3 reasons to love unlisted assets

Private equity appeals to perhaps more investors than ever, given historically low interest rates, flattening of fixed income yields and COVID’s crushing of stock market returns.

The alternative asset class’s almost unfettered access to businesses without the constraints of public ownership has opened up huge opportunities even amid the pandemic, says Jonathan Armitage, CIO of MLC Asset Management.

The MLC Private Equity Co-Investment Fund III, a wholesale vehicle, has been accepting subscriptions since November 2019 and is set to close in October. Armitage and his team are looking to generate an internal rate of return (pre tax and post fees and expenses) of around 15%^.

MLC Private Equity Co-Investment Fund II is coming to the end of its investment phase, having generated a net IRR of 8.6% since inception in May 2017. This return includes recent investments, which are conservatively held at cost for the first 12 months.

The first iteration of the fund, MLC Private Equity Co-Investment Fund I, which has generated an IRR of 20.4% a year since it launched more than six years ago*, is now fully subscribed and closed.

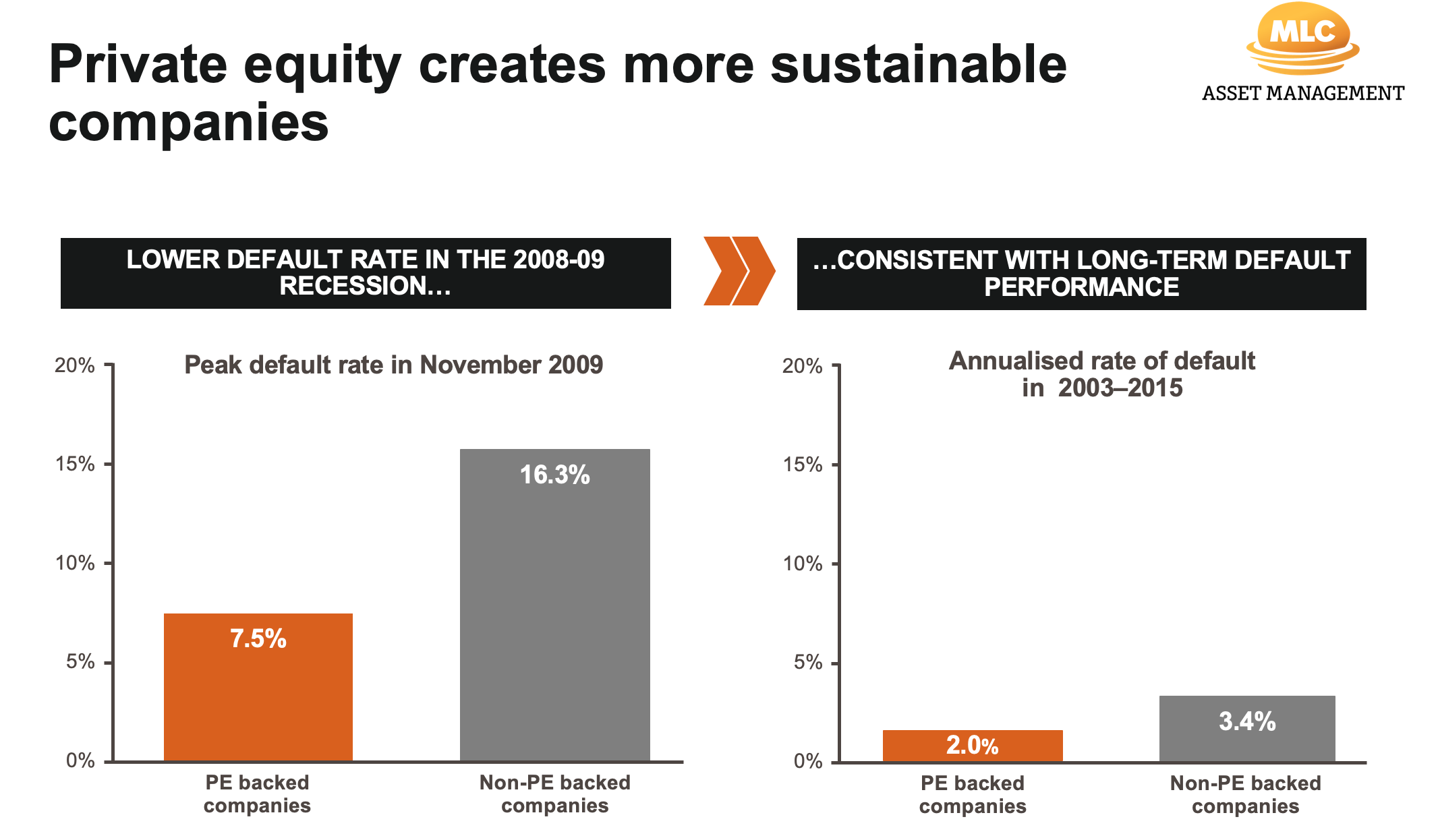

“One of the reasons why we think that private equity plays such an important role in people's portfolios is because the businesses tend to react very quickly both to changes in economic circumstances and market conditions,” says Armitage.

