Why is no one talking about Junk Bond spreads?

In our last post on March 4th this year, we discussed a number of important points as to why we had decided to take our fund to 90% cash. An article that with the passage of time, in less than one-month in-fact (feels much longer than that), has aged incredibly well.

To make it clear, we did not forecast at all what has actually occurred. 2020 will go down in the history books already, and its truly concerning to think that we are still only at the beginning of all of this. Frightening even.

Our savior at the time when talk of the virus was still quite 'benign', was that everyone seemed to be guessing (nothing has changed to today mind you) as to the extent this virus could impact the world - which ranged from quite low in term of its impact, to severe, but with no-one in their right mind suggesting what has actually eventuated. All we knew at the time was that based on 20 years in financial markets, the risk-reward balance felt very unhinged given possible broad-based impacts on company earnings and the fact that the bond market was cracking. On that basis, we were out!

Thankfully therefore we have managed to side-step this bear market, and as a quick update to our positioning, we have actually taken the fund to 100% cash. We are now in the most-fortunate of positions to have suffered a peak draw down of less than 4% and are actively looking to be a net-buyer of risk-assets in the future.

But not yet.

For us to be a buyer of equities, we are of course watching a number of data points closely. A number of those are being discussed here on Livewire and elsewhere daily. We wont attempt to go over that work again.

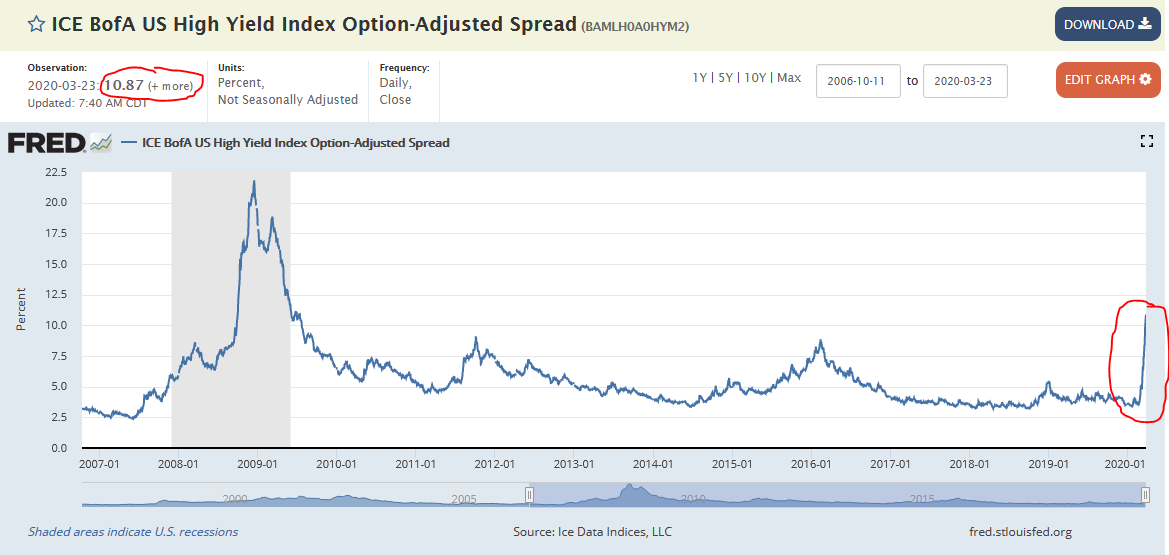

One of the data points we are watching like a hawk which is getting little air-time, but one of vital importance for equities are junk-bond spreads (VITAL!!). As I type, the latest update from the St Louis Fred show junk-bond (high yield) spreads have spiked to 10.87% as at 23/03, as shown below;

Source: (VIEW LINK)

To put into perspective just how violent this move has been, at the start of 2020 when COVID19 was not even mentioned in the news cycle, spreads were just 3.5%.

To this point, the current market is seeing the highest spreads outside of the GFC, even besting those experienced during the tech-wreck. That's probably worth repeating - the current market spreads in High Yield bonds are the highest they have ever been outside of the GFC... To rub salt into the wound, they continue to go vertical almost daily despite the huge government intervention into the market.

Junk spreads which directly impact the yields businesses can borrow at are now at levels which effectively mean the high yield market is shut down. We feel this is an important consideration for equities (which nobody seems to be talking about!) as they are effectively the same as 'equity' on the capital structure. Hence if junk bonds are showing extreme stress, which they are and continue to do so, equities will also highly likely continue to follow suit.

Why you ask? Well thats because junk bonds tend to act more like stocks in their market behavior than other bonds. This is because the strength of junk bonds is connected to the strength of the company that issues them.

In short, while most bond investors focus on how changes in interest rates will affect the market price of their bonds, high-yield bond investors must also understand the default risk of the firm wanting to issue them in order to fund their business. Therefore, high-yield bond investors MUST understand how the company's financial performance will likely be impacted by changing economic conditions and how that could impact or increase the chance of the issuing company defaulting.

What this particular market is showing us right now is that the rapidly changing economic conditions are deteriorating so fast that the risk of company defaults is climbing in a seemingly uncontrollable fashion. This is despite the Governments massive intervention programs. Naturally therefore, this is still a very concerning time for equities as it is for all businesses with many of their operations having been 'shut-down' by governments all over the world.

Although therefore we are wanting to be a net-buyer of risk -assets going forward, we are not yet enticed and remain fully invested into cash, despite the last two days stock-market performance. Everywhere we look, there are 2nd, 3rd 4th order impacts rippling through the economy. Estimating a businesses earnings this year, let alone next is almost impossible right now. And that is why we continue to stand aside.

In such an uncertain business environment - it would be amazing if anyone reading this, if you are a business owner for example, a CEO - whatever your position, to share your stories. Thank you in advance if you do.

We are truly in unprecedented times.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

CIO, REQON Funds Management. 23 years Investment management. Delivering material market outperformance for investors.

CIO, REQON Funds Management. 23 years Investment management. Delivering material market outperformance for investors.

CIO, REQON Funds Management. 23 years Investment management. Delivering material market outperformance for investors.

Comments

Comments

Sign In or Join Free to comment