Where do stock markets go from here?

Matt Reynolds

Capital Group

Wild fluctuations in stock markets resulting from the coronavirus pandemic have tested the resolve of many investors.

“We saw markets drop more than 30% in a month, the quickest decline of that magnitude on record,” says Jody Jonsson, a global equity portfolio manager at Capital Group. “This is a truly global downturn that has impacted virtually every sector. It can be very disorienting, and I think the market is having a hard time sizing the depth and duration of the recession that is coming.”

With many areas of the global economy coming to an abrupt halt, markets have see sawed between gains and declines as investors weigh the potential impact of massive stimulus initiatives by governments and central banks.

So, where are the world’s stock markets headed from here? In a recent call from their home offices, Jonsson and equity portfolio manager Joyce Gordon, both veterans of numerous bear markets, shared their perspective on weathering the recession and positioning portfolios for the future.

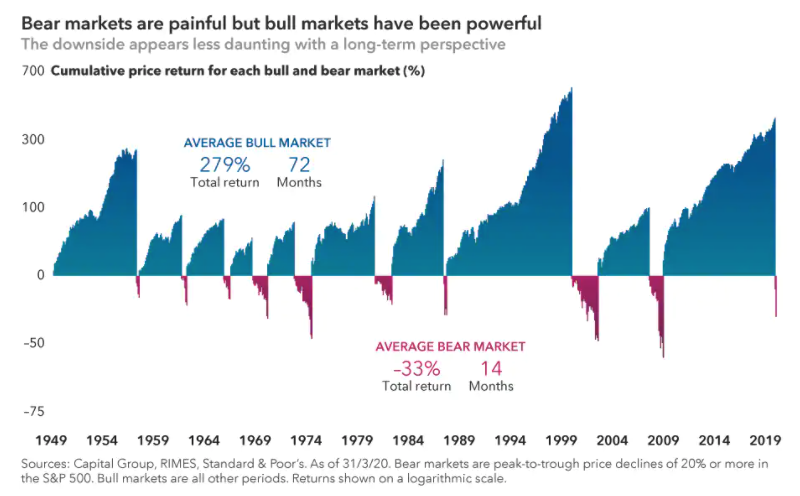

How long will this bear market last?

Jonsson: The recovery may go the way the virus has gone: from east to west. In fact, we can see that China’s market has started to recover already — down about 10% in the first quarter. Once the coronavirus case count levelled out, the market began to recover. I believe that will be the case for the U.S. and Europe as well. When does the curve flatten? As an investor I want to anticipate when those numbers will flatten. The key is to do what we always do: maintain our focus on the long term. It can be very difficult in times like these to look past the next few days. To the extent you can stretch your time horizon to months or years, I think that helps put you in a position to capitalise on the best long-term investment opportunities.

Gordon: I have experienced a lot of bear markets over my 39-year career. Each is different, but there are clear similarities: It always feels horrible when you're in the middle of it, but we have always come out the other end okay. It is very difficult to determine the precise timing of a recovery — sometimes the market bounces and recovers very quickly. That said, while I am hoping for a V-shaped recovery, I don't expect it. I expect a U-shaped recovery that will take some time and be highly dependent on the tapering off of new virus cases.

Are you making changes to portfolios during this difficult period?

Jonsson: I'm thinking about my portfolios in three buckets. The first includes companies I think will be largely unchanged or helped by current conditions. Examples could include certain medical device makers or tech stocks that are supporting the worldwide increase in internet use – a trend that is likely to remain even when the virus wanes. The second are stocks that were hit very hard initially, but that I do not believe will suffer long-term damage. Some of the larger payments companies might be in this category. In those cases, I will look for opportunities to add to my positions when the stock prices are sliding. The third bucket includes companies and industries that might be more structurally impaired if this goes on for a while – think some travel-related companies. With those, we want to try to determine how long they can sustain themselves with very low or zero revenue.

Gordon: We've been more active than usual during this period, selling some securities that we feel will have a lot more downside and buying those that we believe have been unduly punished. I'm developing a list of what I consider excellent companies that we may have a rare opportunity to invest in at 3% or greater dividend yields. If markets decline further, I'll look for opportunities to put cash I’m holding to work. I'm looking for companies where the revenues will be okay going through this and that would include some food companies, for example, and some utilities look interesting. And I will focus on companies with relatively low leverage. I tend to be a defensive investor, so I plan to be very cautious until I see signs that we are through the brunt of this. At that point I will look to invest in companies with more exposure to a recovery. For example, some of the aerospace and defence contractors might be attractive on the other side of this.

Given the global nature of this crisis, how will multinationals be affected?

Jonsson: Multinational companies have faced serious challenges over the past year or so, starting with the trade war. A lot of investors expected these companies would be disadvantaged by their exposure to China, but we found that multinationals have tended to be resilient. Today many global companies have strong balance sheets and cash flows, as well as access to credit, which is particularly important in today’s environment. Smaller companies may find they don't have as much access to liquidity. Coming out of this, we may see some industries become more consolidated as the strong get even stronger because of their flexibility and better access to resources.

I do expect companies to rethink their supply chains and dependence on China as they seek to become more resilient. When companies maximize their efficiency to boost margins, they often find they have thinner margins for error, which is a problem in this environment. I think we're going to see companies managing themselves with a bit more flexibility, a bit more redundancy, multiple suppliers and multiple locations.

