5 stocks to benefit as we hit the road

If the Chinese experience along with early indications locally is anything to go by, then Australia’s love of the car has just got another shot in the arm from COVID-19. As Macquarie wrote in a good note this week, who wants to share a bus or train with people who could be asymptomatic COVID-19 cases? Riding to work this morning there is a clear uptick in traffic volumes and that’s being supported by the experience from other countries as they emerge from lock downs.

Data from China has shown a clear preference for the car over and above public transport supporting traffic growth by the start of May that was actually up year of year while public transport volumes were still weak. Locally, toll road operator Transurban has confirmed that group traffic volume bottomed in the week starting April 12, and has recovered since. With our borders closed, Australian’s are also likely to take to the car for holidays – national lampoon style!

Source: National Lampoons

This has ramifications for stocks exposed to cars, whether that be sales, leasing, parts, roads or maintenance and in todays note we’ll touch on 5 Income stocks exposed to this uptick in various ways. Important to note here that income investing during this time is more about understanding the likely bounce back in earnings and thus dividends. Using historical dividend numbers is fairly meaningless, while extrapolating current payouts is also a pointless exercise. Having a broad understanding of how earnings could recover anchored to the strength or otherwise of balance sheets in MM’s view in the key to investing for future income in these challenging times.

1 AP Eagers (APE) $6.46

APE is responsible for the sale of 1 in every 10 new vehicles in Australia with 224 new car dealerships across 33 different brands. They also have a large truck dealership network with 68 dealerships across 12 brands. It’s a big operation and APE are the clear dominant player in the Australian market. While they carry around $315m in debt they have real assets in the business, including $260m worth of property. As Australian’s drive more to work, holiday domestically at a time when interest rates are record lows, there is a clear case for a rebound in new car sales.

MM is bullish APE while it holds above $5

AP Eagers (APE) Chart

2 Transurban (TCL) $14.74

TCL operate toll roads in Australia, America and Europe and have experienced a notable uptick in the use of their toll roads over the past month as more commuters go back to work, albeit from a low base . April was a horrible month for traffic with volumes down around 60% in Australia, nearer 70% in the US and closer to 80% in Europe. A preference for car travel versus public transport is a tailwind for TCL however that will be partially offset by higher unemployment and a large proportion of professional services still working from home.

In early May, TCL held an investor briefing and one aspect of note was discussion around their dividend. It seems very likely that a tweak to how TCL calculate dividends is likely.

“Transurban continues to assess the use of proceeds from Capital Releases noting that they can be used to: strengthen credit metrics; fund development/acquisition opportunities; or enhance distributions” - Transurban Investor Briefing.

The change here is that capital releases used to support a higher dividend and this change in rhetoric / laying the foundation is exactly what politicians do when their about to take something away from us. In any case, I think excluding capital releases from supporting ordinary dividends is a positive thing for the business in the longer term however the market may take an issue with it in the short term. We hold in the Income Portfolio.

MM remains bullish TCL targeting ~$17, although risk/reward improves on a pullback to $14

Transurban (TCL) Chart

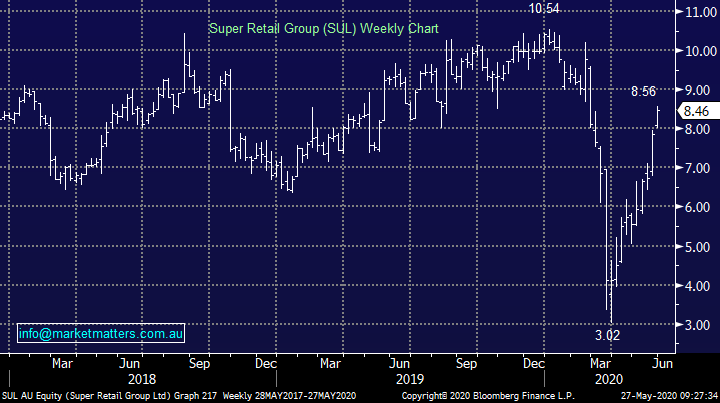

3 Super Retail Group (SUL) $8.46

The diversified retail group is a reasonably new addition to the MM Income Portfolio (along with Transurban). While SUL operates Super Cheap Auto, they also have a broader retail exposure through BCF, Macpac & Rebel Sports, areas of retail that benefit from changing trends towards domestic travel (camping) and in the case of Rebel, the growing number of home gym junkies. While the likes of JB Hi-Fi (JBH) benefitted from the initial spike in electronic purchases that underpin remote working / learning, SUL is set to benefit from this next wave of changing habits, a change that doesn’t seem lost on the market given the exceptional recovery from the ~$3 low in the stock to now trade 20% below its recent high.

It seems to me the market is now pricing in a lot of optimism in this stock.

MM are sitting on a ~40% profit on this position targeting ~$9

Super Retail Group (SUL) Chart

4 Atlas Arteria (ALX) $6.86

Similar to Transurban, ALX owns, operates and develops toll roads. They have 4 in their portfolio with 2 in France and 1 each in Germany and the US. Similar to TCL, they are set to benefit from increasing use of cars and their share price is starting to factor this in.

While low interest rates for an extended period of time will be a bi-product of COVID-19 which is supportive of infrastructure assets, we believe that a significant amount of the recovery is now priced into stocks like ALX.

MM are neutral ALX

Atlas Arteria (ALX) Chart

5 Smart Group (SIQ) $6.59

The salary packaging and leasing company had a strong session yesterday adding 13%. The main driver for SIQ earnings is salary packages, they simplify the process and are good at it. They also do novated leasing and fleet management + associated vehicle buying. New car sales are important for SIQ and as discussed above with APE, while current trends towards new car sales have been weak, we expect this to improve. We hold in the income portfolio.

MM remains bullish SIQ targeting a test of ~$7.80

Smart Group (SIQ) Chart

6 Banking Sector

While we covered the banking sector in the AM note today, the stocks above highlight the level of recovery that is being priced into some stocks / sectors. If such as economic recovery plays out then banks should also benefit, to date they’ve been an obvious omission. I spoke about the banks in a recording yesterday afternoon – click here

MM are bullish the banks

Banking Sector Chart

Conclusion (s)

MM remains bullish SIQ, TCL & APE in that order

MM is now neutral SUL & ALX,

MM is bullish the banks

Have a great day!

James & the Market Matters Team

Register for a free trial to Market Matters

At Market Matters, we write a straight-talking, concise, twice daily note about our experiences, the stocks we like, the stocks we don’t, the themes that you should be across and the risks as we see them.

To sign up for a free trial to Market Matters, leave your email and phone number through the 'CONTACT' button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and Partners heading up a team that manages direct domestic and international equity & fixed-income portfolios for wholesale investors.

........

Any advice provided is of a general nature only.

5 stocks mentioned

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

Comments

Comments

Sign In or Join Free to comment