A complete guide to LIC investing

There are now over 100 Listed Investment Companies (or LICs) and Listed Investment Trusts (or LITs) available for investors to choose from on the Australian Stock Exchange (ASX). In recent years there has been a boom, with several fund managers bringing new products to the market. This guide outlines how LICs work and what to look for.

LICs have been available for a long time, but their number has increased substantially, with many managers launching new LICs through initial public offerings (IPOs). Despite the large size of the LIC sector, there is relatively limited attention from institutional researchers and professional investment managers. This can provide more opportunities for mispricing than in other areas of the stock market. In addition, some quality investment managers can only be accessed through LICs.

Unless we specifically differentiate between an LIC and LIT, when we refer to LICs we are referring to both structures.

Through LICs you can now gain exposure to Australian shares, global shares, fixed interest investments, as well as several other alternative investment strategies. Many LICs are run by exceptional managers, using differentiated investment strategies that can help you to diversify your investment portfolio.

At Affluence, one of our core specialties is investing in LICs. In fact, our Affluence LIC Fund only invests in ASX listed LICs. We believe this sector offers investors the opportunity to produce superior risk adjusted returns compared to investing in a passive investment strategy.

Our methodology involves us assessing the quality of each LIC based on various criteria, and then to only buy them at the right price. They key tool we use to identify whether an LIC is expensive or cheap is its trading price on the ASX, relative to the value of the underlying assets it holds (known as the NTA or NAV). This difference between the trading price and NTA is known as the premium or discount to NTA.

Many of the top tier LICs are too expensive some of the time. And so, we patiently wait until we can buy them at the right price.

What is a Listed Investment Company?

A Listed Investment Company, or LIC (pronounced “lick”) is a specialised type of investment fund that pools together shareholders’ money and invests it under an approved investment strategy. LICs are listed and traded on the Australian Stock Exchange (ASX) and other securities exchanges around the world. In many ways LICs are similar to managed funds, exchange traded funds and other collective investment vehicles, but there are also some important differences.

We use the term Listed Investment Company because the majority of these listed active investment vehicles are companies. However, there are some which are Listed Investment Trusts (LITs). The main difference between these two structures is in the tax treatment. Companies pay tax on their earnings and pay dividends to their investors (which are usually taxable to them but include franking credits). Trusts pay no tax directly, but instead must distribute their taxable income to investors, who then pay tax on it at their own tax rates. These distributions usually do not include significant franking or other tax credits.

Why invest in a LIC?

There are many reasons why people invest in an LIC, but the most common are:

- To achieve better diversification in your investment portfolio

- To access the skills of a professional investment manager

- To get exposure to a market, asset class or investment strategy

- To access the benefits of an unlisted managed fund with the ease of trading and liquidity of traded shares

- To receive income from dividends or distributions

- To profit from the change in premium/discount of the NTA compared to the share price

How do LICs work?

Like other companies, an LIC is overseen by a board of Directors, whereas a trust is overseen by a responsible entity. Their functions are similar, and in both cases the day-to-day investing activities are carried out by specialist investment managers. These managers are appointed or employed by the Directors of the LIC or the responsible entity of the LIT.

Most LICs are externally managed. This means the investment manager is an external company appointed under a formal contract. The appointment usually lasts for a fixed term of 5 years or more and may be terminated or extended at the end of that period. The investment manager charges a fee to the LIC, usually calculated as a percentage of the net assets of the LIC. There may also be an additional fee payable where performance of the investment portfolio exceeds a certain return benchmark. In most cases where the performance of the investment manager has been acceptable and their fees are reasonable, they will be asked to continue at the end of the management contract period.

An alternative structure is an internally managed LIC. In this case, investment staff are employed by the LIC directly. Instead of paying an external manager a fee, the company pays the employment and associated costs of the investment staff. Internal management can be a more attractive proposition for a large LIC because the cost of managing the investments can be more efficient and this can improve returns. However, for most LICs external management makes more sense because the size and scale of activities is not sufficient to make it efficient to manage internally.

LICs have low minimum investments. LICs can be bought and sold daily on the ASX. So long as you have an account with a stockbroker, you can invest in a LIC on the ASX for as little as $500. Brokerage costs usually mean it is better to buy a larger parcel than this to average out the transaction costs.

Unlike an unlisted managed fund where units are purchased and sold in accordance with the Fund’s unit pricing policy, with an LIC the ‘market’ determines the security price. This can lead to situations where the share price and value of the underlying portfolio vary dramatically. LICs can issue and buy back shares, but generally this only happens at certain times.

How do LICs invest?

All LICs have an investment strategy. Generally, the investment strategy will define:

- The asset class the LIC invests in (e.g. Australian shares).

- The return target the LIC is aiming to achieve and the timeframe for achieving those targets (e.g. to outperform the ASX 200 Index over 3 year periods).

- Any investment limits or ranges that will be adhered to (e.g. maximum level of cash holdings, maximum level of investments outside Australia).

All funds within the LIC are pooled together and invested in accordance with the investment strategy.

How do LICs generate returns?

As an investor in a LIC you will receive returns in two ways.

Firstly, most LICs pay regular dividends (or distributions for LITs). These dividends usually include at least partial franking credits and are generally paid from underlying profits generated by the LIC over time. LITs don’t pay franked dividends, however they do pass on any franking credits they receive from underlying investments.

The second source of returns is that the share price of an LIC will increase or decrease over time. The price at which LICs trade on the ASX is set by market forces and is impacted by many factors. Some of these factors may include:

- The reported NTA for the LIC.

- Market conditions and investor confidence.

- The attractiveness of the investment strategy.

- What asset class the LIC invests in.

- The level of the dividend yield (this is never the correct method to price an LIC).

- Performance of the investment manager.

- Cost of running the LIC, including fees to the investment manager.

- How large the market capitalisation of the LIC is, and how liquid its trading is.

- How well the LIC markets itself and communicates with current and potential investors

- Whether the directors and investment managers treat their shareholders with respect, and understand that it is the shareholders money they are investing

There are also many other factors that can impact the price an LIC trades at. To have the best chance of achieving above-average returns over time, it’s important for you to consider a range of factors and to try to buy at an attractive price. We cover this concept in greater depth later in this guide.

The LIC Sector

Listed on the ASX, there are over 100 LICs and LITs with a combined market capitalisation of over $40 billion. They range from small sub-scale vehicles of less than $5 million to the Australian Financial Investment Company (ASX: AFI) which has a market capitalisation of almost $7 billion.

Many investors have only ever heard of the biggest three LICs; Australian Financial Investment Company (ASX: AFI), Argo Investments Limited (ASX: ARG) and Milton Corporation Limited (ASX: MLT). These three combined have a market capitalisation of approximately $16 billion, which accounts for approximately 35% of the total sector.

Given their size and concentration, it is understandable that this is where a lot of investors focus in the sector. However, there are some important similarities between them:

- They are all internally managed and reasonably low cost.

- Their portfolio construction is usually very similar to the major benchmarks.

- Over the longer term, their performance is equal to the major benchmarks at best (and in many cases they have lagged).

Given their similar portfolios and being very benchmark aware, there is limited diversification benefits available by holding more than one of them. Given they invest, and thus perform, similar to the market index, many investors make the mistake of purchasing these LICs at a premium to underlying NTA. Doing this sets up the investor for a high probability of underperforming the market. On occasions, these LICs can trade at reasonable discounts to NTA. Buying these LICs at a discount can be a good opportunity to improve long term returns.

For those investors who are just looking for market-based returns, a low-cost ETF or index fund may be a better alternative.