“We saw that back in the GFC in 2008 and 2009, and we've seen exactly the same thing occur in the last several months.”

And Armitage believes many of the companies its funds hold - businesses spanning a massive range of geographies and industries - will bounce back hard when the post-COVID recovery arrives.

In this wire, he explains how the asset class works, including both the risks and potential rewards, and the evolution of its funds over the last two decades.

.jpg)

Can you give me a bit of an introduction to MLC's private equity capabilities, some of the expertise that you've developed, track record of the funds that you run and some of the things that MLC does differently?

The private equity program has existed for 23 years and was among the first of its kind in Australia. And it is truly global, so around 95% of the assets are outside Australia.

Taking full advantage of the benefits of diversification was our key reason for designing this, breaking the private equity universe down by geography, industry and sector. And that's very much been a hallmark of the program since its inception.

Like anything over a 20-year period, the program continues to evolve. We've added some different components, moving from funds to investments with general partners, and along to co-investments as well. We've also expanded the range of areas of private equity that we look to invest in - from buyout funds to venture funds - and also expanded the geographies we look at.

What types of capabilities and geographies are currently open for investment in the private equity funds we’re talking about today?

Seven or eight years ago, we decided to enter into co-investments, when historically all our investments were in a fund structure. A co-investment is when you invest in a specific transaction alongside a private equity fund. This gives very clear alignment between what both parties are trying to achieve.

After a few years, we felt other investors would welcome such opportunities. So, we started our first co-investment fund, and we're now looking at raising money for the third of these.

What is a buyout fund, in terms of how they operate and generate returns?

Private equity covers a number of different types of transactions. But essentially what you're doing is providing capital to businesses so that they can grow, develop and evolve, either within their home markets or into new geographies. And this takes place in a private market arena rather than public markets, where you see stocks and bonds traded.

We tend to focus on those transactions where we believe a company has either a particular set of expertise or a specific technology that will allow them to continue to grow and expand its profitability.

We generally target a holding period of between three to five years, which we believe provides a good timeframe for an organisation to grow and for markets to further evolve and develop. This length of time also enables a management team to be very clear around what it's trying to achieve over the medium- to long-term.

Then at some point we would, alongside our GP partners, look to exit that business. This could involve selling to another company in the same industry; or it may involve an initial public offering to the market. At other times, we may sell a business to a different private equity fund that perhaps has an interest is consolidating some businesses in the same sector.

What are the characteristics and the types of investments you might be attracted to, and why is now a good time to assess these opportunities?

The wide range of geographies, industries and end markets of private equity is one of the major attractions for us. We invest in a very wide range of businesses, from manufacturing to consumer goods and technology.

Some recent examples of businesses in which we’ve invested include:

- a successful garden centre business based in Europe, which was looking to expand

- several technology companies in areas like financial technology

-

a leading UK-based independent video games company that is rapidly expanding its services to the global games publishing, film and TV markets.

We've also looked at consumer goods, including a UK-based food manufacturing business specialising in Indian foods. Those people who have spent some time in the UK will know that's a big part of the culinary diet there, but also a really interesting opportunity. It offers the opportunity to bring together a couple of family businesses to create much more consolidated operations, alongside the growth on offer.

Such a range of different businesses aren’t always found within public share markets, which is why it’s attractive.

The growth at each of these businesses seems to have a catalyst. What are some of the other selection criteria you apply to new investments?

Backing businesses where we think there are very good growth opportunities is really important to us. Our positive outlook may be because we think the end markets are particularly attractive, or in some cases it may be because the businesses operate in a very fragmented industry. The ability to bring together two or three different businesses to really strengthen an operation is also something that acts as a real catalyst.

Strong management is a key element in these businesses, alongside the growth opportunities, which we as private equity investors back very significantly. Management teams are a very important part of our analysis and due diligence.

Our focus on good growth opportunities means we mostly avoid things that are cyclical or where there are parts of the business that are difficult for management to control. The ability for management teams to have a very clear view about their business destiny is a key for us, so that we as investors can participate in the growth, improvement and profitability.

How has MLC’s private equity programme evolved over the last 20 years, in terms of skill set development and capabilities that have grown over time? And what are some of your unique advantages?

We have developed some extremely strong, long-standing relationships with the top investment firms in the private equity arena. This grants us quite unique access to transactions that newcomers to this part of the market won’t have.

We've also been very concentrated on certain areas of private equity, and only back the top firms or only invest with the top firms rather than across a wider spectrum.

An example of that is venture capital, where you are backing companies very early in their evolution, often right from the start. Facebook is a prominent example. We were among the first backers of Facebook when it was still a pretty embryonic business, but you can only get those opportunities if you've got very strong relationships, and those have developed over a long period of time. That’s one of the great strengths of this program.

