Witching hour for Cinderella stocks

We all know the story of Cinderella. Transformed into a glamorous princess, she was the belle at the ball. However, the celebration abruptly stopped at midnight, when her gown turned back into rags and her coach turned into a rotten pumpkin.

Growth stocks are sometimes like Cinderella, glamourous companies that can have their fashionable moments but can also quickly turn into poor investments.

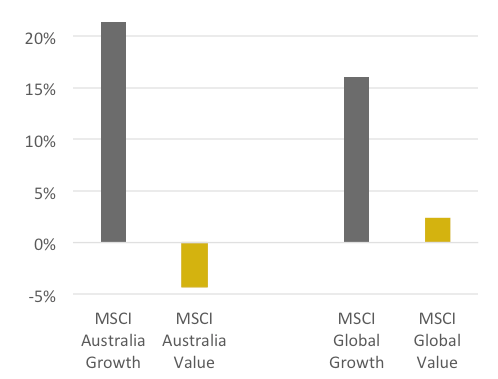

Over the last couple of years, growth has thumped value everywhere. And over the last year, this outperformance was most extreme in Australia.

Figure 1. Annual return of growth and value indices for Australia and the World (as at September 2018)

Source: MSCI

Paying up for high earnings growth is often justified by the fairy tale of strong companies in an environment of scarce earnings growth. However, seasoned investors know that growth and value styles are cyclical. They fall in and out of favour and it would be a mistake to assume one style dominates into perpetuity. Famous examples of growth stock euphoria that eventually reversed includes the ‘Nifty Fifty’ stocks in the 1970s and the technology stocks in the late 1990s / early 2000s.

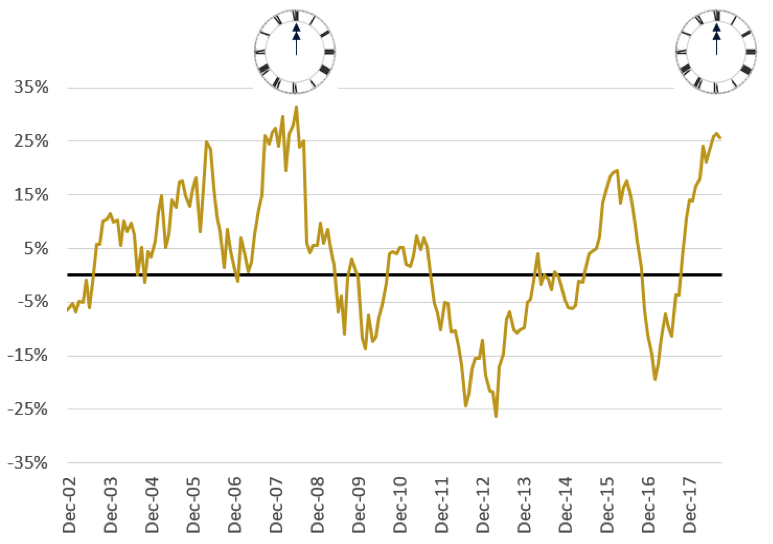

This mean reversion is especially evident when either style shows extreme outperformance. For example, Australian growth stocks peaked in 2007 and collapsed thereafter. Today, it looks like history is repeating and the clock has just passed the witching hour for Cinderella stocks.

Figure 2. Rolling annual return (MSCI Australia Growth minus Value)

Source: MSCI, Vertium

The reason for this cyclicality is that when share prices are extremely high for either style they provide no margin of safety for any bad news, irrespective of company strength or outlook.

CSL: Australia’s growth bellwether

As a business, CSL is an excellent company because over a long period of time management reinvested aggressively (research and development spend of 10% of revenues with a 45% dividend payout ratio) in a business that generates high return on capital (about 35% ROFE over the last five years).

This has resulted in the company delivering a long runway of rising earnings and a share price to match. With its proven track record and a robust earnings outlook, CSL takes the crown as Australia’s premier growth company.

While CSL’s business case is robust, its current investment case may be on shaky ground.

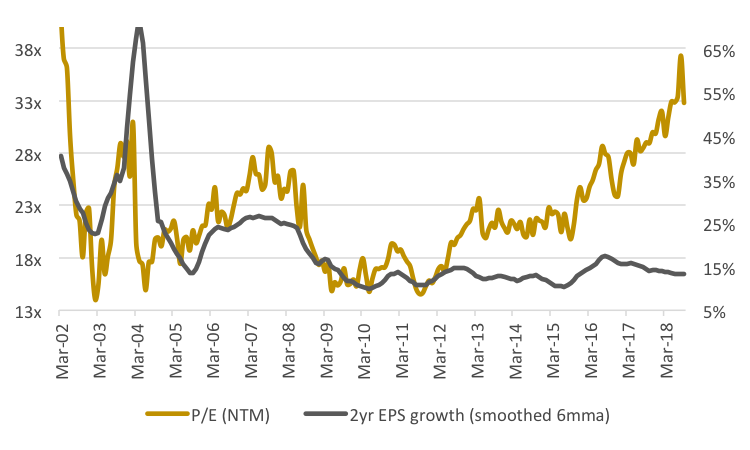

Growth stocks certainly deserve higher valuation multiples because they deliver greater earnings growth. This is evident over CSL’s history. Over the last seventeen years the variation in its price to earnings (PE) multiple roughly matches the variation in its forecast earnings growth over time. When forecast growth was higher, its PE was higher and vice versa.

