5 tips to help investors refocus on retirement

Matt Reynolds

Capital Group

The current COVID-19 crisis and its consequential economic and market impact represent the first serious challenge to the new generation of investors in retirement who have embarked on drawdown. Incorrect investment decisions taken now could mean retirees leading poorer and less fulfilling lives as they move through the retirement years. However, if investors refocus on their retirement objectives and maintain a long-term approach, it should be possible to navigate the current difficulties without substantial long-term damage.

One of the most important considerations for investing in retirement is that individuals are different, each with unique financial needs, different sources and amounts of retirement income and completely personal ambitions for their future in retirement. Any list of potential actions to help refocus investors on retirement needs to bear this in mind. Nevertheless, the following ideas may be worth considering in the light of investors’ own circumstances:

5 tips to help investors “refocus on retirement”

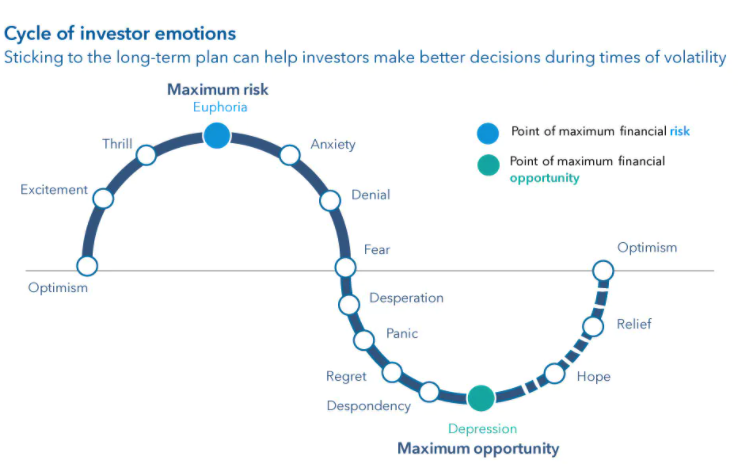

1. Keep a long-term perspective: For all investors, keep your long-term investment objectives at the forefront of your mind and align your actions with them. However, it is important to realise that any dramatic changes to your investment stance in the current environment are likely to be costly; instead, you might consider doing things gradually or waiting for more stability. Market liquidity can be poor in the current environment, which makes transactions potentially more expensive. It is also easy to become over-influenced by market sentiment, which makes decision-making with long-term consequences particularly difficult at times like this.

2. Diversify investments: Diversification is an old principle, but recent market volatility underlines its importance. However confident you feel in picking the best performing areas, it is invariably better to have a spread of investment exposure across asset classes that are suitable for your objectives. This is particularly true at times when shifting strategy can result in realisation of losses.

3. Review income generation options: Once the present COVID-19 crisis has subsided and market volatility has normalised, consider taking the opportunity to review your portfolio. Bear in mind that future income levels expected from the portfolio may have altered; for example, bond yields may have changed – in either direction depending on credit rating - whilst future dividends from equities may be reduced at least temporarily, even if historical equity yields have risen.

4. Consider changes to drawdown amounts: Investors already drawing down from their retirement pot could consider suspending or reducing withdrawals while markets are depressed. If you have other sources of income in retirement such as a defined benefit plan, you might be better placed to do this. Review your spending plans for this year; if a holiday or other large event outlays won’t be going ahead in the near term because of COVID-19, you may have more headroom to adjust your drawdown than you realised. Remember that taking money from an already depressed investment reduces the potential for recovery in your portfolio.

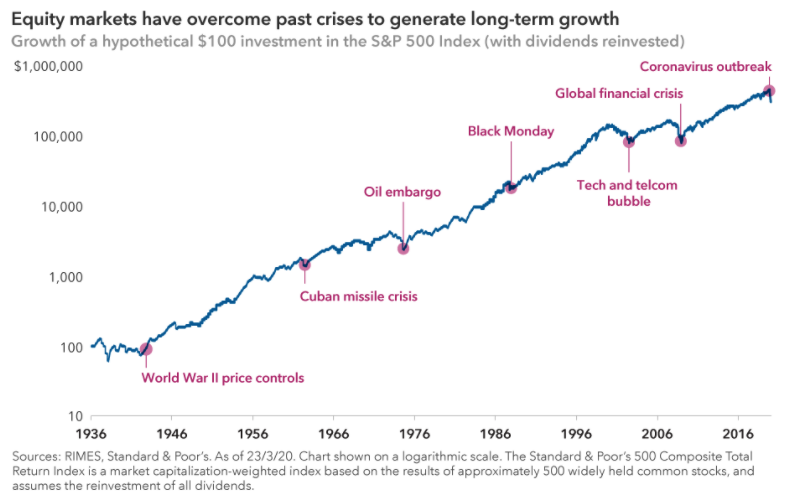

5. Maintain your investment discipline: If you are not a retiree but still working and investing for retirement, you might opt to keep doing so. Given time, markets have always recovered in the past and have the potential to do so after this crisis too. When markets are down, your regular investment contributions will buy more shares or bonds, so you might not want to suspend your payments unless you really have to. Changing your contributions in response to short-term volatility runs the risk of missing out on long-term growth potential.

Position your portfolio to navigate through cycles

Capital Group believes in a smarter way of investing that combines individuality and teamwork into a tailored approach to help investors meet their goals. Find out more by clicking 'CONTACT' below

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The University of Sydney. He also holds the Chartered Financial Analyst designation. Matt is based in Sydney.

3 topics

1 contributor mentioned

Matt Reynolds

Investment Director

Capital Group

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The...

Expertise

Matt Reynolds

Investment Director

Capital Group

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The...

Expertise

Comments

Comments

Sign In or Join Free to comment