40% housing correction highly unlikely

Paul Wylie

Mason Stevens

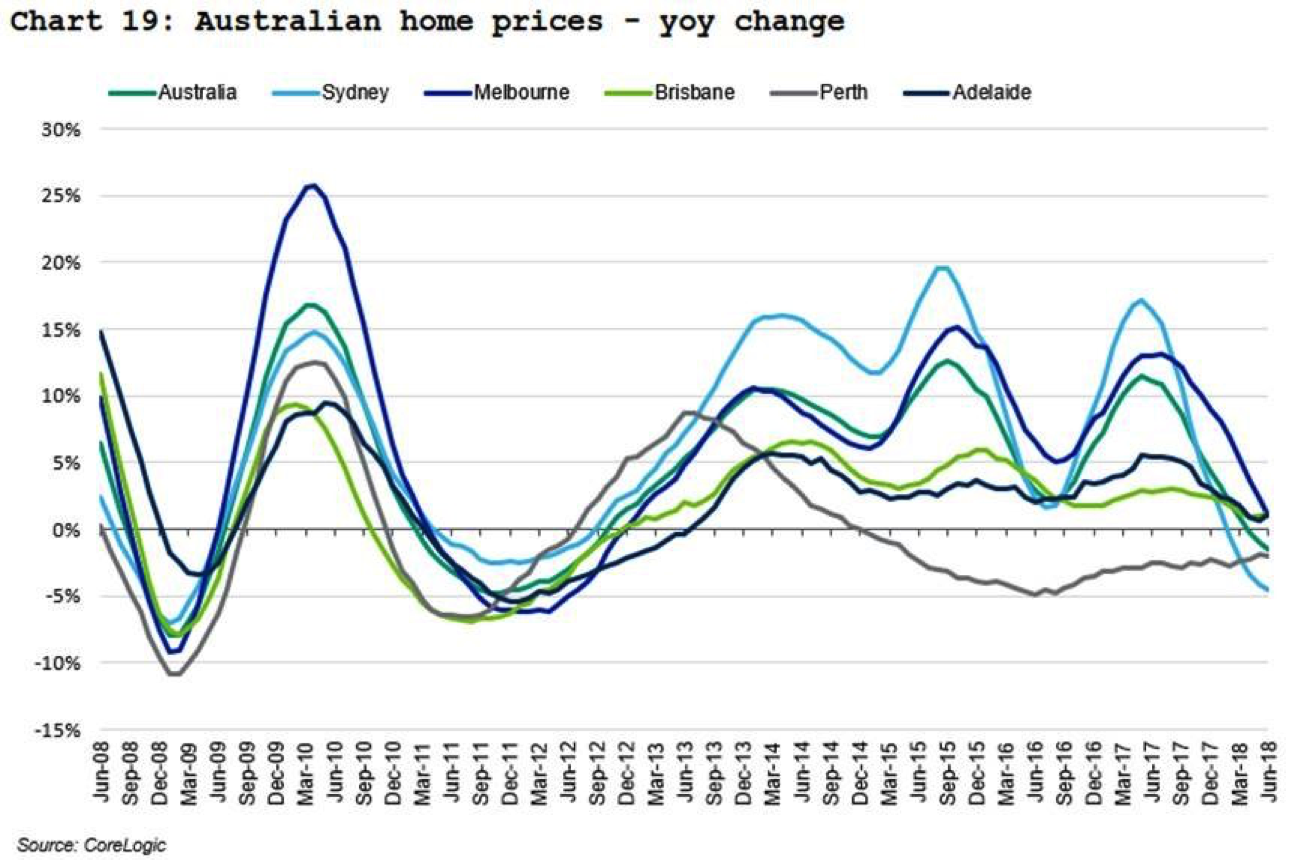

House prices are now falling in Sydney, Melbourne, and Perth according to CoreLogic's recently released data. Year-on-year changes in house prices are shown in the chart below. Some media outlets are quoting "experts" who say the housing market is going to fall 40%. I'm going to go out on a limb here and say that that will not be the case, for five main reasons.

Firstly, the current historically low RBA cash rate means that rental yields and mortgage rates are relatively close to each other. That means that, if necessary, people can service their mortgage by renting out their property and moving in with someone else. For forced selling to occur, either rental yields would need to fall, or mortgage rates would have to increase substantially.

Secondly, Australian immigration growth over the last 10 years has averaged 1.69% p.a., and is expected to continue at that rate for the foreseeable future. Those immigrants need to live somewhere, and that demand will help soak up excess supply.

