The Risk-Return Matrix: Where does it say to invest?

A run of decent economic numbers for the US and the eurozone and the fiscal stimulus promised by US President Donald Trump are reinforcing views that core inflation will accelerate in the coming 12 months.

For asset allocators, this raises two key issues. First, how high, how fast and how pervasive will the rise in inflation be? Our central case is that the gradual tightening in the labour market (particularly in the US) and the wider effects of higher oil prices will boost core US inflation. While US protectionist trade policies and Trump’s fiscal stimulus could result in a higher result, we only expect US core inflation to rise modestly, from 2.2% in the 12 months to December to between 2.5% and 3%.

The other issue is what this rise in inflation means for asset prices. All else being equal, higher inflation should lead to higher interest rates, which should have a negative effect on asset prices. Higher rates would reduce the appeal of assets that have been priced off low bond yields. The most vulnerable assets are the bond proxies, especially A-REITs. The degree to which higher inflation is being driven by stronger demand will help earnings. This, to some extent, will mitigate the implications for valuations from a steeper discount rate. That said, as the risk premium on equity markets (especially the US equity market) is extremely narrow, we are leaning towards the deterioration in valuations outweighing any boost to earnings from stronger growth.

In shorter-term context, the post-US-election rally in risk assets and the corresponding sell-off in bonds have done several things. First, these market movements have reduced prospective returns from equities and credit and lifted prospective returns from bonds. While it’s premature to get too excited about the latter as yields might go higher still, the gap is narrowing. Consistent with this, notwithstanding the record levels of policy uncertainty, market volatility remains low. It’s difficult to see how this can persist and we think that being too relaxed seems imprudent at this point.

Portfolio construction for the Real Return Strategy reflects this thinking. During January, we reduced our equity exposure in favour of cash. Month-end overall equity exposure was about 26% with the US our least-preferred market. We’ve kept portfolio duration low, given our view that the rise in bond yields is not yet over.

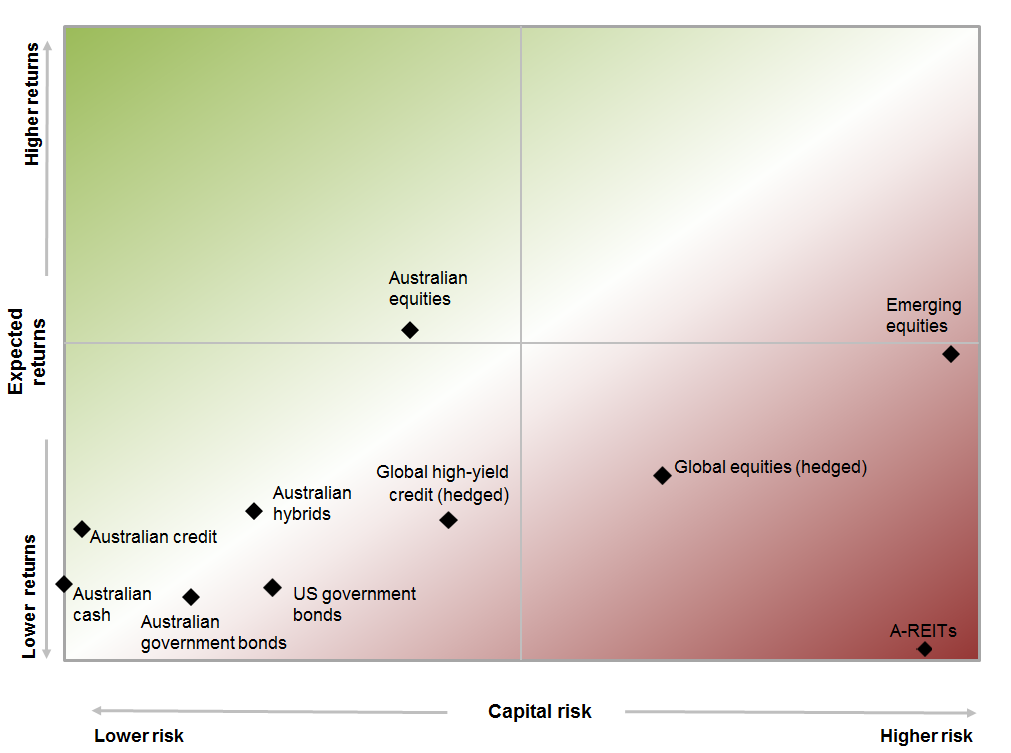

The Risk-Return Matrix

As at 31 January 2017.

The Risk-Return Matrix shows the attractiveness of key Australian and global asset classes. Likely returns over the next three years are judged on an absolute-return perspective. Risk is based on the likelihood of capital loss over the next three years.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Simon is responsible for Schroders' Australian Fixed Income and Multi-Asset capabilities. He has direct portfolio management responsibility for the Schroder Real Return Strategy, Schroder Balanced Strategy and Schroder Fixed Income Core-Plus Strategy

1 contributor mentioned

Simon is responsible for Schroders' Australian Fixed Income and Multi-Asset capabilities. He has direct portfolio management responsibility for the Schroder Real Return Strategy, Schroder Balanced Strategy and Schroder Fixed Income Core-Plus Strategy

Simon is responsible for Schroders' Australian Fixed Income and Multi-Asset capabilities. He has direct portfolio management responsibility for the Schroder Real Return Strategy, Schroder Balanced Strategy and Schroder Fixed Income Core-Plus Strategy

Comments

Comments

Sign In or Join Free to comment