Who will pay?

Mark Todd

Bank of China

As everyone ponders how all economies move into the next phase of Covid-19 - some in the financial markets are starting to think about, how are the shutdowns going to be funded and what will need to be funded?

There is no doubt that most Governments of the world took drastic action to protect their citizens and any cost of that protection was not considered at the time. This was an entirely appropriate response, but it will have dramatic long term implications.

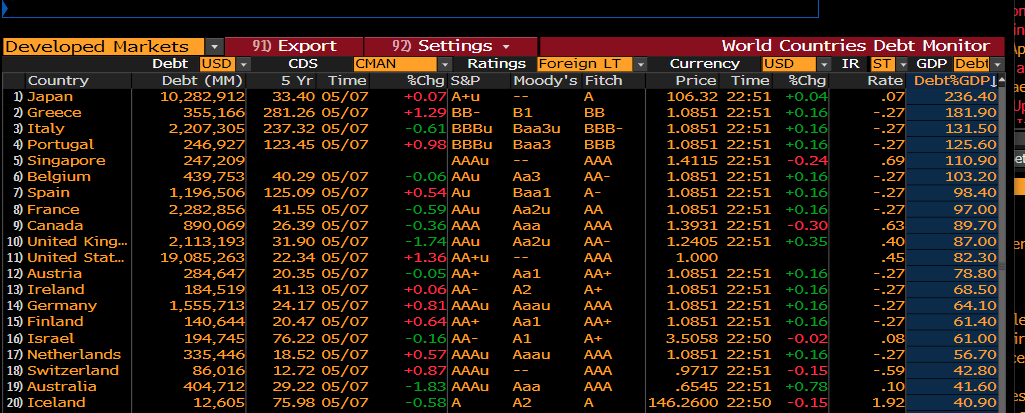

To assess, first, let’s look at the various starting points. How much debt did countries have at the start of the crisis?

The last column on the Bloomberg table below (Figure 1) compares debt-to-GDP across developed markets.

Figure 1: source: Bloomberg

These number are enormous … and they are the starting point.

As a global borrower, it is important to know who owns your debt and why do they own it?

In the case of Japan, ranking number one on the Bloomberg table, - a vast percentage of their debt is owned by locals, either citizens, or institutions, whereas in Greece, coming in second, the debt profile was owned by hedge funds and institutions, which caused much heartache for the Greek people.

What next?

All governments will need to issue debt to fund their obligations to their citizens. When you read “citizens” intellectually substitute the word “voters”, because the present crisis might be a circumstance where “I vote, I need work” could be the next bumper sticker.

In order to imagine how governments can respond to voter concerns, it might be best to understand what they themselves will be dealing with.

Debt to GDP is the countries’ debt (numerator) as a percentage of GDP (denominator). What should analysts assume the denominator will look like for 2020? What about even 2021 right through to 2025? There are over 30 million unemployed in the US in one month.

Who can, with complete confidence, decide what the GDP will look like for any country?

The employment numbers will rebound as economies open, but the reality is that no one really knows at what velocity; what will the bounce in activity look like? Will consumers consume, comfortable that all will be good, no recurrence in pandemics, and that companies will continue to put employee and customer welfare before profits?

I think it is reasonable to presume the denominator will struggle to grow for the foreseeable future, remembering for most investors a month can hold a lifetime of investing experiences, so a five year horizon is the equivalent of a Star Trek light year.

The numerator

This is where the rubber really hits the road because we have been told by Treasury what to expect for upcoming issuance.

The US Treasury announced on 6 May, that its funding requirement for the next quarter is $96 Billion, for one quarter! By President Trump’s own estimate they have the economy contracting this year by 40%; the American deficit will groan onwards to $4 trillion. These numbers are easy to write but nearly impossible to comprehend.

As you try to imagine the size of the US financial commitment - then overlay it, with the needs of Europe, Japan, China, Latin America and the rest of the world.

Why does funding deficits matter?

America, particularly under Donald Trump’s leadership, is not a “cap in hand” borrower. There seems to be very little diplomacy. Think back to the GFC and then Treasury Secretary, Hank Paulson flying to China to assure the Chinese investors that Fannie Mae and Freddie Mac would redeem their debts even if the government had to step in. Fannie Mae and Freddie Mac are the funding entities that provide funding for mortgages in the US.

There is no evidence on the surface that America recognises that it might have any challenge funding $4 trillion in debt … remember those debt ceiling arguments during the Obama Administration?

If there is an investor boycott in any form, then we could see a significant steepening of the bond curve … “Houston, we have a problem!”, America will either cut spending, hurting voters, or raise taxes, hurting voters and companies, or pay the higher coupon on the bond and hope the economy rebounds, which is assuming a very weak US Dollar.

I don’t like any of those strategies and this is all based on the assumption that $4 trillion is enough to kick start an economy that wasn’t increasing in headline revenue prior to the Covid-19 pandemic.

What do investors do?

Australia is not in as precarious a situation as most other countries, as Figure 1 highlights.

I don’t provide advice, personal, investment or otherwise. With these circumstances, I can see a situation that investors may need to take different risks where cash rates are so low predominantly in the short end. Investors who decide to buy long dated government bonds will have revalue risk. The theory is if rates go higher after you invest, there will be a capital loss if you sell that bond in the market. This is a critical issue for fund managers, but if rates in the short end go to zero or lower, then that is a critical issuer for savers.

Therefore, it could be valuable to decide if a part of your portfolio is dedicated to income, and if so, is there a long-dated bond that can meet your requirements?

Again on the premise that I don’t provide any advice, but discern as a keen observer, I would watch to see how markets are responding to the increased issuance - and if you can achieve a compelling rate taking Australian government risk, then it is at least worth exploring through your own independent research or via a fund manager.

Mark Todd

Head of Fixed Income, Bank of China

Bank of China has a commercial interest (in the assets) printed in this article.

Bank of China does not provide investment or personal advice.

Investors should seek its own independent and appropriate advice that is suitable for their investment needs.

Get investment ideas from industry insiders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Mark joined Bank of China in 2019 as Managing Director and Head of Fixed Income Sales, bringing with him over 25 years’ experience in FICC Sales. Prior to joining BOC, Mark was Head of Core Customers within NAB’s FICC Sales division.

Mark Todd

Head of Fixed Income

Bank of China

Mark joined Bank of China in 2019 as Managing Director and Head of Fixed Income Sales, bringing with him over 25 years’ experience in FICC Sales. Prior to joining BOC, Mark was Head of Core Customers within NAB’s FICC Sales division.

Expertise

Mark Todd

Head of Fixed Income

Bank of China

Mark joined Bank of China in 2019 as Managing Director and Head of Fixed Income Sales, bringing with him over 25 years’ experience in FICC Sales. Prior to joining BOC, Mark was Head of Core Customers within NAB’s FICC Sales division.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions

Equities

How to invest $100k for growth

Livewire Markets