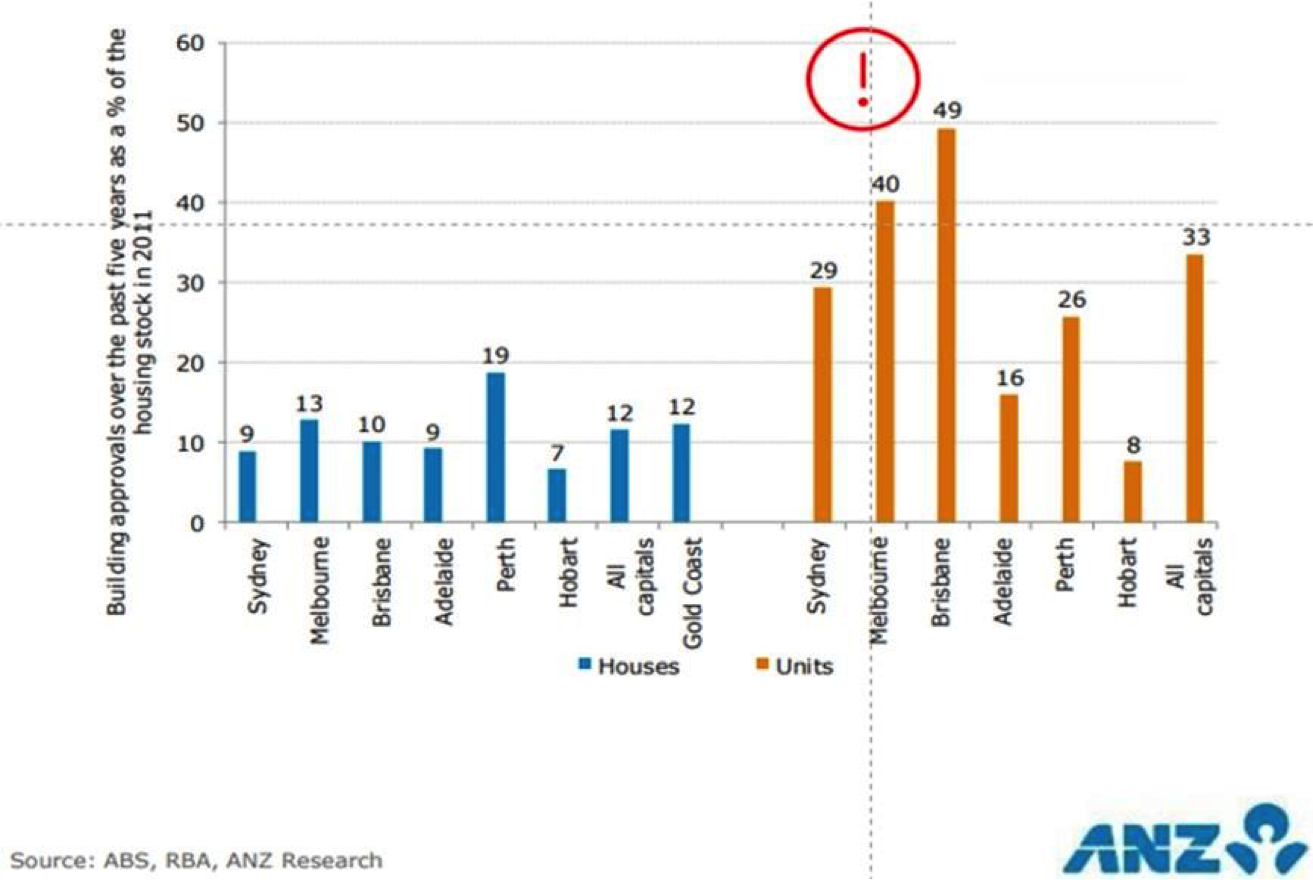

Thirdly, out of the residential building approvals of recent years (see chart below), a portion has already been cancelled/deferred. The changed market conditions and tighter lending conditions mean that some of that supply will no longer come to the market.

Fourthly, Australians dislike selling their homes at a loss even if they are buying/selling in the same market. This typically results in house prices flatlining for extended periods rather than experiencing short, sharp falls.

Lastly, Australians will default on anything else before they default on their home. This means you will see dips in discretionary spending, and increasing credit card and car loan defaults, before any meaningful mortgage defaults.

