When to close a short position

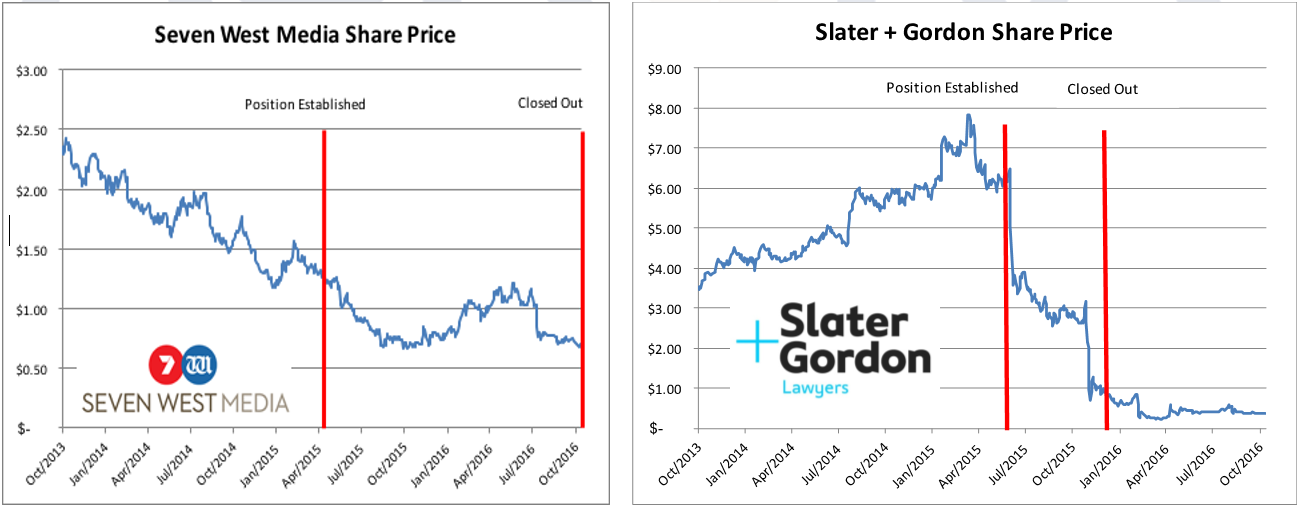

Short-sellers are frequently derided as vultures, criminals, pessimists or un-Australian, in reality, shorting stocks is a stressful and often lonely way to make money in the market. When a fund manager makes the correct shorting decision, there are never glowing pieces in the financial press with a satisfied looking CEO pictured next to the fund managers that were smart enough to back their management team. Earlier this week we closed out one of our largest short positions in the Dividend Income Fund, a long-standing short in Seven West Media. In this week’s piece, I am going to look at the mechanics of closing out a successful short position (essentially buying shares on the ASX to deliver back to its original owner), along with the dangers of being too greedy.

A key component in short selling is knowing when to close out a short or in the words of the Gambler knowing when to walk away.

“You've got to know when to hold 'em, Know when to fold 'em, Know when to walk away and know when to run, You never count your money when you're sittin' at the table, There'll be time enough for countin' when the dealin's done”.

The Gambler by Don Schlitz 1978

In the case of Seven West Media, aside from being concerned about the dilutionary impact of converting preference shares held by a related party, in May 2016 the market seemed to be ignoring the weakness in the company’s business model, namely rising content cost and falling advertising revenue from declining free-to-air viewers. For Slater + Gordon the key catalysts identified were accounting irregularities and a mismatch between the reported profit and incoming cash flows and a very large and complicated offshore acquisition. In both of these cases we developed a valuation that was substantially below the current price along with some clear catalysts that could cause this fall to occur in the near future.