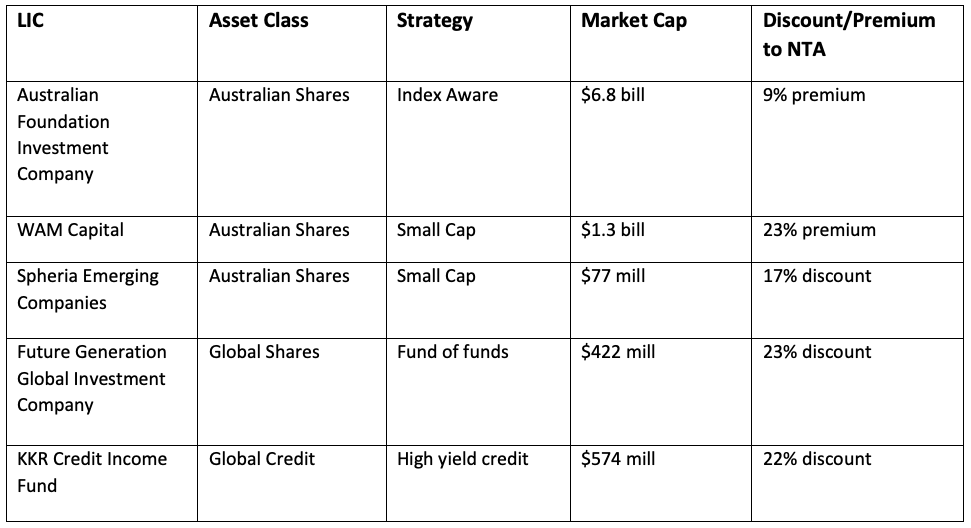

As an example of the variety that is now available in the LIC sector, we have set out below some LICs which are offering investors something quite different. We are not endorsing the quality or attractiveness of any of these LICs (depending on price it is likely we would hold or sell them at different times), just showing the huge range of asset classes, strategies, discounts and sizes that are available.

Market cap and discount/premium to NTA as at 31 March 2020

Understanding the strategy

For each LIC, we like to develop a detailed understanding of the investment strategy being employed. This is key to understanding how an LIC might fit into your existing portfolio. This information can be found in a few places, but most commonly in the Annual Report, on the LIC website (if it has one) or in regular investor reports lodged with ASX.

Some key information you might want to know is:

- What type of assets does the LIC invest in? Does the LIC focus on a small, niche market or does it invest more broadly?

- What geography does the LIC invest in? Is it focussed just on Australia, in one or a combination of overseas markets?

- What are the LICs return objectives? Has it managed to achieve those objectives? What should the LICs performance be measured against?

- How much discretion does the fund manager have within the asset allocation strategy? (e.g. can they hold a large amount of cash if they cannot find compelling investment opportunities?) Some of the best LIC performers historically have tended to be those which have the most discretion, particularly around cash holdings. They also tend to have less volatile performance in down markets.

- Does the manager invest in line with the benchmark, or are they truly benchmark unaware?

- How concentrated are the holdings of the LIC? Some managers hold 50-100 stocks and are very diversified. Others may hold 15 stocks or less. Concentrated portfolios can increase the potential for outperformance, but also the potential for large underperformance.

- How does the LIC aim to beat the market? What is the advantage they have that will allow them to beat the market average?

- How will the LIC complement your investment portfolio? Are they doing something or investing in something that is different to what you currently hold? If so, this can allow you to achieve greater diversification.

If you have time, it may make sense to review the last 3-5 years ASX announcements, particularly those marked as price sensitive. This may assist to provide additional background on the LIC and to understand if the Board or management have deviated from or changed strategy during that period.

Buying at the right price

Having looked at the quality of an LIC, and determined that you would like to own it, the next part of the equation is making sure you buy at the right price. At Affluence, we do this by applying a four-stage process:

- Is the underlying market the LIC invests into trading at an attractive price?

- What is the current NTA value per share?

- How does the current ASX buy price compare to the NTA?

- What is the price at which we would like to buy?

Underlying market value

Before investing in an LIC, you need to consider whether the asset class the LIC invests in is cheap, reasonable value, or expensive. If the underlying investments are very expensive, the LIC is likely to produce a lower investment return over the medium to long term. This can be a very difficult assessment to make, but one of the questions it may be useful to ask is “would I be happy to own these investments directly?”

If you believe the asset class is expensive, then it may be prudent to be patient and wait until you believe there is more value before considering the LIC, or to make a small investment now, and monitor for signs of greater value in the future.

Net Tangible Asset value per security

NTA per security is the key variable (along with the share price on ASX) to determine whether an LIC is good value. ASX requires the NTA per security to be published by all LICs at least monthly, and this must be done by the 14th of the following month. Some LICs will provide NTA data more often (weekly or even daily), but many still only report monthly.

Because the NTA data is usually out of date, it needs to be considered in light of market movements since the last NTA date. For example, if the LIC invests in a diverse portfolio of ASX stocks and the ASX 200 Index has fallen 5% since the end of the last month (when the NTA per security was last reported), it is likely the NTA of the LIC will also have fallen during this period. It is difficult to estimate with certainty the exact NTA between reporting dates, but you can broadly estimate it if you understand what the LIC is investing in.