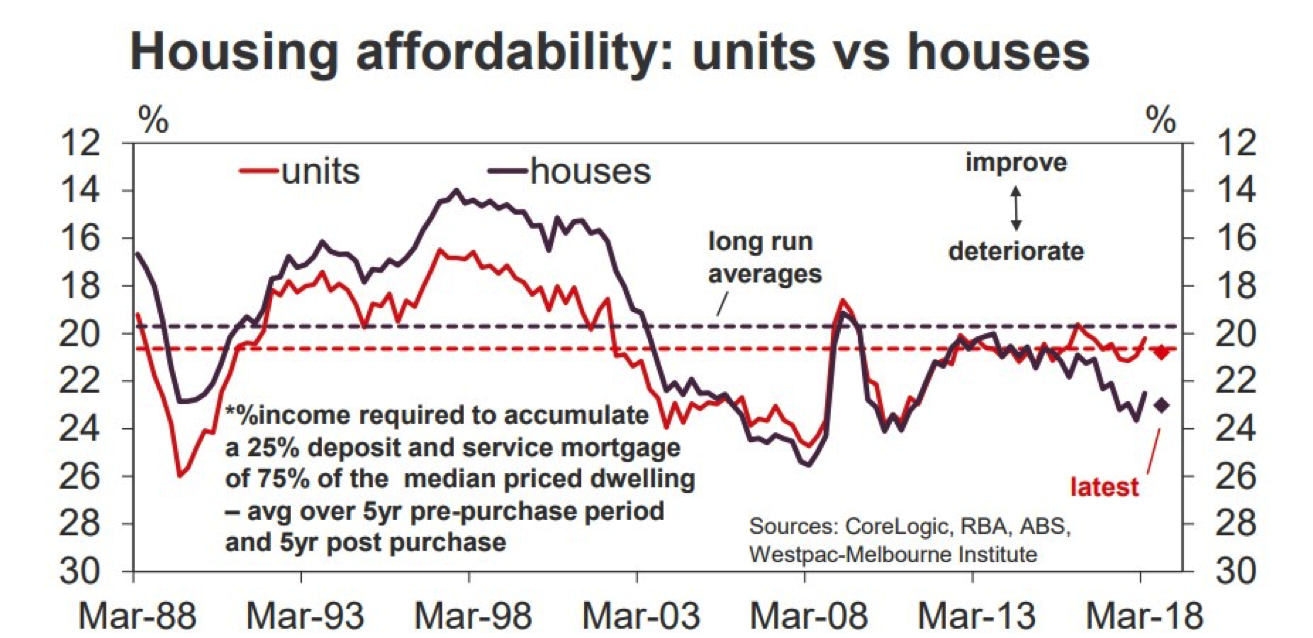

The above is not to say that the Australian housing market doesn't have issues. It does. For example, Australian housing is currently very unaffordable. Mortgage principal and interest costs, according to Moody's, has been averaging 35% to 40% of income for a two-income household in Sydney for the last 3 years. This is above historical averages and only surpassed by the peaks of 1989 and 2007 (see chart below).

