A contemporary business 40 years in the making

Data #3 is an IT services company with a rich history dating back almost 40 years. Since listing in 1997, the company has grown to over 1,100 employees and has expanded its services capability beyond Queensland. Last financial year it posted over $980m in revenue, with net profits growing 30% from the previous year.

Read the long-term trends and adapt accordingly

Whereas in the past Data #3 was viewed as more of a “box reseller”, these days the conversation with the client is more about how Data #3 can design and implement a solution to facilitate the client’s need for mobility, cloud and security. The client can then focus on core business while knowing there is a flexible, scalable and nimble IT capability running in the background.

Transformation in the P&L as well

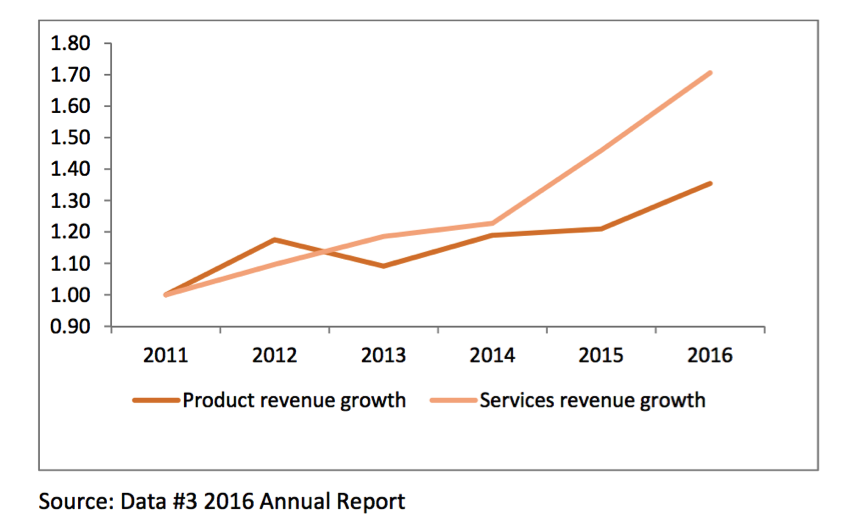

15 years ago, Data #3’s revenue line would be dominated by lumpy one-off type product sales. Margins were thin, reflecting limited opportunity to add value as well as strong competitive pressure. Fast forward to now and the services revenue has expanded at double digit levels.

Product sales last financial year amounted to $794m (6% compound growth since 2012) while services revenue has grown by 11% to $187m. As the chart below shows, since 2010 services related revenues are over 70% higher, while product sales are up 35% over the same period.

In addition, services revenue can be recurring in nature which is a coveted attribute for investors given improved visibility and lower volatility compared to the swings and roundabouts of product sales.

More importantly, a contemporary service offering where companies like Data #3 are taking on a much more strategic role than in the past means the profitability margin on services revenue is generally a lot higher than the margin earnt on a simple hardware resale. Meanwhile, the company maintains a strong balance sheet with virtually no debt and very high cash levels.

Risks to consider

NovaPort believes one of the biggest risks was the undertaking to transform Data #3 from a “box reseller” to a provider of more complex and strategic outcomes based services solutions to the end market. While still early stages, Data #3 has made more than solid progress without jeopardising the balance sheet or just as importantly, it’s hard won reputation in the market place. Nevertheless, we constantly monitor the company’s macro-associated risks related to business confidence levels and changes in technology trends, as well as the risks specific to its client makeup and the ability to deliver on contracts.

NovaPort Capital is a boutique Australian equities investment manager specialising in small and microcap ASX-listed companies. For further stock insights from NovaPort, please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

NovaPort Capital is a boutique Australian equities investment manager specialising in small and microcap ASX-listed companies. NovaPort is a benchmark unaware, active investment manager.

1 stock mentioned

NovaPort Capital

NovaPort Capital is a boutique Australian equities investment manager specialising in small and microcap ASX-listed companies. NovaPort is a benchmark unaware, active investment manager.

Expertise

NovaPort Capital

NovaPort Capital is a boutique Australian equities investment manager specialising in small and microcap ASX-listed companies. NovaPort is a benchmark unaware, active investment manager.

Expertise

Comments

Comments

Sign In or Join Free to comment