Figure 3. CSL’s PE multiple vs its 2-year earnings growth forecast (March 2002 – September 2018)

Source: Factset

However, the relationship between CSL’s valuation multiple and forecast earnings growth has disconnected since early 2017. To make this observation clear the following charts give pause for thought.

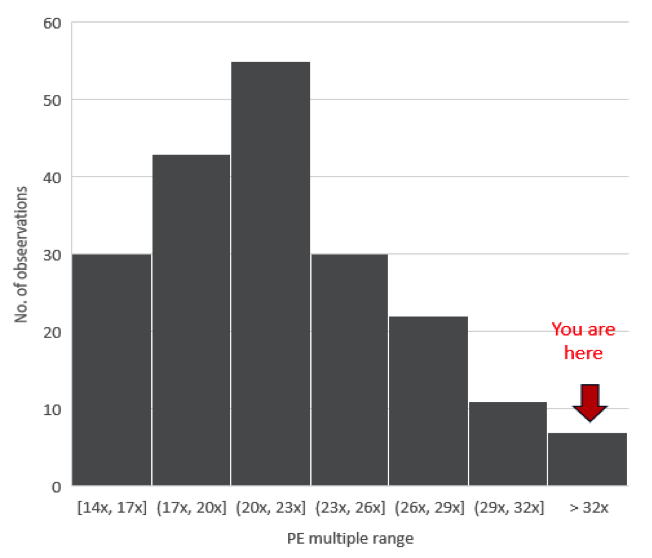

Figure 4 shows the history of CSL’s PE multiple at the end of each month between March 2002 and September 2018. For the majority of the 199 monthly observations, CSL traded on a PE multiple of between 20x and 23x. And rarely does it trade above 32x (just 7 out of 199 months).

Figure 4. CSL’s PE multiple history (March 2002 – September 2018)

Source: Factset

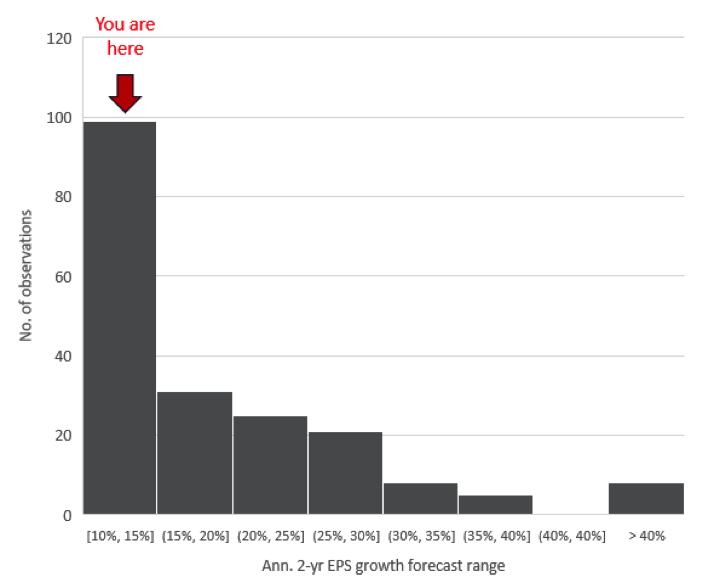

Figure 5 shows the number of observations of CSL’s earnings growth forecast at the end of each month between March 2002 and September 2018. Despite CSL’s PE multiple peaking at 37x in August 2018, its forecast earnings growth is at the lower end of its historical range of 10-15% per annum.

Figure 5. CSL’s history of 2-year earnings forecast (March 2002 – September 2018)

Source: Factset

The last time CSL traded more than 30x PE multiple was back in early 2002 when it justifiably matched its two-year earnings growth forecast of greater than 30% per annum. If the fifteen years prior to 2017 is a guide, CSL’s lofty valuation multiple will eventually mean revert to match its earnings growth rate.

Watch out when witching hour approaches

Most so-called Cinderella stocks will turn into ordinary investments. Only a rare few will thrive in the long term but, nevertheless will experience many trials and tribulations along the way.

For example, CSL has seen nasty drawdowns in the past from elevated PEs that can shake out the most patient investors. From 2001 to 2003, its share price lost 76% from peak to trough. It took several years to recover the losses but a decade later the company is one of the most celebrated Australian growth companies.

The challenge for investors is that for every true Cinderella, there are hundreds of wannabes - ugly stepsisters trying to force themselves into your ‘glass slipper’ portfolio.

And if you think you found a true Cinderella, are you able to tell when midnight approaches and valuations reach extremes?

If not... be prepared for large drawdowns and hope your fairy godmother shows up to conjure the happy ever after.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

1 stock mentioned

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Comments

Comments

Sign In or Join Free to comment