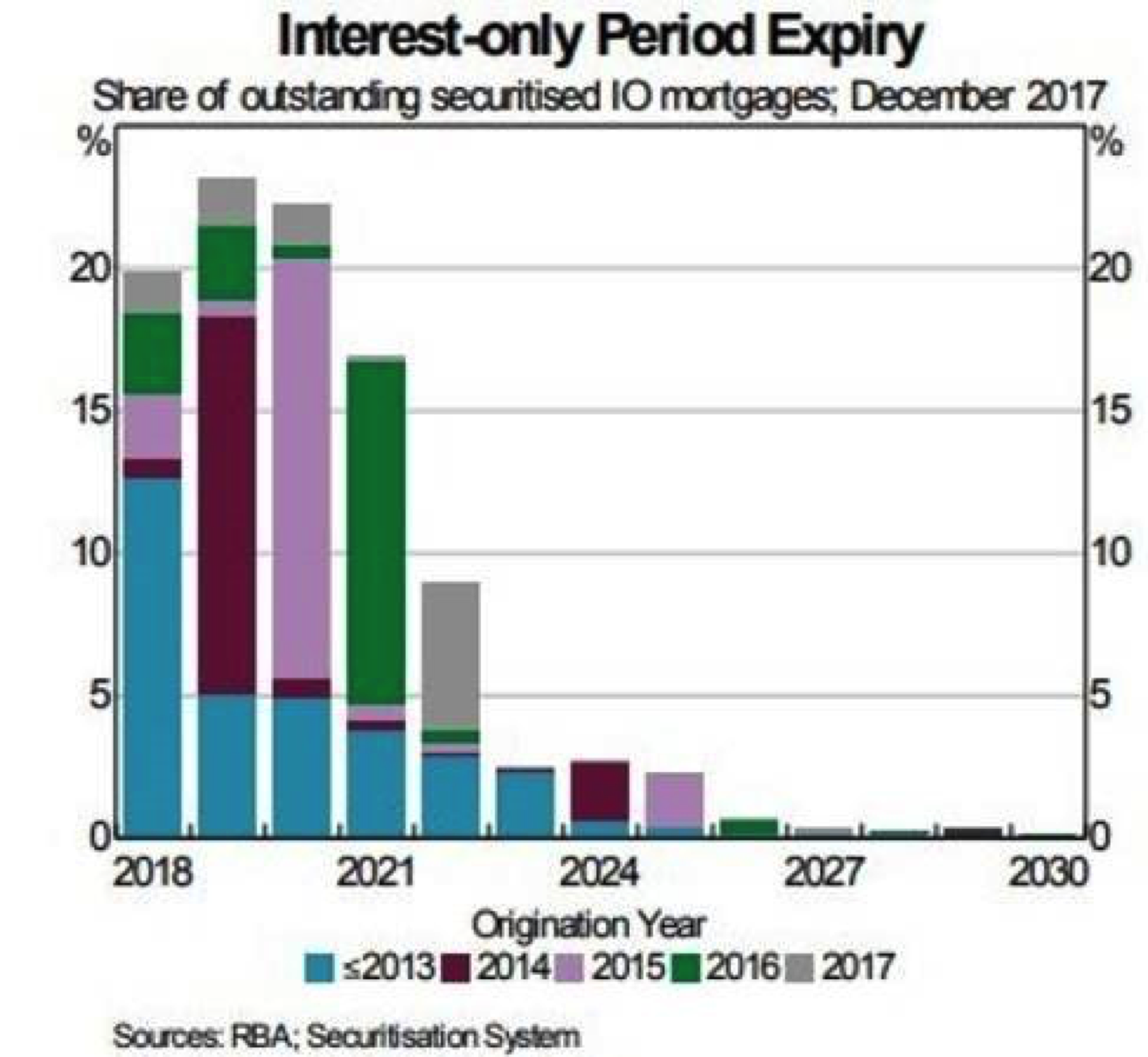

The crackdown on interest-only mortgages is also going to be an issue for the market, as investors are forced to transition to principal and interest repayments. The transition is expected to peak in 2019/2020 and may cause some additional selling at the margin or, at best, less demand for new investment properties as free cash flow is eaten up by increased mortgage payments.

Summary

It's hard to overestimate how much of a political football housing is in Australia. The Australian federal government, along with their State counterparts, has a long history of enacting policies that support house prices (e.g. first-home-buyer grants).

In the UK, when house prices fell 25% in 2009 the government panicked and enacted policies to stabilise prices and reverse the trend, as it was politically popular to do so. For example, they offered to co-invest with first-time home buyers, who could then buy out the government's equity in their home later.

In the event of a major housing crash here, I would be surprised if the Australian government didn't try to do the same thing here.

To get meaningful price falls in Australia, you need meaningful forced selling. It would require unemployment to increase substantially. With the employment market still relatively tight, it is hard to see anything near a 40% housing correction from here.

--

This article is prepared by Mason Stevens Limited (Mason Stevens) ABN 91 141 447 207 AFSL 351578 and is general advice only and does not take into consideration yours or your client’s personal objectives, financial circumstances or needs and should not be relied upon as personal advice. You should consider this information, along with all of your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Securities, by nature, rise and fall and as a result investing in securities including derivatives involves risk. Past performance is not a reliable indicator of future performance and may not be achieved in the future. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.

Mason Stevens ensures that the information provided is accurate and complete but does not warrant its accuracy or reliability. Opinions and or information may change without notice and Mason Stevens is not obliged to update you if the information changes. Mason Stevens and its associated companies, authorised representatives, agents and employees exclude to the full extent by law, liability of whatever kind, including negligence, contract, fiduciary duties or otherwise, to investors or anyone else in respect of any loss or damage, including indirect or consequential loss or damage, foreseeable or not, arising from or in connection with this information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Paul is an experienced global credit portfolio manager, having recently held the positions of Global Head of Credit Solutions and Strategic Trading for Lloyds Banking Group.

1 topic

Paul Wylie

Fixed income Investment Strategist

Mason Stevens

Paul is an experienced global credit portfolio manager, having recently held the positions of Global Head of Credit Solutions and Strategic Trading for Lloyds Banking Group.

Paul Wylie

Fixed income Investment Strategist

Mason Stevens

Paul is an experienced global credit portfolio manager, having recently held the positions of Global Head of Credit Solutions and Strategic Trading for Lloyds Banking Group.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets