A different kind of Energy Disruption

When we are asked to think about key disruptors that have changed the world in the past 20 years most of us will reel off a list of applications or companies like Uber, Electric Vehicles/Tesla and Facebook. Many of us will ignore some of the less obvious disruptors.

A lot of this disruption has driven or been created by (there is a big chicken and egg argument here) the increasing immediacy of society. We want to know where the car that is taking us to the airport is, we don’t want to post letters that take days to arrive and we want our Friday night takeaway at our doorstep as soon as we push a few buttons.

Unconventional oil and gas as a disruptor

One disruptor that has dramatically changed an industry and potentially shifted the course of global politics and economic strength has been unconventional oil and gas production. We wrote 18 months ago on the question of whether shale was a Ponzi scheme, an admittedly sensationalist headline. At the time we were quoting a Company senior management’s comments when we used this headline, but the fact is shale is markedly different to conventional oil.

The typical large conventional oil field we think of multi-billions of dollars being invested, multi-year build time following an FID decision and then a steady to declining field profile. Unconventional drilling is quite different as we all know in that rightly or wrongly we focus on single well economics of a field and staged production of those wells. Drilled and ‘un’completed wells DUCs means that production can be staged a lot more immediately and the marginal production is coming from a source where production decisions can be made in a matter of months not years.

The disruption is on marginal production and can’t be applied universally. An analogy that we would use is that it’s like you’ve developed Uber, but you can only use it to get to and from the airport and not for any other commutes. We have seen the impact of this disruption on the reaction to higher oil prices. In September 2018 on the back of declining global production and the belief of a strong global economy (Brent) oil hit USD80/bbl. The growth rates coming from North American shale during the 2H highlights the immediacy of production decisions and the disruption unconventional production can cause to the market and this observer’s oil price projections!

BHP’s cumulative shale losses, the trials and tribulations of Sundance Energy and failed pursuits of companies like Red Fork and Lonestar have left many ASX investors sceptical about North American unconventional producers. We get that, we were in that camp! However, investors should not forget that strong management teams with the right asset at the right time in the cycle can generate value. It was only 5 years ago that Eagle Ford producer Aurora Oil and Gas was taken over by Baytex for USD1.65bn. At the time the company had 22,000 acres and 166 mmbbls of oil.

The successful Aurora team have a second swing

Australis represents the (Aurora) Management team’s second swing and we are backing them to achieve success with their foray into the Tuscaloosa Marine Shale “TMS” (and Portugal).

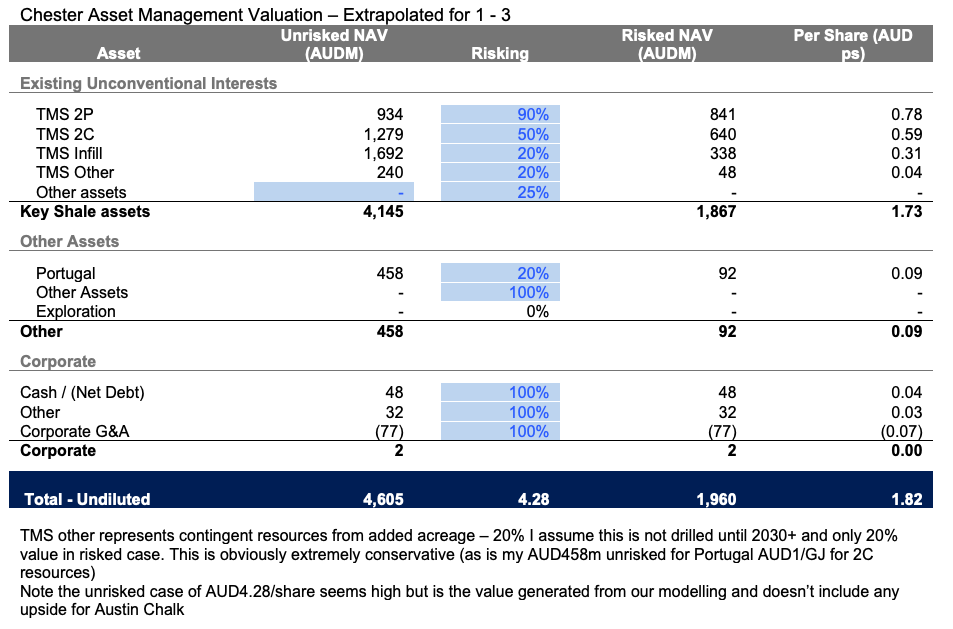

We model a base case using USD60/bbl oil on the TMS base company type curve, from 15 Encana wells drilled over 4 years ago) and get a valuation of AUD0.90/share. Upside exists from several factors: Well improvements (capex and higher IP rates), decreased well spacing from 250 net acres (infill drilling), Austin Chalk, additional acreage, Portugal (maturation of the play). Not to mention higher oil prices!

