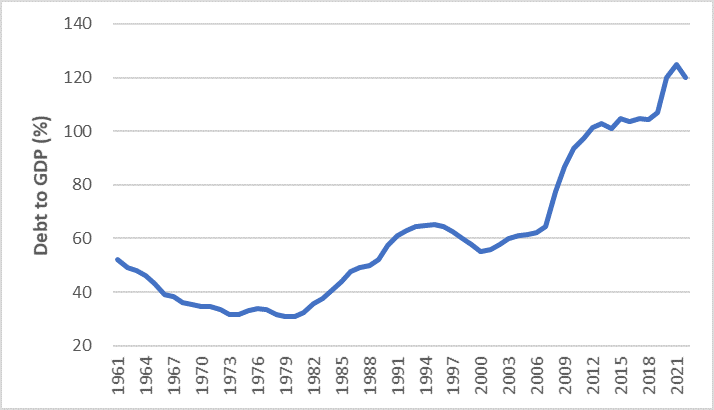

US Government Debt to GDP

Source: Federal Reserve Bank of St. Louis (2020-2022 are latest forecasts)

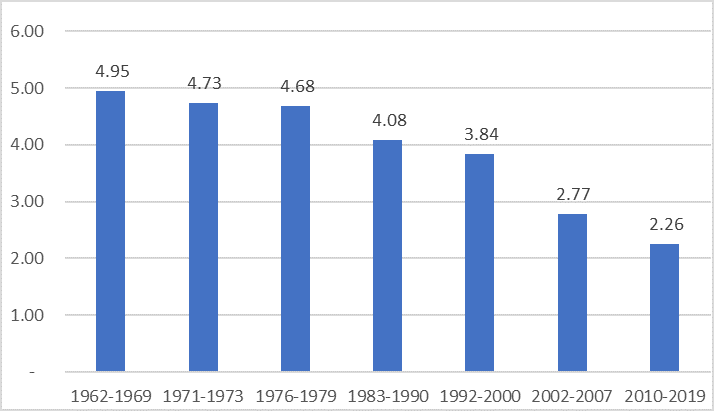

Average Annual US GDP Growth During Expansionary Periods (%)

Source: Macrotrends, ICN

Source: Macrotrends, ICN

Now, in the interest of full disclosure, I am not an economist, though I’ve worked with, met, listened to, and corresponded with more than I care to remember over my career. With that in mind, it seems to me the questions for investors are quite simple, yet the magnitude of the outcomes on portfolios is huge. Can seemingly never-ending stimulus prop up markets indefinitely? What will the impact of these measures be on the real economy? After decades of concern about government deficit spending, is rising government debt an issue of the past, one we should never have spent time worrying about in the first place? Is inflation or deflation the enemy that should hold our concern? Does unprecedented intervention in markets and price setting mechanisms by central banks signal the death of capitalism as we know it? It is a necessary debate that really hasn’t occurred, though it appears that two sides have emerged.

In one corner is the challenger, proponents of Modern Monetary Theory (MMT). These new kids on the block who submit that the level of deficits don’t really matter as they are simply a tool, increasing market intervention is welcome, and these loose conditions can only aid growth. The main enemy? Inflation.

Note that MMT isn’t really a theory, but more of an explanation of how the monetary system works. Suffice to say advocates of MMT tend to be pro-intervention and harbour little concern about government debt levels relative to their neo-classical counterparts. The proponents of MMT are gaining momentum. So much so, in fact, that US Democratic Presidential nominee Joe Biden has appointed MMT’s flag bearer, Stonybrook University Professor Stephanie Kelton, as co-Chair of his economic task force. And why not? It is a politician’s dream to have an open cheque book.

Even here in Australia, a country where government debt is usually the focal point of elections, both sides of the aisle have gone quiet on the question of deficits. Interestingly, at the onset of the GFC, before the notion of MMT had really arisen, the worry was Depression-like deflation; better to risk runaway inflation later than deal with deflation now. In MMT circles, inflation and all other risks are easily brushed aside (or at least banished to the corner of the room).

In the other corner we have the historical champions, those raising alarm bells on debt levels and the consequential deleterious impact on growth. This is a group that includes in its numbers followers of Secular Stagnation, a depression era theory once discredited and now getting a second sounding. The main enemy? Deflation.

Amongst their number (in one form or other) are market luminaries such as Ray Dalio and Stanley Druckenmiller, as well as eminent economists including ex US Treasury Secretary Larry Summers and former Dallas Fed member Lacy Hunt. It’s fair to say that followers of these concepts are much more neo-classical in nature. Basically, their view is that massive government debt retards real growth until such time that it is necessarily dealt with, a period that would most certainly be characterized by great economic pain.

Of course, these arguments could and have been put forward since the onset of the GFC as was formally done by Summers in a 2013 speech. To date they have seemingly been wrong…at least according to markets. However, they have been spot on in one respect: there is no inflation and interest rates are at levels that few would've dreamed. So, are these guys dinosaurs, or is it just a matter of time until they are proved right?

Thus, we have the two sides lined up: those believing in the economic concepts followed for decades versus those who choose to look at the last 10 years as proof that those old concepts are incorrect. Old school versus MMT.

