A couple of hot stocks

A2M is up 9% in two days helped by the BAL earnings upgrade. It has also announced it will expand its brand throughout the North East of the US starting this month. The area is home to 60 million consumers which according to research from A2M accounts for 20% of the total milk volume in the US. The move will see A2M increase its range from around 3,600 stores to approximately 5,000 stores and will be supported by increased marketing investment from the “Love Milk Again” campaign.

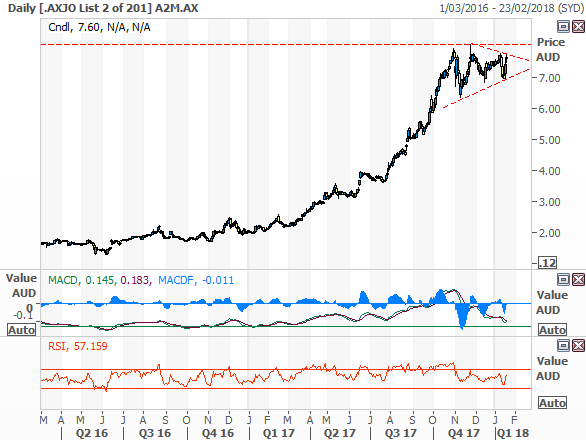

The stock has been going sideways for the last three months, it will be interesting to see if it breaks out of that trading range to the upside or downside – see chart below.

We don't hold it unfortunately.

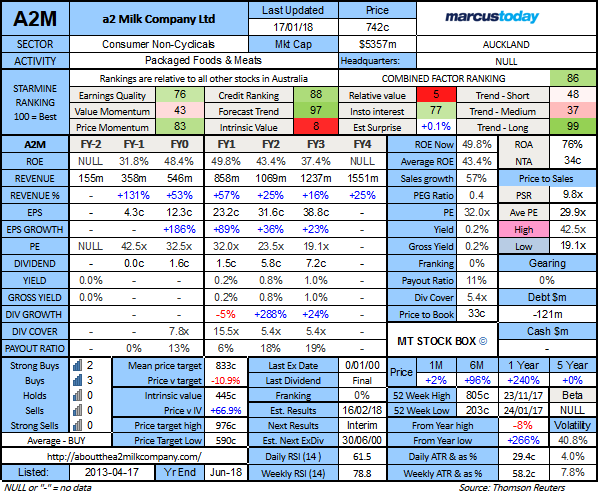

The numbers on A2M

This is a Marcus Today Stock Box. A PE of 32x is not quite the 70x that stocks like DMP got to when its hair was on fire. However, it’s not so high that it would prompt you to sell it on price alone. Not with a return on equity of almost 50% and significant earnings growth in the forecasts. Sentiment is good, all the brokers are buyers or holders (see table on right), and it is still 11% below the average broker target price. It is 8% down from the year high. Results in February will be crucial, but the tide is with it and the odds are on the results being good not bad. It's the sort of stock that will get smacked when the market turns over, but, if I held it, I'd hold it and see which way this price breaks next.

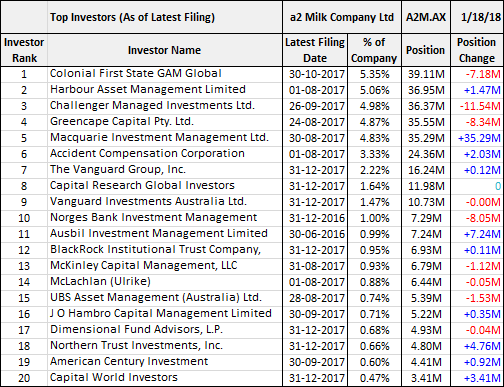

A2M share register

There's a bit of movement on the share register. Challenger, Colonial First State (a top performer in the mid-cap space) and Greencape were all selling in August, September and October but don't appear to have done anything since and still have big holdings. Macquarie Funds Management bought 35 million shares in August and notably, Macquarie the broker has been pumping out ‘buy’ recommendations ever since. The most recent notable movement was Norges Bank who sold 8 million shares in December. A lot of the mid-cap stock pickers took some profits when the share price plateaued last year but appear to retain some longer-term faith.

Technical view

With the markets flying, and the news flow good, a break above the all-time high of 796c is looking more likely than a break down at this point. Now 760c. A break above 800c will attract some technical attention. On the chart there is a bit of a sort of "Pennant" formation. The technical interpretation of that is that if the stock breaks out of the pennant to the upside you buy it, and if it breaks to the downside you sell it.

