What to do in a soft retail environment

Entering the local reporting season it’s unlikely that sentiment toward the domestic housing market could be much worse. By and large, we share the popular concerns with our base premise being, without significant foreign capital or an RBA intervention, Australian house prices must mean revert towards a sensible valuation range for the average Australian to ensure affordability.

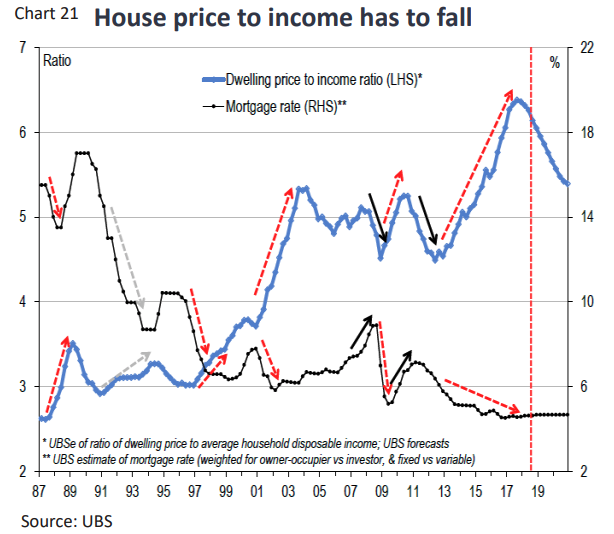

The access to credit is obviously the next consideration. Chart 21 highlights that in the 1990s, the average house price to income ratio was around 3x, before rising to 5x in the heady days of double-digit credit growth.

So when the average house price to sales ratio spiked to above 6x, it was largely driven by the foreign (Chinese) capital flows arbitraging Australian house prices to other OECD countries. Without that flow, and with the backdrop of the inability to access credit with the prospect of a Labor government looming, it appears to be very much a buyers market.

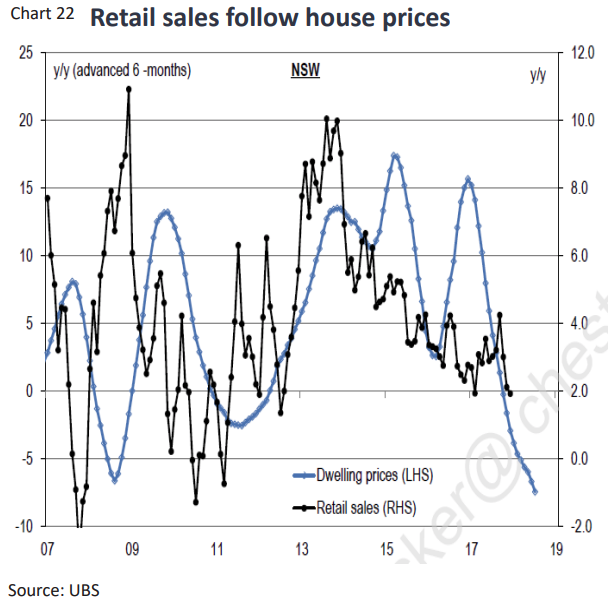

Chart 22 highlights the wealth effect of falling house prices on retail sales. While this is in aggregate, and given how leveraged the average Australian is, it appears inevitable that the retail weakness continues while housing softens.

It is a very tough time to be an Australian retailer.

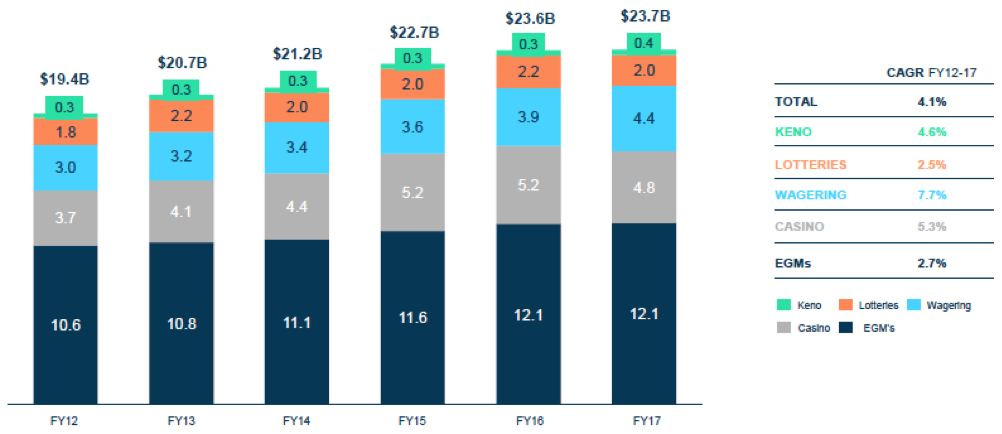

Against this challenging backdrop, we continue to spend time assessing where there are structural consumer trends that can offer favourable investment opportunities. We wrote previously about our position in Tabcorp (TAH) which we feel provides relatively defensive exposure to growing cash flows. Aided by recent regulatory changes that reinforce the value of TAH’s exclusive long term licences across the fields of wagering, lotteries/keno and electronic gaming services we would expect consumer spending in these segments to remain relatively resilient in the face of a tougher consumer environment. (Chart 23)