Knowing When To Fold Them

Knowing when to close out a short is more art than science and it is based on probability weighting the outcomes of going to zero versus rebounding after a big sustained fall. Investment research from the investment banks is generally near to useless for investors looking to close out a short as either a) the bank has ceased coverage of the stock, b) the company is still covered by the analyst who still has a buy recommendation despite the massive fall, as they are desperately hoping it will recover and they will keep their job or c) the analysis is far too negative and bitter towards the company that they believe has unfairly duped them.

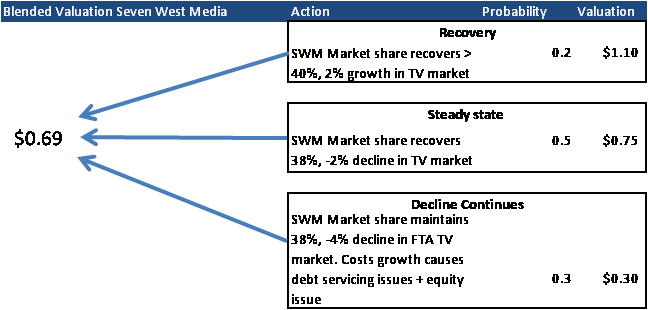

When these catalysts occurred in late 2015 for Slater + Gordon and in August 2016 for Seven West Media after the company reported that they expected 2017’s earnings to be down 15-20% due to higher costs and stagnant TV and print markets, the stocks both approached our initial valuation. In both of these cases the underlying problems were worse that our initial assessment, but based on this new information we then developed three new valuations based on a recovery, steady state and then a zero valuation upon bankruptcy. The above table shows the three valuations, together with a subjective probability weight that yields a blended valuation.

Folding Too Early

The above chart on the right for Slater + Gordon shows that we shorted the company in May 2015 at $6 per share and then bought the stock back at $1 to close out the position in December 2015. Whilst the stock has continued to fall in 2016 and our profit would have been greater had we held onto the stock; we were concerned in December that the bulk of the gains in shorting the stock had already been made and could not detect any Enron-style accounting fraud that would lead to imminent bankruptcy. Paradoxically you actually don’t want the shorted stock to zero as this creates administrative issues with the shorter having to negotiate an off-market transfer to obtain the equity needed to deliver the shares to close out the short position. With the stock currently trading at $0.35, in hindsight I was too cautious and insufficiently greedy.

Being too greedy

One of the dangers you face by being too greedy and not closing out a short when the bulk of your original thesis has played out is that either the price starts to rebound as it has become too cheap or that the sharp fall stimulates corporate takeover activity in the stock you have shorted. In both of these situations the short-seller is forced into the position of buying back the shorted stock at a time not of their choosing, thus contributing to upward moves in the share price, eroding profits.

The above situation of being too greedy occurred with a short position in global minerals testing company ALQ earlier this year. In late May 2016, ALS reported a poor result with earnings down 30% due to a downturn in minerals and energy testing, which saw the the stock fall -11% on the day of the result. After declining 30% over the past year ALS’s share price was now below our probability weighted target price. Anticipating the potential of further falls after investment bank analyst downgrades, the position was not closed out. Unfortunately, two days later ALQ received a bid from a private equity consortium, as we were concerned that this bid may presage a bidding war for the company with much larger European competitors, SGS and Intertek the position was closed out, albeit at a higher price.

Aurora’s View

Knowing when to close out a successful short position can be quite challenging, as the easiest option is to do nothing, drawing comfort from the negative news stories and research reports vindicating the fund manager’s initial negative thesis. However, in most situations (outside of an Enron or Onetel) there will be investors with interest in your shorted company at a certain price. It is far preferable to make a considered decision to close out a position early and move on, than be caught in a “short squeeze”. This occurs when a heavily shorted stock rises sharply in response to a small piece of positive news, as a number of short-sellers close out their position by buying back stock, thus causing further upward price momentum.

Contributed by Aurora Funds Management: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap & Praemium. Atlas' Australian Equity Income Fund (ASX:AFM01) provides quarterly income with low volatility. Click follow to be the first to get my next wire.

1 topic

3 stocks mentioned

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets