5 charts that will determine the next 12 months

In attempting to forecast the short term outlook for Australian equities in 2019, I do so with some trepidation. I have always suggested, and I think it has now become a broadly accepted principle, that it is far easier to forecast the performance of asset markets over a longer period (3 to 5 years) than it is over the short term (1 year).

The short term is subject to daily noise, with the perceptions and reactions of traders and speculators a constant. Today, these market players dominate short term price movements, so their activity and trading correspond to the immediate feel of tail or headwinds.

Traders by their nature survive on volatility and they exacerbate market price movements by front running, shorting and utilising leverage. With the addition of computer trading, retail day traders and stock lending facilitation, the equity market of today presents as a place where the full ambit of human emotion, positive or negative, greed or fear, is highlighted by rapid price movements.

However, from a longer-term investment perspective, there may develop opportunity. It is clear that the many issues confronting markets have developed out of complacency - excessive monetary policy support through low interest rate settings and excessive quantitative easing.

Importantly, in 6 months’ time, what today presents as difficult issues will have been addressed, resolved and passed. What today is speculation will have been replaced by facts.

Think of the US - China trade war, Brexit, the US budget and a necessary response from Congress, the US monetary policy adjustments, the Trump Russia enquiry, the forthcoming Australian election and anticipated taxation changes. Most of these matters will be dealt with in the first half of 2019 and we will then be able to deal with actual events rather than speculation.

Thinking of the present uncertainty, I am drawn to quote from one of the great thinkers from history. Abraham Lincoln once said:

"The dogmas of the quiet past are inadequate to the stormy present. The occasion is piled high with difficulty, and we must rise with the occasion. As our case is new, so we must think anew and act anew."

What would the world give for a leader like Lincoln? How much easier would it be to invest with a steady hand at the helm? But we don't have Lincoln, we have Trump … and volatility is the short-term result.

Having made those points, with its implicit disclaimer, I now enter the world of speculation. In doing so, I present five charts that are influencing my thinking.