When reporting an NTA, an LIC may provide more than one NTA value. There are up to three NTA calculations that are commonly provided:

- NTA before tax. This calculation does not make any allowance for tax on current years’ income and profits and therefore does not reflect the tax that will be paid/payable by the LIC for the current tax year.

- NTA before tax on unrealised gains/losses. This calculation allows for income tax and for capital gains tax on any investments sold in the current financial year. It does not allow for tax that would be payable if all current investments were sold.

- NTA after tax. This calculation incorporates tax on income and realised capital gains and also allows for tax that would be payable if the entire investment portfolio was sold.

In most cases, we believe the most appropriate value to use is the NTA before tax on unrealised gains/losses. This reflects the position after allowance for tax payable on current year earnings and capital gains, but before any deferred tax on the remaining investment portfolio.

If the LIC has stated an intention to wind-up or otherwise dispose of all or a substantial portion of its portfolio, it may be more appropriate to use the NTA after tax.

What is the right price to pay?

It is fair to say we prefer to buy LICs at a discount to their NTA. But in our view, there is no one rule which determines the right price to buy an LIC, relative to its NTA value. There are a whole range of factors to consider.

One of the key factors we consider is the price and NTA history. If we can, we prefer to study how an LIC has traded historically relative to its NTA. This data is sometimes published by the LIC. It may also be available through your broker research.

If you can buy at a price below the average discount/ premium, calculated over a reasonably long period, this can be a good indicator of value. Other factors which you might wish to take into account when considering your preferred buy price are:

- Historical performance – LICs which have performed very well tend to trade at a premium, or at a lower discount than comparable LICs. In some case it is worth it, but it will depend on the extent of the premium you are paying. By and large, we prefer to be patient and wait for an opportune entry point. Conversely, periods of short-term underperformance by an otherwise excellent manager can provide opportunities to buy in at a good price.

- Size – Larger, more liquid LICs tend to trade at higher prices relative to NTA, whereas smaller LICs are more likely to trade at a discount.

- Underlying assets – LICs that invest in offshore markets or unlisted investments tend to trade at bigger discounts than those who invest in larger, more liquid Australian stocks.

- Portfolio concentration – Some LICs have very concentrated portfolios, where one or a few investments make up a large proportion of the portfolio. These tend to trade at bigger discounts because of the additional concentration risk in the portfolio.

- Investor confidence and market performance – in times when confidence is low, which tends to be during market corrections, LICs can trade at larger discounts. When confidence is high and/ or markets are fully valued, LICs tend to trade at higher prices, relative to NTA.

These are just a few of the many variables which can impact the price at which a LIC trades, but we have found over time that they tend to be the most prominent.

Below are two examples of the change in discounts/ premiums to NTA that can occur over a long period.

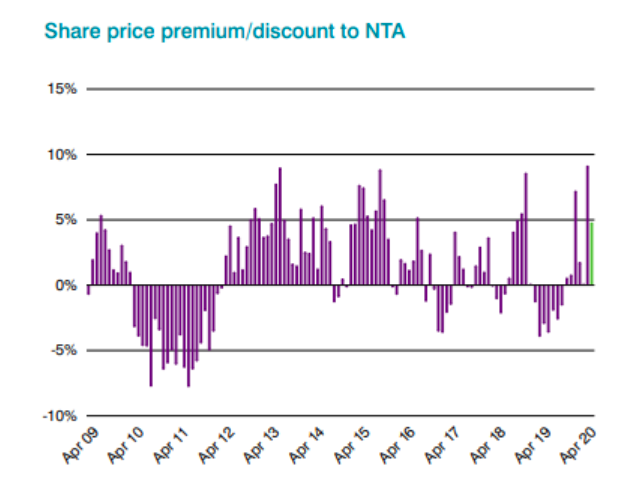

The first is from the largest LIC, AFIC (ASX: AFI). Over the past 10 years AFI has traded in a range of between a 9% premium and an 8% discount to NTA. Given that AFI portfolio performance has been at best similar to the ASX 200 Index, it’s easy to see how an individual investor's performance could be substantially different depending on the discount/premium when they first invest. Armed with this type of information, it is obvious that one way to potentially improve returns from AFI is to buy it at a discount and potentially sell when trading a premium.