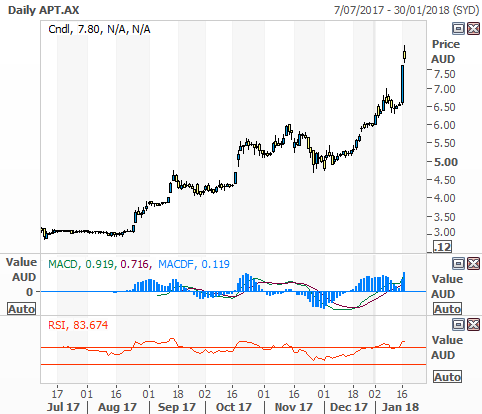

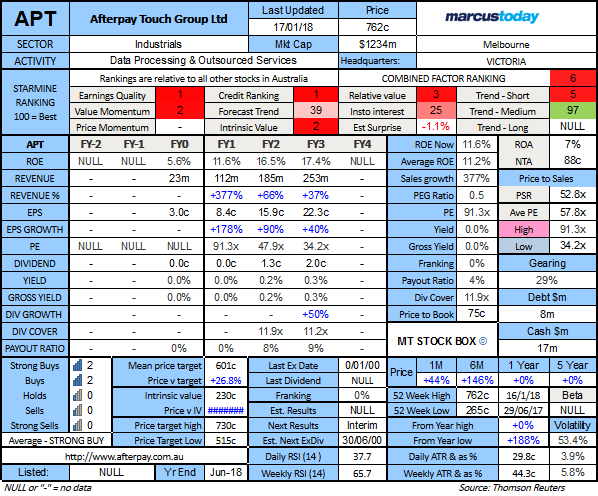

AFTERPAY (APT)

APT was up again yesterday, up 2.36% to 780c after a 16.8% rise the day before. They are up from 650c to 780c in two days on the news they will be entering the US market through a partnership with technology-based private equity fund, Matrix Partners.

Bell Potter lifted their target price 26% on the news and says the entry into the US market will add around 43c to APT’s valuation. Matrix bought $18.75m worth of stock in the company for $6.51 and had negotiated for one of its general managers, Dana Stalder to join the APT board. Matrix will also take 10% of APT’s future growth of its US subsidiary, expected to be more than $US50 million.

The AFR yesterday pointed out that Afterpay can turn over its lending book approximately 11 or 12 times a year with their current repayment rate of 30 days. This would allow them to finance $4 billion worth of sales annually when taking into account the company’s equity and loan facility from NAB.

I had been wondering why the banks haven't created their own Afterpay style offering to blow APT away, but it seems they are backing it rather than beating it. NAB is encouraging NAB customers to link up to Afterpay with debit and credit cards. And for those wondering about solvency, there is an incentive for customers to repay on time and penalties for those who don’t, with possible suspension and a late fee of $10 for a missed payment.

"Afterpay" is becoming a verb, and what more could you ask for a brand. We hold it in the SMA and will continue to do so despite the fact it is overbought. When the market tips over no one will be blamed for taking profits in high performing, high multiple mid-caps, but the Afterpay story means I will also look to buy back in when the market starts going up again.

There is only one broker recommendation listed on FN Arena - Ord Minnett has a BUY recommendation and a 950c target price, 20% above the current share price.

Here is the chart:

Here are the numbers from the Marcus Today STOCK BOX:

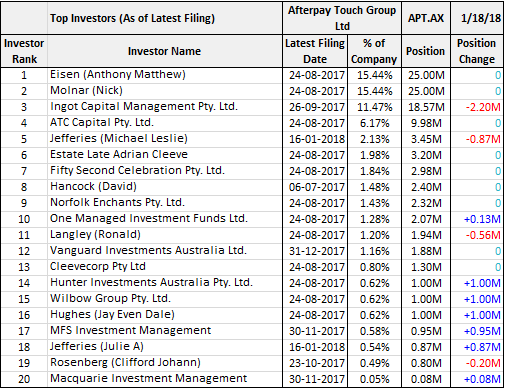

Here is the share register - not a lot to go on:

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and informing private investors with insightful, honest, straight-up independent stock market research and ideas. Marcus likes to call it as it is without agenda, puts subscribers first, and this has paid off for real people with real money.

1 topic

1 stock mentioned

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and...

Expertise

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and...

Expertise

Comments

Comments

Sign In or Join Free to comment