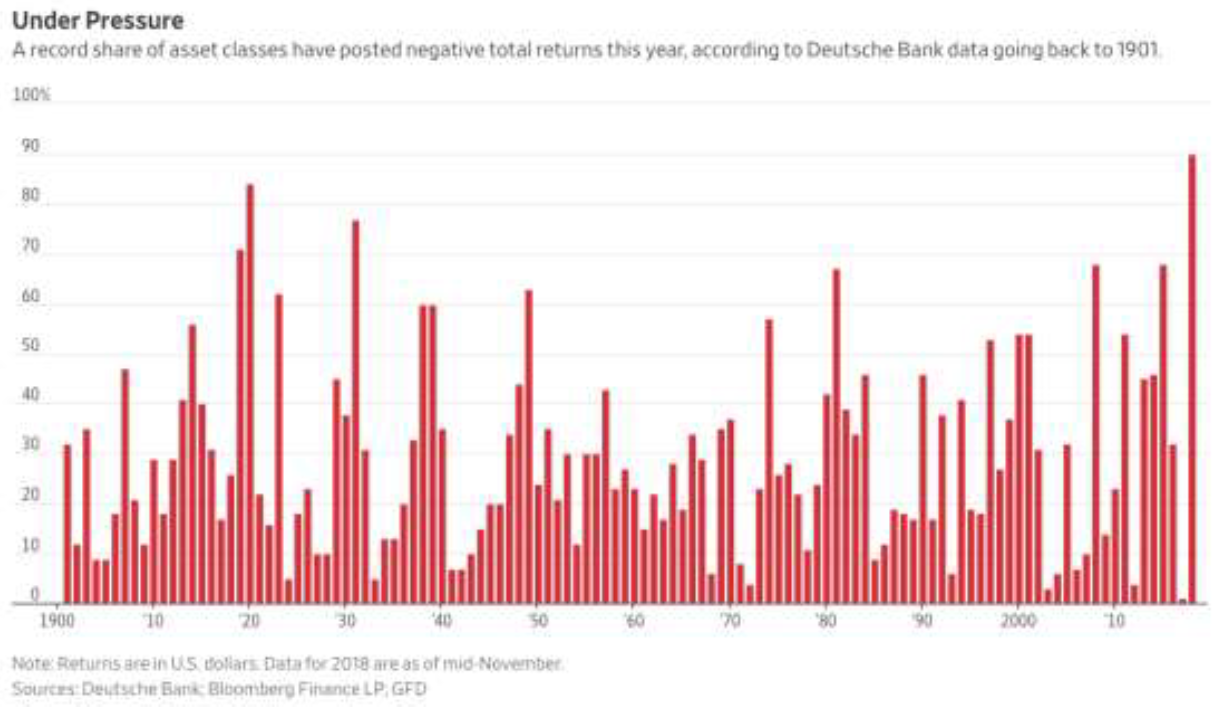

Chart 1 – 2018 has been a particularly bad year for most investment assets

My first chart tracks the returns on US dollar investment assets for the last 118 years. From this we can see that 2018 has been an extraordinarily poor year – indeed the worst on record!

The multi asset USD returns (across equities, bonds, debt and property, etc.) that capture returns across the world, show that over 90% of asset classes have recorded negative returns. However, 2017 showed the complete opposite with virtually every USD-based asset class rising.

Why is this important to note? Simply because markets move faster than human perceptions of change, and the chart shows that markets have moved in anticipation of bad economic outcomes.

From an Australian equity perspective, I note (at time of writing) that the Australian equity price index has declined by over 6% this calendar year. To some extent bad news is already priced into markets. Further, the price index is lower than it was 3 years ago, suggesting that there is generally not much “bullishness” in Australian equity prices. That suggests some support for equities in 2019.

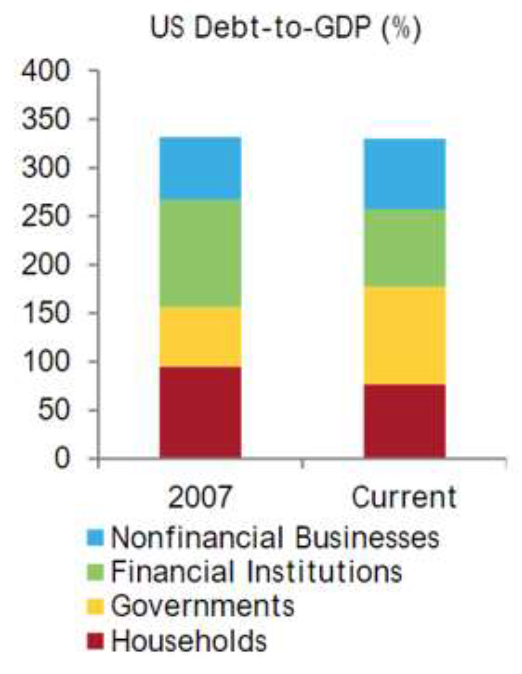

Chart 2 – US Government Debt is a growing problem. Is QE4 coming?

My next chart focuses on the burgeoning US government debt that is now accelerating under President Trump. The chart compares the makeup of total US debt from 2007 to 2018.

My thoughts on this analysis are as follows. While total US debt as a percentage of US GDP has not increased (and that’s good), it is very concerning that the level of US Government debt has ballooned from about 50% of GDP to about 100% of GDP.

These are levels of Government debt that could see bond yields rise dramatically, as the creation of debt (bonds) exceeds the capacity of markets to consume it. Indeed, such debt levels have seen dramatic credit rating downgrades across southern Europe as it is perceived that the budgets of these countries will be progressively ruined by ongoing interest payment requirements.

The offset is of course the creation of fabricated demand by the utilisation of quantitative easing (QE) – the printing of money! This in turn holds down interest rates, maintains the solvency of governments and stimulates risk assets.