How has the big macro shock of the COVID pandemic affected private equity investing?

Like all businesses across the economy, we've seen some mixed outcomes. But in general, we've actually seen our businesses continue to perform very well indeed.

Source:

S&P LCD as of August 2015. Includes default rates for leveraged loans for

all companies in the S&P LCD Index.

"One of the reasons we think that private equity plays such an important role in people's portfolios is because the businesses tend to react very quickly both to changes in economic circumstances and market conditions. We saw that back in the GFC in 2008 and 2009, and we've seen exactly the same thing occur in the last several months"

As the impact of the pandemic has flowed through to different parts of the economy, we’ve seen businesses look to adapt to their operations. Some parts of businesses have been significantly reduced, while others have seen a significant uplift in the type of business that they do, their operations and their end markets.

In the example of the garden centre business mentioned earlier, obviously as shutdowns were put in place by various governments, that business faced some pretty significant short-term challenges. But since markets have started to reopen, it has rebounded incredibly strongly. And it's actually operating at about 30% ahead of where it was 12 months ago. Part of that has probably been pent up demand and the fact it's been a very good summer in the northern hemisphere. But it's also down to the management team taking the time when they were locked down to really reassess the type of business that this could be once the garden centres opened up again. And that's very much driven, not only strong revenues, but they've adjusted the cost base. So now, the profitability of the business is significantly ahead of where it was 12 or 18 months ago.

What are the pros and cons of being able to invest in private markets versus public markets?

The lower liquidity of private equity is one of the main differences. When you're committing capital to these businesses, you are committing it for the medium- to long-term. These are not businesses that are traded on a daily basis, and you need to ride out some challenging economic times.

But the diversification across different industries and markets is one of the real advantages that you don't get with public markets. There are many examples where our funds have gained access to some really good growth prospects, including parts of the technology sector. Not many public market businesses can give you that real targeted exposure to such growth opportunities.

What's the average size of the investments in your funds? And what type of returns have been generated by those that are already up and running?

Two funds are up and running, and our first fund has been fully invested. We're targeting a return of around 15% net IRR (pre tax and post fees and expenses^). If we look at the average of the investments that have been made across the business, we've delivered strong returns to our clients.

As we've grown out the program, these funds have invested alongside MLC. The average amount of money per investment is usually somewhere between $30 million and $50 million. And we tend to target around 20 investments per fund, but this depends on the opportunities that arise at a specific time.

Are the returns from private equity funds all capital gain, or are there distributions along the way?

It can be a mixture of capital return and capital gains. That will vary from investment to investment, in how those businesses travel in terms of our time of ownership, and also depends on our exit strategy.

If we look at our first fund, we are very much in what I call harvest mode. So all the investments have been made and we're now seeing those returns coming back to the investors in those funds. And it's been a mixture of capital return and also capital gains as those businesses have been sold.

In our second fund, we’re pretty much to the end of the investment part. But already we’ve had one business that has been sold into the creation of a larger technology platform and another that has just listed on the US stock market. So, even though that second fund only launched less than three years ago, we’ve already seen some very attractive results.

Invest with a leading Private Equity Manager

The MLC Private Equity team has successfully launched two co-investment funds that have generated strong returns for investors. MLC Private Equity has created an opportunity with a newly created closed-ended fund and a larger fund size to better match the level of potential co-investment opportunities.

Co-Investment Fund III First Close is planned for October 2020 with documents recommended to be submitted by no later than 30 September 2020.

This opportunity is for Wholesale Investors only, please click here for more information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

This is an archived profile. Glenn Freeman was a content editor at Livewire Markets from August 2020 to July 2024.

........

^The investment return objective is 15% net IRR p.a. (pre tax and post Management Fees, Performance Fee and expenses) over the life of the Fund. This is a target and may not be achieved.

*MLC Private Equity Co-Investment Fund I has generated an internal rate of return (IRR) of 20.4% per annum since inception (15 November 2013) to 30 June 2020, and MLC Private Equity Co-Investment Fund II, which is still in investment phase, has generated an IRR of 8.6% since inception (16 May 2017). All returns are calculated IRRs based on latest available valuations from MLC’s managers, as at 30 June 2020. Return is pre-tax and post Management Fees, Performance Fees and expenses to investors based on their capital contributions. Past performance is not an indicator of any future performance of the MLC Private Equity Co-Investment Funds I, II and III. Past performance is not an indicator of any future performance of the MLC Private Equity Co-Investment Funds I, II and III.

4 topics

This is an archived profile. Glenn Freeman was a content editor at Livewire Markets from August 2020 to July 2024.

Expertise

This is an archived profile. Glenn Freeman was a content editor at Livewire Markets from August 2020 to July 2024.

Expertise

Comments

Comments

Sign In or Join Free to comment