LWE - 28th Aug, 2021

Zip soars, APT idles, ahead of a 'big growth runway'

Mia Kwok

Livewire Markets

Whatever you may think of the buy-now-pay-later (BNPL) space, investors cannot get enough of the growth story behind market favourites Afterpay and Zip.

The two competing BNPL companies both reported their full-year results today and despite a lopsided balance sheet, investors have been largely optimistic about the report.

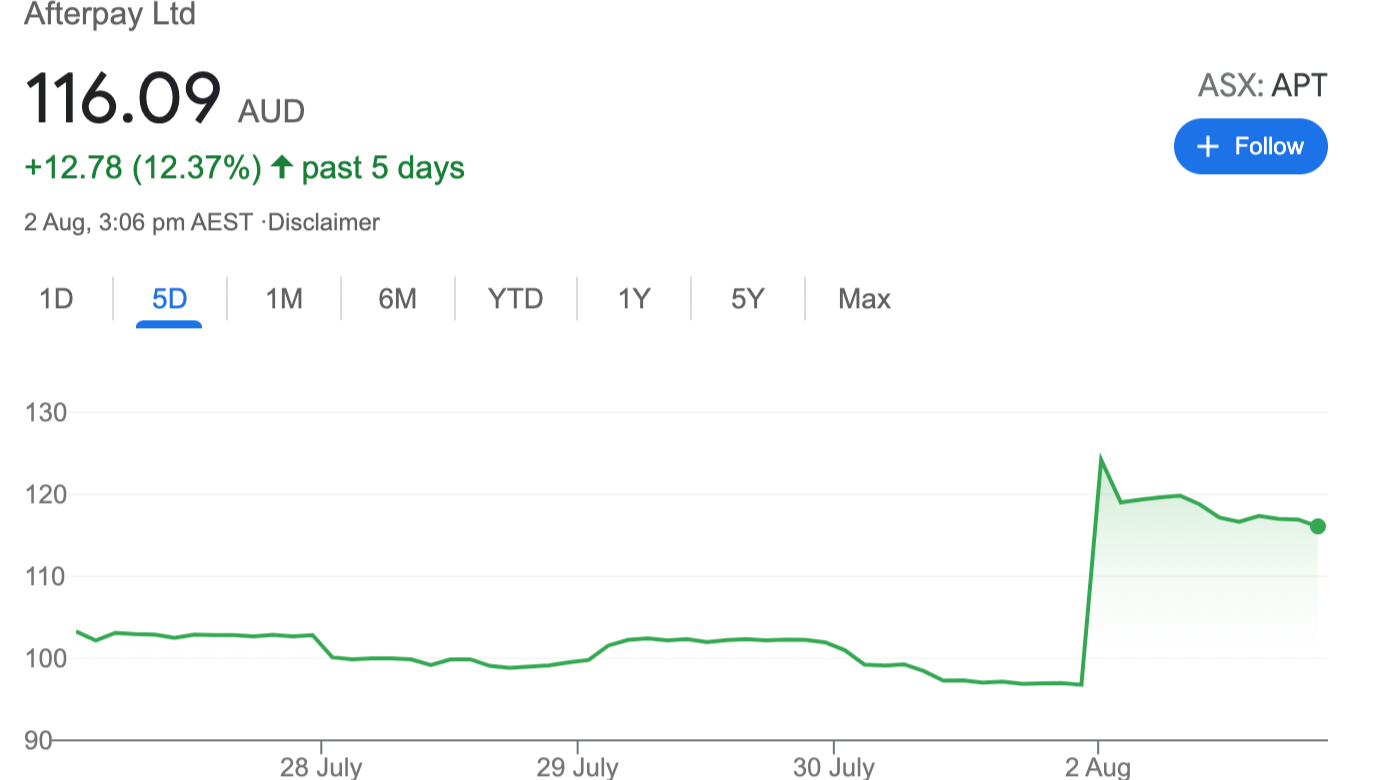

After taking a morning dip, Zip (ASX:Z1P) is up over 6% from its intraday low. Afterpay (ASX:APT) has fallen less than 1 per cent by midday today, however, leading analysts have attributed this to Afterpay's upcoming acquisition by Square, rather than any reporting season trading.

I spoke with Jun Bei Liu, portfolio manager of the Tribeca Alpha Plus Fund, to gain insight into today's results. She gives a rundown of why the boosted expenditure (read: big losses) is a good thing for both Zip and Afterpay as they race to gain US market share.

She also gives a look behind the curtain on the Square deal and why Afterpay's share price was sluggish today, despite positive news.

"Buy Now Pay Later has been a very exciting high growth innovative space, and we have believed in it for so long. I think from here on it is still a very exciting journey" said Liu.

First up, here's the overview:

Z1P by the numbers:

- 150% YoY increase in revenue to $403.2 million

- 248% YoY increase in active customers to 7.3 million customers; 109% YoY increase in active merchants to 51,300 merchants.

- 179% YoY increase in transaction volume to $5.8 billion

- 293% YoY increase in transaction numbers (largely driven by the US) with 41.3 million transactions

- 147% YoY increase in cash gross profit to $198 million

APT by the numbers:

- 90% increase in underlying sales to $21.1 billion

- 63% increase in active customers to 16.2 million; 77% YoY increase in active merchants to 98,200 merchants.