Could there be a return to QE in the US in 2019, and what would that mean for riskier assets (like equities) across the world? Whilst that is speculation, you can hopefully see the thread of my thoughts.

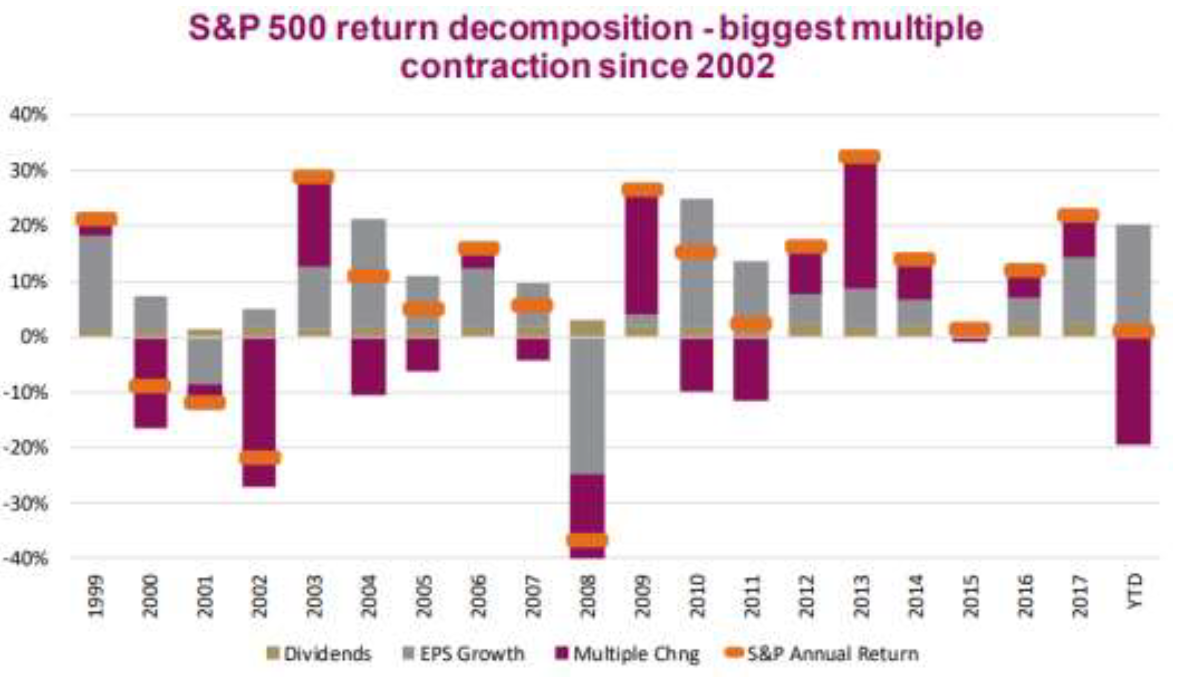

Chart 3 – PER contraction in 2018 means what for 2019?

Again, I am focusing on the US, as its equity market drives the sentiment for the Australian equity market. The following chart shows the interesting interplay between earnings growth (eps), PER movements and dividends, that determine the total yearly returns from US equity markets. A similar analysis could also apply to other equity markets across the world.

At the date of this report, the return on the S&P500 index for 2018 is flat (but trending negative). The growth in earnings (circa 20%) has been totally offset by PER contraction. This is the opposite of the 2017 outcome, when earnings growth was enhanced by PER expansion.

In forecasting equity performance in 2019, we have to have a view on earnings growth and PER movements. Further we have to determine by how much the market has already adjusted to perceived outcomes. Finally, the PER will be directly affected by bond yields. A higher bond yield should push PERs lower while lower bond yields will push PERs higher.