We may see an industrial renaissance in the U.S. as companies seek to become more resilient coming out of this. We've already seen the early stages of this trend in technology, with companies like Taiwan Semiconductor, for example. But now we're also starting to see it among pharmaceuticals, as many of the key compounds for therapies are made only in China.

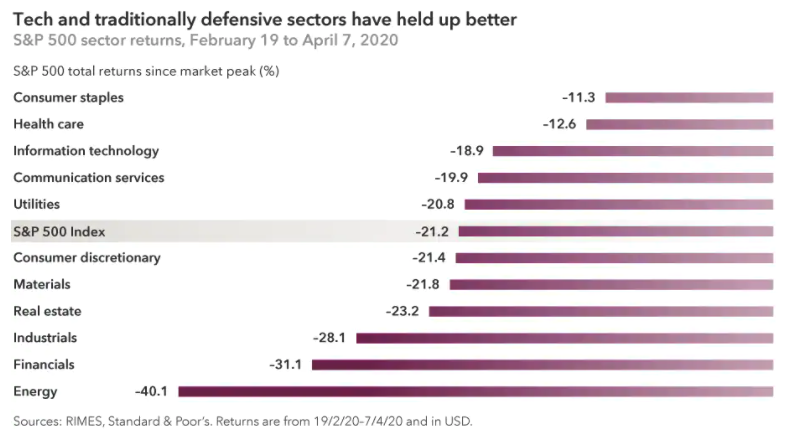

How are defensive areas of the market holding up?

Gordon: Traditionally defensive investments have generally held up well, but there are exceptions. Energy, one of the higher yielding sectors, has been the hardest hit in this decline as it has faced both supply and demand shocks. We had an economic slowdown that's hurting demand for oil at a time when Saudi Arabia and Russia couldn't agree on production cuts and began flooding the market with oil. On the positive side, companies in consumer staples, health care and some defence contractors — those companies whose revenues tend to hold up better during recessions — have also stood up relative to the broader market.

Within sectors, we are seeing that companies with strong balance sheets and low debt have been less impacted than companies with higher leverage, which we expected. Before the news of the coronavirus, I was already focused on dividend-paying companies with lower leverage and strong free cash flow. Companies with excessive leverage may be at risk of cutting dividends.

We've seen many companies either cut, eliminate or suspend their dividends in today’s extreme environment. Some are doing this out of an abundance of caution to make sure they have ample cash to weather a difficult period. In other cases, they may face pressure from rating agencies or governments, as has been the case recently in France. We're likely to see more dividend cuts so we are working hard to try to anticipate them.

What sectors are likely to lead us out of the downturn?

Jonsson: Tech isn’t usually defensive, but in the current downturn some leading technology companies like Amazon have acted somewhat defensively because they are benefiting from physical distancing and stay-at-home policies. What's been particularly noteworthy to me is that it hasn't just been cheap stocks that have held up. For example, I own a European medical equipment maker that was recently trading at over 40 times earnings. Because the demand for its products is so steady and repeatable, the stock price has not moved much during this period. And so I am looking at the resilience of businesses rather than just what I'm paying for them as a guide to what might be defensive if this drags on. If we avoid a prolonged recession but enter a period of slower growth because there will be greater government debt, I think such growth companies may still do well in that environment.

Gordon: Health care stocks have also held up relatively well. A lot of these companies have the opportunity to develop a drug that might combat the coronavirus, while others are gearing up to make much needed testing equipment. And, given the crisis that we're in, I expect less pressure from Congress on drug pricing. So I believe US drug companies may do well from here. Companies that make devices for knee or hip replacements, for example, will likely get temporarily cut back, as many of those surgeries will be postponed. But I don't think demand goes away; it just gets pushed off and they look better perhaps a year or 18 months from now.

What can investors do to keep calm during this period?

Gordon: Try not to look at the market every day. That can only amplify anxiety. Times like this can be unnerving, but remember that the stock price only matters when you buy and when you sell. Remember that while your clients may feel hopeless because they are doing nothing, there’s a lot happening behind the scenes as we look for opportunities to upgrade portfolios and test the resilience of the companies in which we are invested. We have a lot of resources, including a great team of investment analysts in markets around the world who have deep experience. For example, we have health care analysts who have previously worked as doctors and I believe are the best in the industry.

Jonsson: There is so much anxiety and fear in the market, and I think it is important to lean the other way when sentiment gets lopsided. With negativity so high, I'm trying to allow for the possibility of positive surprises. Maybe the current situation isn't quite as bad as it seems, or maybe we solve this. Maybe good old-fashioned scientific ingenuity comes up with some great solutions. But most importantly, don't lose sight of the long term and consider this downturn an opportunity to invest in some great companies at attractive prices.

Position your portfolio to navigate through cycles

Capital Group believes in a smarter way of investing that combines individuality and teamwork into a tailored approach to help investors meet their goals. Find out more by clicking 'CONTACT' below

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The University of Sydney. He also holds the Chartered Financial Analyst designation. Matt is based in Sydney.

1 contributor mentioned

Matt Reynolds

Investment Director

Capital Group

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The...

Expertise

Matt Reynolds

Investment Director

Capital Group

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The...

Expertise

Comments

Comments

Sign In or Join Free to comment