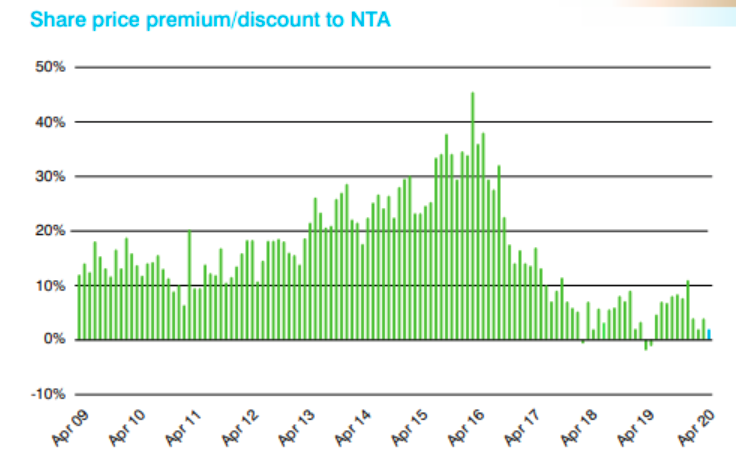

The second example is from AFI stablemate, Djerriwarrh (ASX: DJW). DJW is slightly different in that while it holds a very benchmark aware portfolio, it also sells options to generate additional income at the expense of potential future capital gains. This leads to portfolio performance that is generally a little behind the ASX 200 Index, however it pays a high dividend yield which historically was chased by yield hungry investors. This chase for yield resulted in investors valuing DJW on a dividend yield basis, which at one point forced it to a more than 40% premium! So, if you bought DJW in 2009 or 2010, by 2016 you would have benefited not only from strong market returns but also from the premium increasing from around 10% to 40%. Since then, reality has finally set in and this stock fell to a discount in 2019, resulting in significant underperformance since 2016.

In conclusion

Like all investments, it is best to do your homework properly before buying any LIC. We suggest you consider only quality LICs with proven managers who have performed well in the past. Ensure those LICs hold assets you like and have an investment strategy you understand, with an appropriate management structure in place. Understand how an LIC will fit into your portfolio and how you expect it to assist you in achieving your investment goals. Most importantly, try to buy at the best possible price you can, relative to the value of the underlying assets and the trading history of the LIC.

Invest in LICs without the hard work

The Affluence LIC Fund invests exclusively in LICs and LITs on the ASX. The fund seeks to take advantage of inefficiencies, allowing investors to gain exposure without the need to research each security. To request additional information please email invest@affluencefunds.com.au or click the ‘CONTACT’ button below.

Affluence Funds publishes monthly member-only reports on opportunities in the LIC space. Register on our website to receive these reports to your inbox.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Daryl has over 25 years’ experience in finance and investing. He formed Affluence to provide investors with regular income and long-term capital growth by investing with some of the best fund managers available in Australia.

........

This article is prepared by Affluence Funds Management Limited ABN 68 604 406 297 AFS licence no. 475940 (Affluence) to enable investors in Affluence Funds to understand the underlying investments of the funds in more detail. It is not an investment recommendation. Prospective investors are not to construe the contents of this article as tax, legal or investment advice. Neither the information nor any opinion expressed constitutes an offer by Affluence, its subsidiaries, associates or any of their respective officers, employees, agents or advisers to buy or sell any financial products nor the provision of any financial product advice or service. The content has been prepared without considering your objectives, financial situation or needs. In deciding whether to acquire or continue to hold an investment in any financial product, you should consider the relevant disclosure documents for that product which are available from the product provider. Affluence recommends you consult your professional adviser to determine whether a financial product meets your objectives, financial situation or needs before making any decision to invest.

2 topics

4 stocks mentioned

Daryl has over 25 years’ experience in finance and investing. He formed Affluence to provide investors with regular income and long-term capital growth by investing with some of the best fund managers available in Australia.

Expertise

Daryl has over 25 years’ experience in finance and investing. He formed Affluence to provide investors with regular income and long-term capital growth by investing with some of the best fund managers available in Australia.

Expertise

Comments

Comments

Sign In or Join Free to comment