Why aren't rising rates hitting gold?

Gold is holding up despite an environment of rising bond yields that are traditionally a headwind for the metal. With this relationship breaking down, we look at what is supporting gold, and nominate our preferred exposures in the sector.

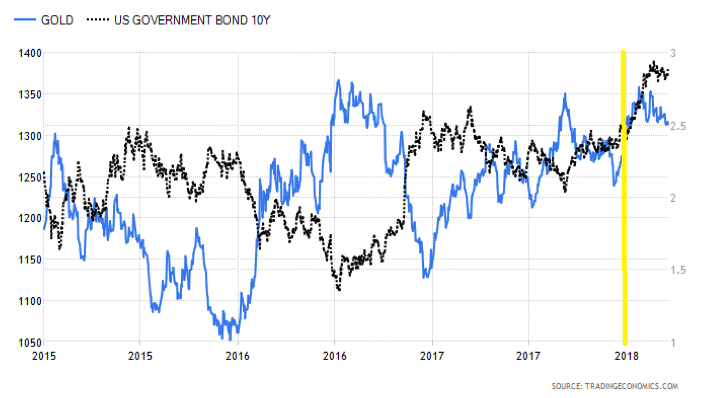

Bonds and gold's inverse relationship breaking down

As illustrated in the chart below, a strong inverse correlation emerged between gold and the 10-year US Treasury bond price from the start of 2015 until the start of 2018. In recent months, however, these dynamics have clearly shifted with the inverse correlation between treasuries and gold showing signs of breaking down.

In the United States the announcement of corporate tax cuts and infrastructure spending packages will likely see the budget deficit blow out from 3% to 5% at a point where the US economy is at full employment. This unprecedented move has stoked fears of a blow out in wages and inflation, causing bond yields to move higher. However, despite rising bond yields the gold price has remained fairly resilient.

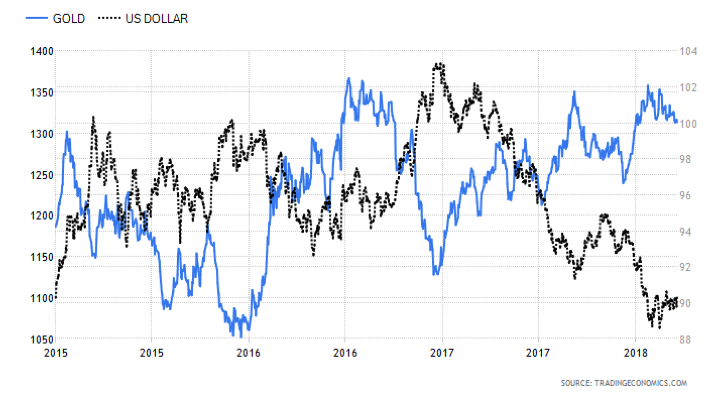

US Dollar now key driver of gold?

With the decoupling of the gold price and bond yields, it appears the US dollar has become the key driver of price. An interesting piece of research by Macquarie looks at the performance of the gold price during US dollar bull and bear markets dating back to 1980. What was found is that in months when the US dollar rises, for every 2.0% increase, the gold price on average declines 1.1%, while for every 2.0% decline in the US dollar, the gold price rises 1.3%.

Since October 2017 there has been a clear shift in investor willingness to take on risk, which has seen the US dollar take on the role of a risk currency. When global growth is synchronised and strong, it’s not uncommon for money to flow out of the United States and into areas such as emerging markets, placing downward pressure on the USD in the process.

It therefore appears that at this stage the negative effects of rising bond yields on the gold price are being at least partially offset by the positive effects of a weakening USD.

Where to next?

The key question for investors going forward is what is the likely direction of the gold price from here?

Movements in the gold price are notoriously difficult to predict, with the proverbial streets lined with the graves of countless price predictions made by esteemed commodity analysts and research houses alike.

There is a strong agreement that the recent spate of synchronised global economic growth is reaching a peak, that’s if it hasn’t peaked already. Despite a strong jobs market, US GDP forecasts have been revised lower, European data has been noticeably softer, while the Chinese authorities continue to prioritise sustainable and environmentally conscious growth.

On the political front and geopolitical tensions appear to be rising, whether it be related to the Russian Spy saga, or threats of Tariff wars. Additionally, the upheaval inside the White House over recent weeks has also been conspicuous.

With signs that global growth is decelerating and political tensions rising, we have seen the USD stabilise, a sign that investors are starting to feel less optimistic about the global outlook. Notably though, this recent period treasury yields have remained fairly stable. For an investor in gold, a stabilisation and eventual reversal in the USD is a key downside risk, particularly if the reversal coincides with a period of stability (or increase) in bond yields.

Our preferred exposures

When scouring the market for gold producers we prefer to break them into a couple of sub-categories based on those that produce domestically and those that produce overseas.

In the present environment, as a general rule, we’d prefer to hold Australian based producers who incur their costs in AUD and sell the gold in USD. There are numerous gold producers in Australia who hold assets in places such as Papua New Guinea and Africa. These miners not only have greater sovereign risk, but they tend to incur their costs in USD as well as sell the gold in USD, therefore failing to benefit as much from a declining AUD.

A couple of gold producers that meet the criteria in our eyes are Northern Star Resources (NST) and Evolution Mining (EVN).

Both Evolution and Northern Star possess very strong balance sheets with manageable debt levels and significant cash reserves. As low to medium cost producers with high grades, these businesses are in a strong position to leverage off a rising gold price should that transpire. Both have performed very well for clients in recent years, however given the aforementioned reasons for being cautious on the outlook for gold we’d be looking to reduce positions and lock in at least a portion of profits.

Our conclusion is that despite a seemingly favourable political backdrop for gold, we don’t think political tensions are significant enough at present to offset the economic backdrop of stable (or rising) bond yields, coupled with a stable (or rising) USD. So, for the moment, we are therefore reticent to take new positions in the underlying gold commodity, ETF’s or gold producers. For those investors looking for gold exposure, we tend to limit exposure within a portfolio to 5%.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

1 topic

3 stocks mentioned

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

Expertise

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

Expertise

Comments

Comments

Sign In or Join Free to comment