Source: Tabcorp

Source: Tabcorp

Our near-term confidence in TAH is heightened by the profit upgrade that Jumbo Interactive (JIN) gave in December. As a pure online retailer, JIN simply resell Lottery tickets on behalf of TAH and advised that TTV (Total Transaction Value) growth was expected to be 44% up from the initial 20-25% growth it had forecast.

Accounting for over 40% of TAH’s earnings (EBITDA), a strong result from the group’s lotteries business should underpin a solid group result as the business seeks to realise further cost benefits from its 2017 merger between Tabcorp and the Tatts Group.

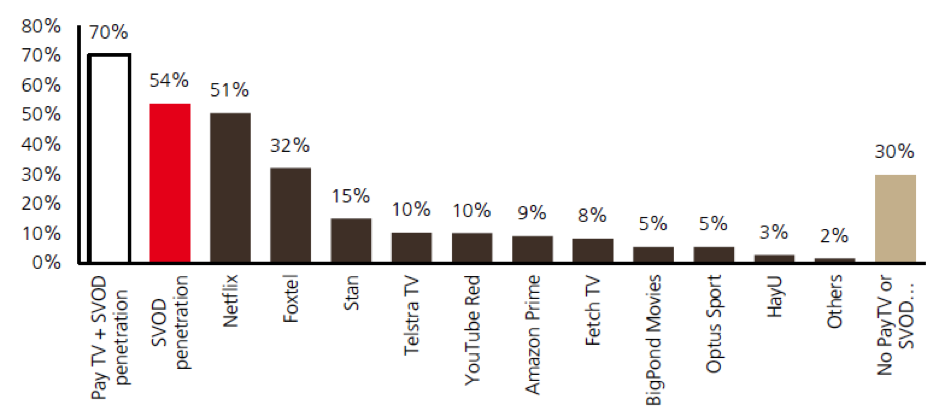

The other structural growth trend occurring in Australia, and has done for a while, is the trend towards Streaming Video on Demand (SVOD). Mirroring trends seen globally over the last decade and encapsulated by the ‘cutting the cord’ phenomenon that continues at great pace in the US, consumer preference for greater flexibility when accessing content is unquestionable. This trend is especially strong amongst millennials (and Gen X’ers) whose viewing experiences have evolved with the rapidly changing world of digital devices and Smart TVs.

In the domestic market Foxtel, Netflix and Stan are the undoubted content leaders, albeit operating quite different business models. Since 2015 when both Netflix and Stan launched in Australia Foxtel’s traditional pay TV model has become increasingly challenged and one it is rapidly trying to redress with the launch of competing streaming products. In addition to the appeal of no term contracts with Netflix and Stan, the value proposition of Foxtel continues to be viewed poorly (AUD50-100/pm depending on the number of channels taken). On the other hand, the perceived relative value of Netflix (AUD13-17/pm) and Stan (AUD10-15/pm) is driving strong take up for their syndicated and original content offerings.

Valued at between $450-$500m by Grant Samuel, the independent expert engaged by the Fairfax board to review the proposed Nine Entertainment (NEC) merger, we expect Stan can become an increasingly valuable asset within the wider NEC portfolio of assets (currently <20% of NEC market capitalisation). As content distribution becomes increasingly fragmented (including live sport) in the coming years we expect Stan will benefit from its early push into the domestic streaming market that has seen it gain about 1.2m subscribers too date and significant brand recognition (Chart 24)

Source: UBS (Survey results from ~1900 respondents)

To summarise, we have the view that while much of the backdrop for Australian consumption is weakening, Australians will always gamble and watch TV!

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Rob recently founded Chester Asset Management after 7 years at SG Hiscock where he was PM of the SGH Australia Plus product that delivered in excess of 10% outperformance per annum over 3.5 years.

3 stocks mentioned

Rob recently founded Chester Asset Management after 7 years at SG Hiscock where he was PM of the SGH Australia Plus product that delivered in excess of 10% outperformance per annum over 3.5 years.

Rob recently founded Chester Asset Management after 7 years at SG Hiscock where he was PM of the SGH Australia Plus product that delivered in excess of 10% outperformance per annum over 3.5 years.

Comments

Comments

Sign In or Join Free to comment