7 reasons to be upbeat on the Australian economy

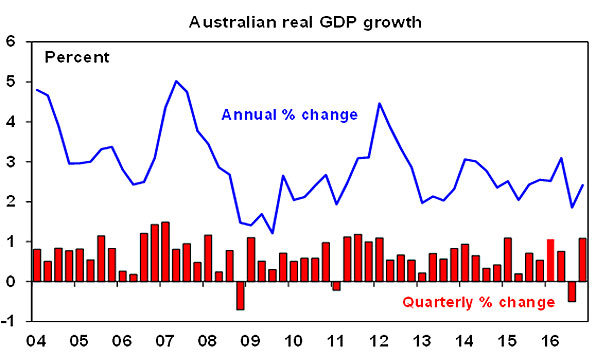

For the last few years, we have heard constant predictions of a recession in Australia as the mining boom turned to bust and a housing bust was seen to follow. Some even went so far as to say that an imminent recession was “unavoidable”. Those fears intensified after the September quarter GDP data showed the economy going backwards. But a 1.1% rebound in December quarter growth highlights that yet again it hasn’t happened. The December quarter rebound was on the back of stronger consumer spending, housing investment, business investment, public demand and export volumes. So where to from here?

Key points

- A rebound in the economy in the December quarter confirms that Australia is continuing to avoid recession.

- There are seven reasons to be upbeat about the Australian outlook: thanks to a more flexible economy Australia is on track to take out the Netherlands for the longest period without a recession; south-east Australia is continuing to perform well; the great mining investment unwind is near the bottom; the surge in resource export volumes has more to go; national income is rising again; public investment is strong; and there are signs of life in non-mining investment. Growth is on track to return to near 3% this year.

- Stronger growth & profits are good for Australian assets.

The Australian worry list

To be sure, aside from global threats, Australia has its own worry list. The key threats and constraints are as follows:

- Business investment plans point to mining investment continuing to fall at the rate of 30% or so a year.

- Housing construction activity is likely to peak this year, a large supply of apartments will hit various cities, affordability is poor, and household debt levels are very high.

- The Australian dollar arguably remains too high and has risen more than 10% from early last year. (That said most countries want a lower currency these days.)

- Unemployment and underemployment at a combined 14% are high. The combination in the US is 9.4%.

- Inflation is too low and risks staying below the 2-3% target for longer reflecting record low wages growth, a rising $A, competitive pressures and weak rents as new supply hits.

- Our political leaders seem collectively incapable of undertaking productivity enhancing economic reforms

That said, most of these concerns are not new and have been discussed endlessly. Endless whinging about them is distracting from the good news.

Reasons to be upbeat on the outlook for Australia

In fact, there remains good reason to be upbeat on Australia.

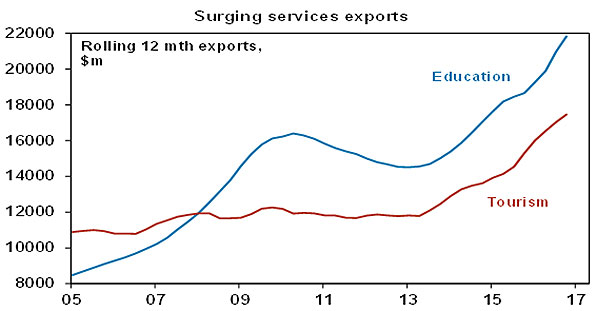

Firstly, at now 102 quarters without a recession, Australia is on track to take out the Netherland’s record of 103 quarters without a recession. This owes a bit to statistical luck, but it also reflects the benefits of the economic reforms of the 1980s and 1990s that made the economy more flexible and sensible macroeconomic management that meant that when the mining boom ended it enabled other sectors of the economy to take over in driving growth. This included housing and services exports like tourism and higher education.

Secondly, reflecting this, the southeastern states of NSW, Victoria and ACT are continuing to perform strongly in a reversal of the so-called two-speed economy.

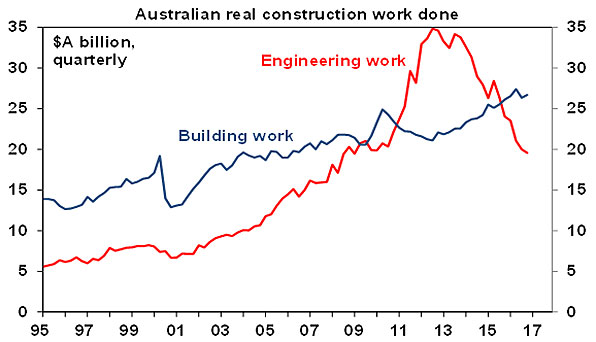

Thirdly, while mining investment is continuing to decline, it’s now a smaller share of the economy so its decline is having a diminishing impact and it’s nearing the bottom anyway. At its peak in 2012 it was 7% of GDP whereas its now less than half that so a 30% annual decline is having half the impact on the economy. What’s more mining investment intentions indicate that by mid next year it will have fallen back to around its long-term norm of about 1.5% of GDP. Engineering construction – which has been dominated by mining activity - has already fallen back to its long-term trend. This means a slowing in housing investment is less of a threat because it will be offset by a lessening in the detraction by falling mining investment.

