3 predictions for the remainder of 2020: this week in capital markets

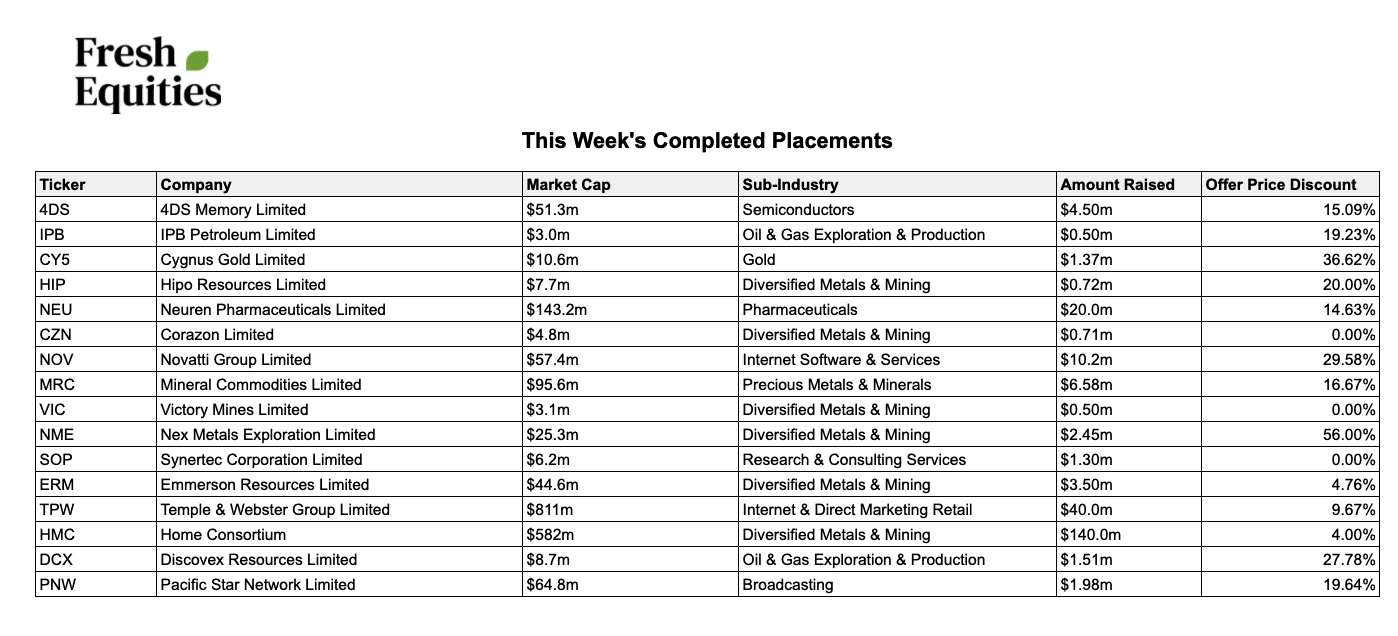

$235m was raised during the past week across 16 deals. Not a lot to sink our teeth into and a far-cry from what we saw when the COVID raising-spree began. The end of the financial year put the brakes on most significant corporate activity for Monday/Tuesday, reporting and the like taking up the market's time. The back-end of the week saw an increase in activity, but it was mostly smaller deals coming forward.

The most notable event this week was the Temple & Webster raise. In a similar style to Kogan (and with the same broker in their corner), the online furniture darling tipped their hat to investors for a $40m placement. This was a good time for Temple to raise. They already have ~$29m in the bank and it's been a great few weeks of trading. The company has been benefiting primarily from a wave of newly-isolated Australians jumping into home decorating and looking for a COVID-friendly way to buy furniture. As we've highlighted previously, more and more raises are being earmarked for growth. This certainly wasn't a survival raise, Temple wants to use their new momentum and war chest to explore "organic and inorganic growth opportunities". The deal was promptly covered and resumed trading with the sort of momentum you'd expect of a bought deal. Unfortunately there wasn't any love for small/medium sized shareholders via an SPP or pro-rata issue, and we hear that even institutions were heavily scaled in the placement.

Looking onward - we're in a new financial year now. It's unlikely to be as turbulent as the last one, but will certainly not be back to normal. There'a a US election later in the year, COVID still banging on the door, and lingering recession fears. Here's what we think will transpire in capital markets.

1. More deals, but smaller deals

The second half of the year is usually when we see the majority of deal flow, for obvious reasons this year has been a bit of an outlier...

The first six months of 2020 saw 429 deals completed. This is more than we saw in either half of 2019 - for reference, there were 253 deals in H1 2019 and 405 in H2 2019. This suggests that there is still more to come. We believe that there is a growing list of small/mid cap companies that are waiting for the right time to hit the market. These raises tend to do better in times of high investor confidence, so we suspect that these deals will start to appear alongside a sentiment rebound.

Don't expect as many large cap raises. It's become a pastime for equities analysts to speculate on the next top 200 company to require capital - and there's a long enough list. But unless we see another dip in the market, these deals will appear slowly and continue to be for executing growth plans.

2. Expect quiet periods

With EOFY, reporting season, and bank covenants not due to be tested until December there will be quiet periods - we expect August to be one of them. Last year August was down 20% on capital raise volume vs July and September. This year, there isn't likely to be much confidence of any sort until we are further along our COVID recovery plan.

October through to December is always a busy period. Perhaps more-so this year as it is then (assuming there's no more spikes) when it is expected that restrictions will be properly relaxed. This is when we could see the aforementioned flurry of small/mid cap deals.

3. More volatility means investors should aim for quality companies

Volatility will continue. At the moment there's a lot of reasons for volatility, and there's a lot more traders in the market. We saw this manifest into some extreme examples last week with >1,000% daily spikes for Alterity Therapeutics and Etherstack - these were more the result of traders more than fundamentals.

There will be plenty of short term opportunities, but they will stay short term. Now is a good time to find fundamentally sound companies with a strong balance sheet, good business model and reliable cashflows. These will be the companies that are raising over the next few months for growth not survival. Our recommendation - find a few favourites, preferably in COVID resistant industries that will be looking to grow, and prepare to ride the wave.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Ben is the co-founder and co-CEO of InvestorHub, a leading SaaS business that helps public companies build direct investor relationships at scale, driving better on-market and off-market outcomes.

Our platform is one powerful solution, centralising investor engagement, communications, and analytics—backed by Direct to Investor (D2I) marketing experts.

Trusted by 160+ companies globally, InvestorHub supports businesses on the LSE, AIM, AQSE, and ASX.

........

This does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or

any other product or service by Fresh Equities Pty Ltd, its representatives or any other third party regardless of

whether such security, product or service is referenced.

4 topics

16 stocks mentioned

Ben is the co-founder and co-CEO of InvestorHub, a leading SaaS business that helps public companies build direct investor relationships at scale, driving better on-market and off-market outcomes. Our platform is one powerful solution,...

Expertise

Ben is the co-founder and co-CEO of InvestorHub, a leading SaaS business that helps public companies build direct investor relationships at scale, driving better on-market and off-market outcomes. Our platform is one powerful solution,...

Expertise

Comments

Comments

Sign In or Join Free to comment