Since the start of 2019, there have been 3 material announcements that have impacted our view of ATS:

1: Stewart’s Well IP-30 rate

The Stewart 30H-1 well is the first well in what is now an 8-10 well program. The rate that this flowed suggested a 34% improvement on the IP-30 base type curve modelled by us and endorsed by ATS Management (and reserves certifier Ryder Scott). Notably this well was also drilled at a cost of USD10.3m (materially below our expectations). The base case doesn’t factor in any upside for technology gains and capex savings from wells that have been experienced across other plays in the past 4 years. Extrapolating this well, assuming the 34% IP rate also equates to a 34% increased recovery per well and development wells at USD9/well, our valuation more than doubles.

2: The company raised capital (announced 15 February)

At the time (and now) we considered a capital raising a prudent approach. Oil pricing is volatile and there are plenty of ASX examples including Sundance Energy and Elk petroleum whereby the oil price has worked against highly indebted companies. We’d much rather see a company take a prudent approach to its balance sheet

3: ATS provided a drilling program update highlighting technical issues with the 4th of their wells

Management noted that a downhole tool had failed with Williams 26H-2 before a drill string became stuck while pulling out of the hole. Prudently Management took the approach not to attempt fishing operations to retrieve the Bottom Hole assembly but to complete the well in its current form. This is well #4 of the program and is the second issue encountered after those experienced with Berghold 29H-2. Wellbore issues of the Williams 26H-2 well are more typical of difficulties encountered in the TMS historically by previous operators. ATS had been utilising a drilling design that was consistent with best practice achieved in 2014 by previous operators and had proven effective until the very last step of the William 26H-2 well. The company had already decided, prior to this issue being identified on 24/2/2019 to apply new technology to the drilling fluid system used in drilling wells 5 onwards. Although the latest hiccup is not ideal, the share price reaction to the announcement has been violent. We can only assume those selling are inferring at least one of 2 things:

- Management was aware of the issue prior to announcing the capital raise on 15/2/2019 (which we don’t view as possible!) and; or

- The 2 well issues should be extrapolated across the play and means it doesn’t work. To this point we would remind holders of a few points:

- These 4 wells are not the only wells drilled to date in the TMS! This seems somewhat an obvious point and is evident in every one of ATS’s presentations that the IP-30 type curve is based on Encana’s last 15 wells and there were another 35 wells (older wells from Encana and other operators) in the play that show production

- The Berghold issue is different to that experienced with the Williams well and extrapolating the Williams well issue ignores that fact

- Wells do fail. Obtaining the exact % of well failure rates is difficult as it is not a figure E&P companies readily report but studies show failure rate for unconventional wells have typically averaged 5-10% across plays. Obviously, experience helps a company to reduce well failures over time

- Even if wells fail ATS’s reserves and resource numbers are generated by an independent source (Ryder Scott) based on available information across the play

In relation to the points above we have increased our assumed failure rate from 5% to 15% which reduces our valuation by ~10%.

Say that despite the evidence you still refuse to accept that the TMS as a play works, the independent reserve certifiers are incompetent and Management of both Encana and ATS have lied to everyone. The share price in that far-fetched scenario still isn’t 0.

Portugal imports all its gas and ATS has a 458bcf discovery onshore Portugal that the market just doesn’t value. It’s contingent not prospective which basically means the gas has been discovered but not fully appraised and we know that appraised gas fields in gas short markets often fetch >$1/mcf (Waitsia in WA being a recent example and WA isn’t even short gas). So, an upside case for Portugal could be AUD500m (AUD0.50/share) if appraised, but we don’t think it is out of the question to suggest that the gas could be worth at least AUD0.35/mcf and underwrite the current share price of the company (AUD0.16/share + AUD0.07/share net cash).