Fourthly, we are continuing to benefit from the third phase of last decade’s mining boom, which is the surge in resource export volumes as new projects complete – notably gas projects this year.

Fifthly, the blow to national income from the slump in commodity prices has reversed as prices for iron ore, metals and energy have rebounded. While a new commodity price boom is a long way away the rebound is pushing up national income. Amongst other things, this along with booming export volumes is leading to a dramatic shrinkage in Australia’s current account deficit which could soon be in surplus for the first time since the 1970s and the associated surge in resource company profits could knock $8-10bn p.a. off the Federal budget deficit.

Sixthly, public infrastructure investment is ramping up strongly in response to state infrastructure spending particularly in NSW and the ACT much of which is financed from the privatisation of existing public assets.

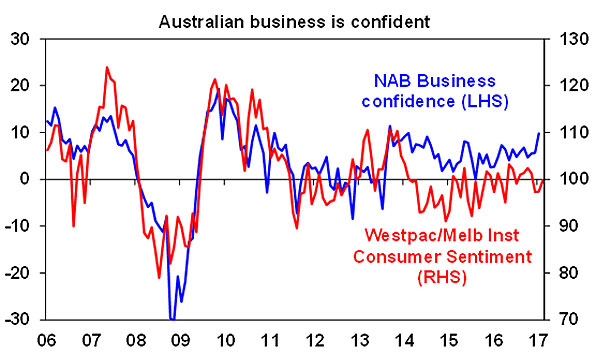

Finally, there are signs of life in non-mining investment. In terms of fundamental drivers borrowing costs have been low for some time but business confidence is reasonably high, profits for non-resource companies are growing around 5% per annum, and capacity utilisation is up from its lows. While mining investment plans for the financial year ahead are around 30% below such plans a year ago, plans for non-mining investment are actually up 7%.

Overall, a recession is likely to continue to be avoided, and economic growth is likely on its way back to near 3% this year.

Interest rates on hold

There remains a case for another RBA interest rate cut: the $A remains too high, slowing housing investment at a time when mining investment is still falling risks slower economic growth, banks are under pressure to raise rates out of cycle and inflation risks staying lower for longer as wages growth remains weak. But against this, growth has bounced back nicely in the December quarter, national income is up and RBA concerns about the threat to household financial stability that may flow from more rate cuts imply a high hurdle to cutting rates again. As a result we are removing the rate cut we had expected for May and now expect rates to be on hold this year. That said if the RBA is to do anything on rates this year a cut is more likely than a hike. A rate hike is unlikely until later next year.

Profit growth goes back to positive

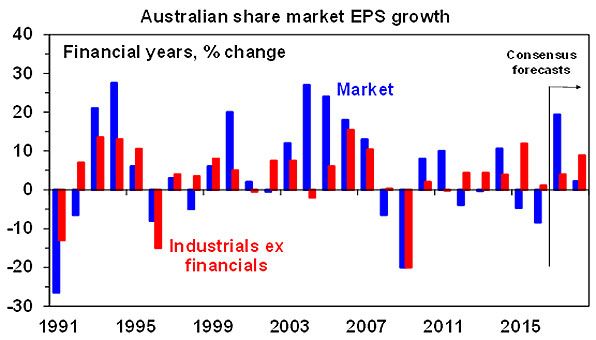

The Australian December half profit reporting season confirmed a very strong return to profit growth. However, this dramatic turnaround has been driven by resources stocks with more modest growth for the rest of the market. In terms of some key statistics: 45% of companies results have exceeded earnings expectations which is around the long-term norm, 59% of companies have seen profits up from a year ago with a median gain of 4% year on year and the focus has remained on dividends with 80% of companies either increasing or maintaining their dividends which is a positive sign of corporate confidence in the outlook.

Consensus profit expectations for the overall market for this financial year were revised up by around 2% through the reporting season to a strong 19%. The upgrade has all been driven by resources companies which are on track for a rise in profit of 150% this financial year reflecting the benefits of higher commodity prices and volumes on a tighter cost base. Profit growth across the rest of the market is likely to be around 5% with mixed bank results and constrained revenue growth for industrials. Outlook comments have generally been positive and as a result the proportion of companies seeing earnings upgrades has been greater than normal. While the bounce in resource profits will slow, profit growth for industrials is likely to pick up reflecting stronger economic growth.

Implications for investors

A return to reasonable growth underpinning reasonable profit growth is positive for Australian assets. With Australian shares up 12% since the US election and trading on a forward price to earnings multiple of 15.5 times which is above the long-term average, the market is vulnerable to a further short-term consolidation or correction. However, the improvement in profits – which is likely to broaden to industrials – should underpin a rising trend in the market on a 6-12 month horizon.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Comments

Comments

Sign In or Join Free to comment