Thus we come to the problem of today’s forecasting. Are US bond yields (and Australian bond yields) about to fall or rise? The supply of bonds (the burgeoning US debt) suggests US bond yields will rise and US PERs are going to fall. A recession in the US, leading to lower bond yields or an introduction of QE4, could suggest PERs will rise as earnings come under pressure. In the later scenario, PER expansion offsets earnings decline for a ho-hum outcome for equities.

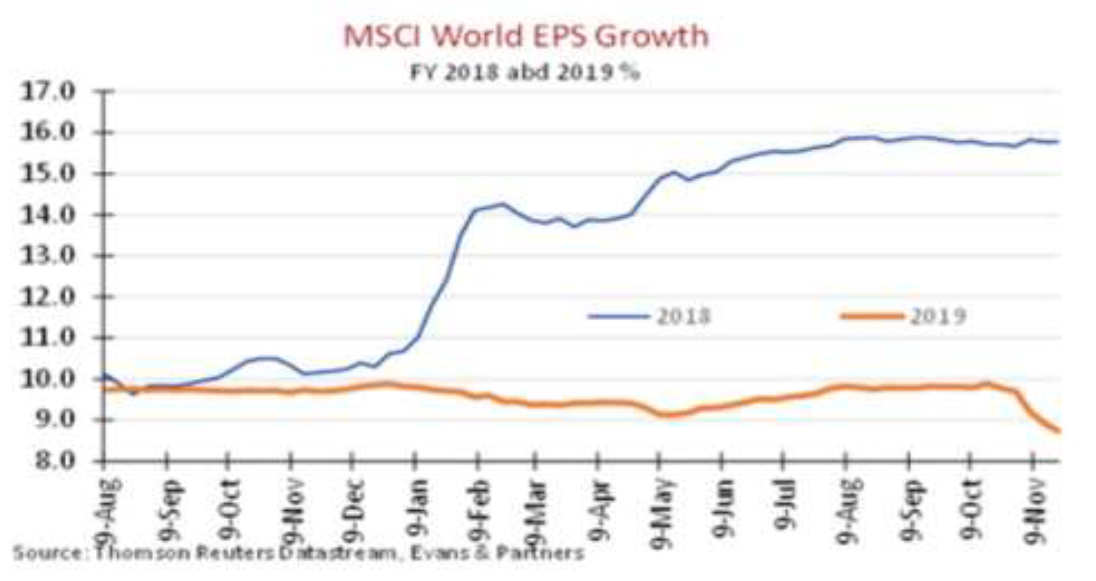

Chart 4 – World equity earnings are currently forecast to rise in 2019

My next chart highlights the current earnings achieved for 2018 and the current forecasts for 2019. It is observable how earnings have lifted substantially in 2018 and are forecast to have a moderate rise in 2019 (at this point).

We note that the dramatic lift in earnings for 2018 has been strongly affected by the Trump tax cuts. The US equity market accounts for over 60% of the world index and so world earnings growth is substantially attributed to US earnings growth – particularly their massive multinationals.

Looking forward to 2019, we see that market analysts are trimming forecast earnings growth.

The interplay of earnings growth and PERs is that earnings growth of about 8% does not support PERs of 17 to 18 times unless bond yields are heading lower.

But given that bond yields are already historically low and bond debt is growing faster than GDP (particularly in the US), I suspect that PER compression will continue in 2019. That is not a bullish scenario for equities in Australia.

Chart 5 – Australian earnings growth

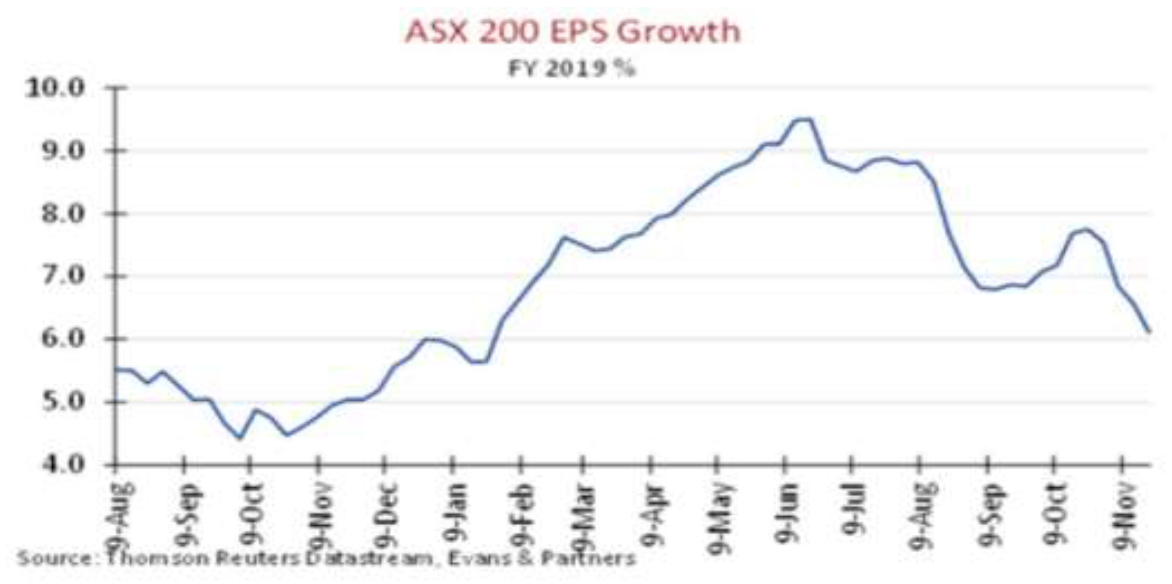

My final chart focuses on Australian earnings growth projections, currently being subjected to sober readjustments by equity analysts.

We are now about halfway through financial year 2019 and we can see that market earnings growth is moderating towards 6%; I personally have little confidence that even this growth can be achieved. Thus, it seems to me that the correction in our equity market, driven by US PER contraction in the December quarter of 2018, has correctly adjusted to a flat earnings outlook for the Australian market. However, the market will soon (from about February) become focused on the outlook for FY2020. On this interplay, I suggest that investors maintain a patient attitude to equity investment and accumulation. The outlook for FY20 will become clearer as the plethora of macro and political issues are dealt with.

Also, I note that over the last five years, Australian market analysts have been excessively bullish on earnings growth in Australia and have therefore contributed to the volatile ride for Australian equity prices.

Therefore my conclusion and speculative forecast for 2019 is this: flat Australian earnings will be compounded by declining PERs … and the macro environment will be driven by higher bond yields caused by ill-conceived fiscal policies in the US.

There will be plenty of opportunities in the next year to buy quality Australian equities at cheap entry points as prices oscillate given all the uncertainties. In the meantime, the Australian listed market is full of income opportunities and these are fairly unique in a world where most sovereign long-term bond yields sit well below 2% yield.

The short-term outlook is seldom clear and is at present packed full of uncertainty. Buyers of Australian equities in 2019 will need to be patient and focused on the undeniable growth that seems assured for Australia over the next 5 to 10 years.

As for speculators, I wish you luck - because you will need plenty of it to navigate 2019.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

John has 35 years experience in funds management and corporate advisory services. Prior to establishing Clime, John’s roles included ten years at NRMA Investments as the head of equities.

Clime is a management and advisory business for mainly SMSFs.

John has 35 years experience in funds management and corporate advisory services. Prior to establishing Clime, John’s roles included ten years at NRMA Investments as the head of equities. Clime is a management and advisory business for mainly SMSFs.

John has 35 years experience in funds management and corporate advisory services. Prior to establishing Clime, John’s roles included ten years at NRMA Investments as the head of equities. Clime is a management and advisory business for mainly SMSFs.

Comments

Comments

Sign In or Join Free to comment