Further muddying the waters in the short term are other loosening policies enacted by central banks around the world which have been intervening in such a way that market-derived pricing signals have been lost. The recent historic announcement that the Fed would buy individual corporate bonds springs to mind. Even interventionist ex Fed Chair Janet Yellen believes the Fed has overstepped its bounds in many respects, reacting to such decisions as lending to states and municipalities with surprise or even disdain. In addition, the policies may have redefined “short term” to a period much longer than previously thought. Or as the old saying goes, markets can stay irrational longer than one can stay solvent; that can keeps getting kicked down the road.

Picking sides in this discussion is of the utmost importance as market and economic impacts likely hang in the balance. Firstly, however, we must not forget that the unprecedented stimulatory policies have been in place more than a decade. Despite them, or because of them, this period has been categorized by the following which are objective, not opinions. These are the facts:

- Sluggish economic growth

- Low inflation and stagnant wages

- Declining real interest rates, in many cases into negative territory

- Increasing government debt partially offset by an increase in the personal savings rate

- A boom in financial assets

- A decline in capital investment

- A growing output gap (gap between actual output and potential output)

- A marked slowing in the velocity of money

- Continuation of a decline in birth rates globally; demographic headwinds continue to rise and are only made worse with the rise in nationalism

- Unprecedented central bank intervention in the price discovery process.

In addition to these factors, we've seen a cultural change which likely finds its origin with the appointment of Alan Greenspan as Chair of the Federal Reserve in 1987. Who can forget the “Greenspan put”, a phrase bandied about markets referring to comfort that was assumed to be forthcoming each and every time markets began to wobble. In fact, it almost appears that the tail is wagging the dog with the perceived policy impacts on markets more the focus than their underlying impact on the economy.

Secular Stagnation

In 2013 former Treasury Secretary Larry Summers delivered a speech to the IMF reviving the theory of secular stagnation. In short, followers of this notion believe that central bankers can no longer use traditional interest rate and money supply policies to spur consumption and investment. While perhaps effective in the short term (certainly aiding market sentiment), and having worked historically at economic troughs and bottoms, many have shown the efficacy of these overused measures is waning as the US GDP growth figures below attest. In addition, McKinsey’s think tank analysis suggests that at government debt/GDP levels over 50% each incremental dollar of deficit spending has a proportionally lower positive impact on growth. While financial assets are boosted, real investment and consumer demand suffer.

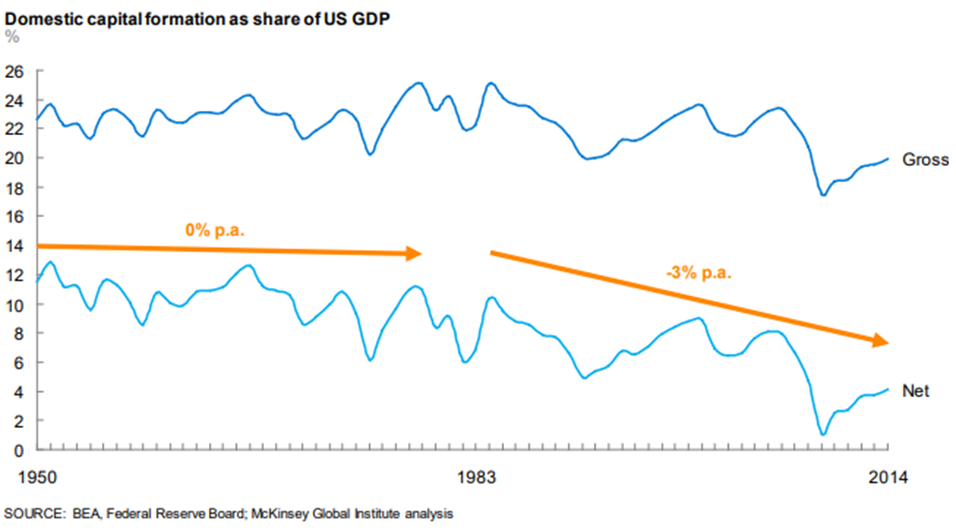

A case in point is net capital formation in developed countries that has been declining for years. Using the US as an example reveals a 35 year slide from around 12% of GDP to around 3%. Of course, movement of capex to cheaper labour jurisdictions explains part of it, but certainly not all.

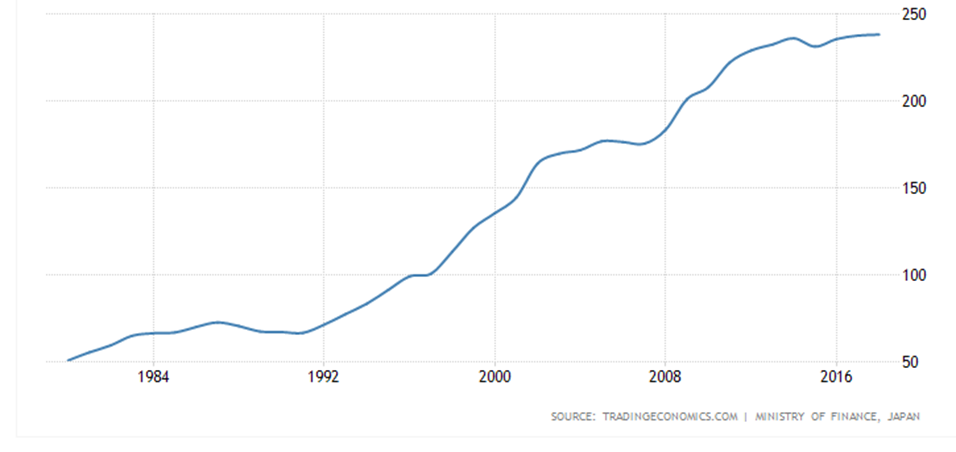

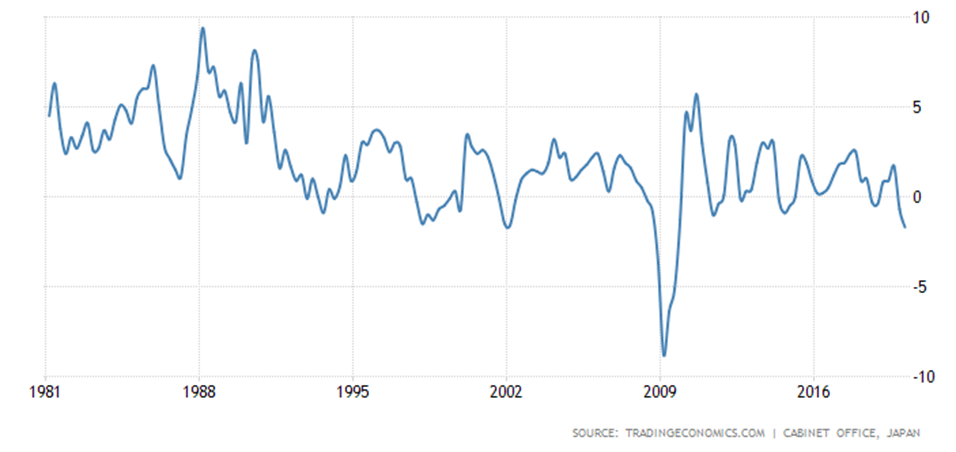

To find a real-life example of the problem one has to look no further than the plight of Japan, which has tried to battle stalled growth via deficits for decades. Few would argue that this has been a successful endeavour as evidenced in the charts below. Why would we think the same measures would result in a different outcome in the rest of the world? And remember, since 1990 the Japanese stock market is basically flat while the S&P 500 has quadrupled!

Japan Debt/GDP

Japanese GDP Growth

- Japan now has the highest government debt/GDP in the world at 238%. This compares to the US at 107% and Australia at 45%.

- Once the envy of the world, Japan’s GDP growth has wobbled between 3% and -2% for decades despite record stimulus continually thrown at the problem.

So what?

Given the current pandemic, the fact that increasing government debt since the GFC has not resulted in inflation or deep recession, coupled with the political attractiveness of stimulus, it is hard to believe there will be an end to policymakers’ current actions in the near future. The printing presses will keep on rolling. It is also hard to argue risk assets are cheap whether you are an MMT or Secular Stagnation proponent.

The practical implications of falling solidly in the secular stagnation camp, a camp that actually has objective evidence backing it up, is that near term inflation is not the enemy. The view is that real rates will continue to fall, growth will not accelerate, and, in fact, deflation may well occur. This means the view on high grade government bonds must adjust to a more positive stance on a secular basis, even at these historically low rates.

Furthermore, if correct, the liquidity boom will at some stage fail to prop up equity markets and further anti-capitalism interventions in price setting mechanisms will be unable to stop “zombie companies” from failing. The most likely scenario is continued or worsening substandard growth for years to come while the worst case is for disruption if/when the debt issue is finally dealt with. In either case, the risk versus reward balance for most asset classes appears skewed to the downside on a medium term basis. Certainly "tail risk" has risen. In the short term, however, excess liquidity, FOMO, momentum etc. may well drive markets higher. Surely, however, investors need to understand that major risks do indeed exist and re-examine their risk appetite and downside scenarios. How much are you prepared to lose?

Get investment insights from industry leaders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

David is the principal of ICN, an investment consultancy providing investment and asset allocation advice to Australian businesses and investment companies. Prior to ICN, David was an institutional portfolio manager, both long only and absolute return, at ARCO Investment Management, Janus Henderson and Wallara Asset Management. David also has corporate strategy experience at ANZ and Sumitomo Trust (NY).

David Rosenbloom

Principal

ICN Consulting

David is the principal of ICN, an investment consultancy providing investment and asset allocation advice to Australian businesses and investment companies. Prior to ICN, David was an institutional portfolio manager, both long only and absolute...

David Rosenbloom

Principal

ICN Consulting

David is the principal of ICN, an investment consultancy providing investment and asset allocation advice to Australian businesses and investment companies. Prior to ICN, David was an institutional portfolio manager, both long only and absolute...

Comments

Comments

Sign In or Join Free to comment