- $156 million loss in FY21 compared to $20 mill in FY20

- 104% increase in operating expenses (including marketing and other operating expenses)

- Weak EBITDA with a 13% decrease to $38.7 million

Losses aren't phasing Liu

"For Zip, its 4Q21 results did come through with higher than expected losses. That's mainly because of increased operating operational expenses that affected the profit somewhat. But it's in line with expectations," said Liu.

Much of the expenditure went towards global expansion into the necessary US market, which has paid off handsomely for Zip.

"It's all very impressive," said Liu.

"You know US revenue is annualising at $260 million -- and that's very impressive. One encouraging thing is that the US customers are transacting much more frequently, which has been expected, but still, it's very, very positive," she said.

Spend now, spend later: the marketing race

One of the headline figures from both Zip and Afterpay has been the large year-on-year increases in operating expenditure. For the most part, this has been a marketing spree by both players. Afterpay reported a 104% increase in operating expenses (including marketing and other operating expenses) with nearly $300 million in expenses reported for the financial year.

"I think it comes down to the competitive nature of the industry - especially this industry," said Liu about the marketing blowout.

"For the newer markets, you have to spend because it's about scale. It's about the ecosystem and for every customer you add to it, the customer spends more over time, and they stick with the ecosystem," she said.

"So I think it's incredibly important to keep spending, and in an environment where there are many other players starting as well (especially some of the large players) you've got to stay ahead of the competition," she said.

No doubt this market is competitive. Klarna is already a large player internationally, partnered locally with Commonwealth Bank. While Apple Pay and Paypal have recently announced a similar BNPL product suite that caters to the same market -- but with the added sticky factor of a large, loyal existing user base.

"Scale is incredibly important and valuable. So, I don't think you can say marketing spend will come back in the next few years, just simply because of how much growth there is and how much tough competition is coming in as well," she said.

Afterpay can't think outside the Square

Afterpay had a number of good announcements this reporting season, including a huge diversification strategy for its revenue base. But investors were largely unmoved, and this has been put down to Square.

Normally acquisitions present a good opportunity for investors, but Afterpay's share price growth trajectory is being hampered by the US conglomerate Square. The takeover was announced earlier this month a provided a short-term boost to APT investors and is due for completion early to mid-2022.

"The Afterpay share price reaction is somewhat linked to Square's price over in the US. Now Afterpay gives us quasi-NASDAQ exposure," said Liu.

Today, Afterpay announced its new product: Afterpay's in-app advertising for its direct-to-consumer website and app. The website reported receiving 15 million clicks in December alone - the Christmas trading period - which directed consumers to retail products, said Liu.

"It's very different proposition but perhaps in a way will de-risk Afterpay in terms of regulatory risk," said Liu.

The new advertising service could be a huge revenue booster for Afterpay, or at the very least helps to diversify the platform away from its regulation-risky BNPL product.

According to Afterpay, early testing has shown an average 20% lift in sales for advertisers using the Afterpay app.

Afterpay also reported a decreased reliance on late fees, which to date has been an incidental part of its revenue strategy.

But it might take investors a little more oomph to get them over the line with the looming takeover. Afterpay is still trading at about a 6-7% discount on the bid price, said Liu.

For investors looking to get a piece of the Square-pie, Liu also indicated that there are plans to list Square in Australia by the end of the year, which could be something to look forward to.

Conclusion

The high-growth ride isn't over for Afterpay and Zip, said Liu. There is still a big growth runway as each seeks to tackle the US market. Don't be dismayed by marketing figures - that's the nature of the beast.

"Ultimately, I think these are very high growth businesses and they speak to the opportunity in those new markets in the US. So, there is an incredible amount of opportunity coming out of those areas even though there will be increasing marketing spend," said Liu.

"But the opportunity, the addressable market opportunity is real, and it has been tested by others. So that's why you know you can put a higher probability of them capturing some of that market share."

Related articles:

Equities

Why Square's $39bn bid is only the beginning for Afterpay

View

Equities

From disappointment to delight: Why Hyperion's holding its Afterpay shares tight

View

Equities

Beyond Afterpay, who are the next ASX fintech dazzlers?

View

Never miss an insight

Enjoy this wire? Hit the ‘like’ button to let us know. Stay up to date with my content by hitting the ‘follow’ button below and you’ll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Mia Kwok is a former content editor at Livewire Markets. Mia has extensive experience in media and communications for business, financial services and policy. Mia has written for and edited several business and finance publications, such as Business Insider, Superfunds Magazine and Urban Icon.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

1 topic

2 stocks mentioned

1 contributor mentioned

Mia Kwok

Editor

Livewire Markets

Mia Kwok is a former content editor at Livewire Markets. Mia has extensive experience in media and communications for business, financial services and policy. Mia has written for and edited several business and finance publications, such as...

Expertise

Mia Kwok

Editor

Livewire Markets

Mia Kwok is a former content editor at Livewire Markets. Mia has extensive experience in media and communications for business, financial services and policy. Mia has written for and edited several business and finance publications, such as...

Expertise

Comments

Comments

Sign In or Join Free to comment