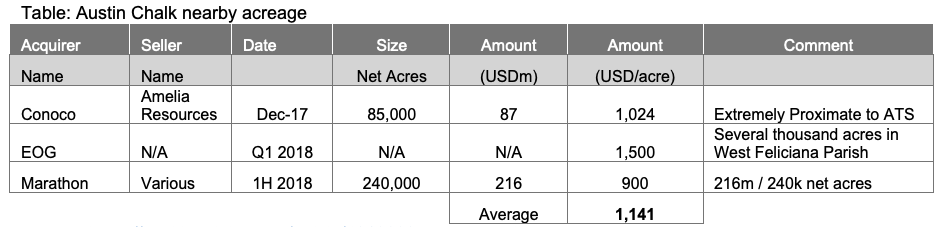

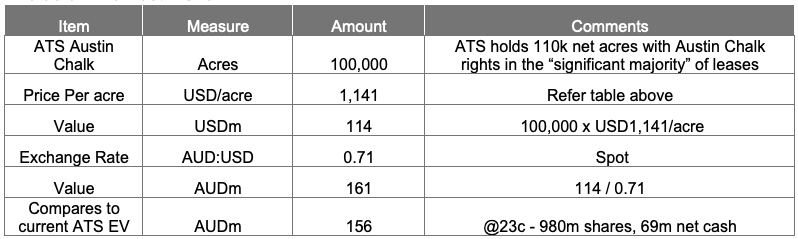

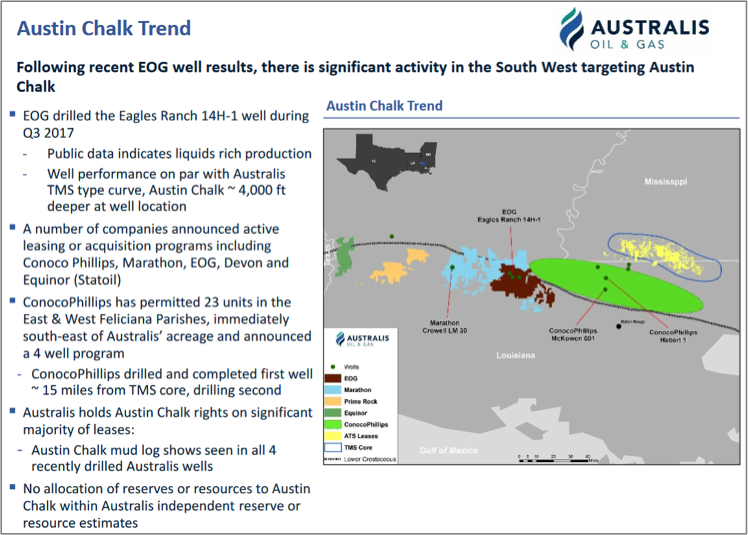

If you still choose to believe that Portugal isn’t worth anything than the last bit of optionality for ATS is the Austin Chalk. There is no question that the Austin Chalk is a developed play and has been exploited throughout Texas but the extension of the play into Louisiana and Mississippi (where ATS holds its acreage) is garnering increasing interest. ATS makes little mention of Austin Chalk and the market doesn’t give ATS any value for it, yet other operators: EOG, Marathon and ConocoPhillips, have been acquiring Austin Chalk acreage around ATS. Some of these transactions have not been significant enough for large announcements by these operators but amounts have been published. ATS holds Austin Chalk rights on the “significant majority” of ATS leases. If we take this to mean 100k net acres (out of 110k) than we can calculate a rough value of ATS’s Austin Chalk rights that aren’t valued by the market.

Sources: seeking alpha; and the advocate

Value of ATS Austin Chalk

Source: Chester Asset Management

Our calculation shows that Austin Chalk rights alone are comparable to the current share price of the company and we would not be surprised to see an operator like Marathon showing interest in acquiring or partnering with ATS.

Source: Australis investor Presentation March 2019

In conclusion

So, with some disruptors stretching the friendships of price to valuation, ATS is one we feel has upside (and downside valuation support) worth considering, particularly in this panicked/emotionally driven sell-off.

We have provided our extrapolated valuation above but will wait to judge whether we adopt this as our reference valuation following the full 10-well program.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chester Asset Management is a high conviction equities fund manager co-founded in 2017 by Rob Tucker and Anthony Kavanagh, with a 25-40 stock benchmark unaware strategy comprised of predominantly broadcap (ASX300) stocks.

2 stocks mentioned

Chester Asset Management is a high conviction equities fund manager co-founded in 2017 by Rob Tucker and Anthony Kavanagh, with a 25-40 stock benchmark unaware strategy comprised of predominantly broadcap (ASX300) stocks.

Chester Asset Management is a high conviction equities fund manager co-founded in 2017 by Rob Tucker and Anthony Kavanagh, with a 25-40 stock benchmark unaware strategy comprised of predominantly broadcap (ASX300) stocks.

Comments

Comments

Sign In or Join Free to comment