A good year ahead for resources

Tim Hannon

Conrad Capital Group

We have argued the case for an exposure to the resources sector for over 12 months. Despite the excellent performance of the sector over this period, we continue to remain confident as our multi-pronged investment case remains intact.

The demand side for cyclicals is supportive

The initial foundation of our positive view on resources, and cyclical companies generally, is that global industrial production is growing strongly. Every major global economy is experiencing robust economic conditions. This is a very positive backdrop for consumption of metals and other commodities.

We expect this positive economic momentum to continue because financial conditions are likely to remain accommodative (interest rates remain low). Our interest rate view is predicated on a current lack of wage inflation as well as our observation that central banks seem unwilling to allow interest rates to increase materially in case it derails the global economic recovery.

The supply side for cyclicals is supportive

The other factor supporting our positive view on commodities is supply side discipline.

Firstly, the Chinese government is dictating forced production cuts of major commodity groups – including aluminium, paper, concrete, steel and coal. This order is driven by the government’s objective of increasing the price of commodities to improve the profitability of these industries, as well as repair the environment.

Adding to the supply side argument is the behaviour of major resource companies themselves. They are not responding to higher commodity prices with supply expansion plans. Just two years ago, the resources industry went through an existential crisis, with major companies like Glencore almost entering bankruptcy. This experience has left most Boards and Executive teams keen to reduce debt and reluctant to expand production. This behaviour is very supportive for commodity prices, and commodity companies.

Market dynamics supportive of commodities and resources

Strong demand from the economic cycle, and disciplined supply growth has been supportive for commodity prices over 2017. We expect more of the same over 2018.

Major resource companies will likely continue delivering earnings upgrades, reducing debt and undertaking share buybacks and increasing dividends. All these outcomes are very supportive of equity values.

Commodity demand from electric vehicles

The resources sector is not just a beneficiary of strong global demand and disciplined supply though. The future growth of the electric vehicle industry is creating new demand for some commodities. Our analysis suggests the growth of electric vehicles will see a greater requirement for lithium, nickel, cobalt, copper and rare earths.

The global car industry

The total stock of vehicles on the world’s roads is estimated at 1.0 billion and forecast to rise to 1.2 billion by 2035. The average estimate for annual global passenger car sales is approximately 100 million. Based on global population growth and greater car ownership levels in developing countries such as China we forecast this number rising to 130 million per annum by 2025.

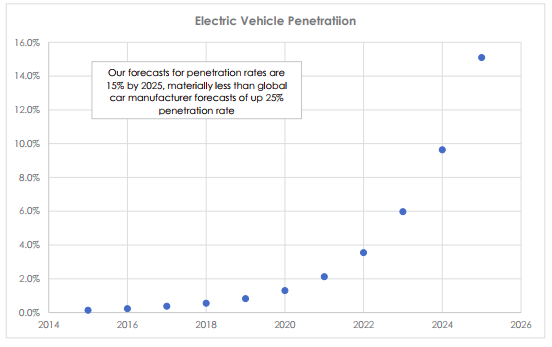

What is the likely penetration rate of electric vehicles?

Government and automobile manufacturer targets point to at least a 15% penetration rate of electric vehicles by 2025. To move to this penetration rate, electric vehicle sales need to be 50 million per annum by 2025.

“By 2030, the Volkswagen group will electrify its entire model line-up” VW’s ~ CEO, Matthias Mueller

The ramp up of electric vehicle production is unlikely to be linear. The diffusion and adoption of new ideas and new products often follows a S-shaped growth pattern, or an adoption curve.

The pattern observed is driven by contagion akin to epidemic patterns. This model has predicted the growth of many things - cable television, iPhones, LED technology, computers, investment fads, and fashion.

We expect electric car demand will follow a typical adoption curve, with growth driven initially by ‘innovators’ and ‘early adopters’ before being adapted by the ‘majority’.

"History shows that ‘growth industries’ can be a very difficult space to invest in. Growth does not always create economic value for companies. The best examples have been the automobile and aircraft industries, that have been perennial destroyers of value since their invention.” ~ Warren Buffett, American investor

How much incremental metal is required for each electric vehicle?

For the purposes of our analysis, we assume a 30-kWh battery for each electric vehicle. We highlight below the metal intensity required for each ‘kWh’ of battery power:

Nickel

Nickel content is 0.60 kg per kWh or 18kg per electric car Based on our electric vehicle growth forecasts we expect incremental high-grade nickel sulphate demand to grow by 900,000 tonnes per annum by 2025. This compares to current production of high-grade nickel of approximately 1.1 million tonnes. The nickel price required to incentivise this new production is above $US 12 per pound, almost double the current nickel price of $US6.30 per pound.

If we assume nickel rises to this price over the next few years, Australian nickel producer Independence Group (IGO) is worth up to $8.50, 70% above the current share price.

Lithium

Lithium content is currently 1 kg for each kWh, going to 0.5 kg/kwh by 20253, or 30kg per electric car. Based on our electric vehicle growth forecasts, we expect lithium demand to grow to 1 million tonnes per annum. This compares to current production of about 200k tonnes per annum. The current price of $US14,000 per tonne is elevated, and is likely to remain so for several years until supply responds to the high price.

If we assume lithium remains elevated and then declines to the marginal cost of production, our valuation of Orocobre (ORE) is worth $10.56 per share, 49% above the current share price.

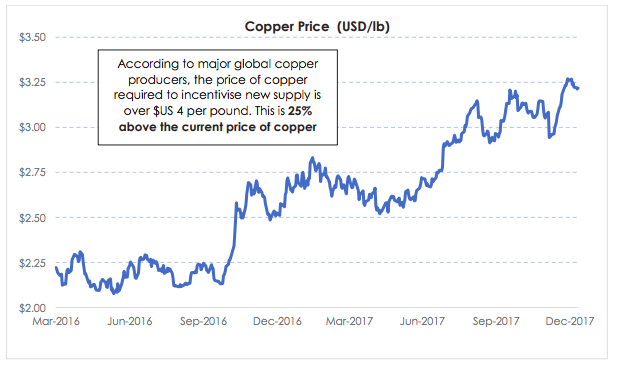

Copper

Copper content is currently 45kg per electric vehicle, or 25kg more than a conventional vehicle. Based on our electric vehicle growth forecasts we expect copper demand to grow by an incremental 1.1 million tonnes per annum. This compares to current production of about 22 million tonnes per annum. The copper price required to incentivise this new production is above $US 4.00 per pound, 25% above the current copper price of $US 3.25 per pound.

If we assume copper rises to this price over the next few years, Australian copper miner Oz Minerals (OZL) is worth $13.52 per share, 48% above the current share price.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim has 25 years’ experience in the investment and securities markets. Tim was a partner of Goldman Sachs and during his 16-year tenure at the firm had senior experience across all areas of equities investing.

5 topics

3 stocks mentioned

Tim Hannon

Managing Director

Conrad Capital Group

Tim has 25 years’ experience in the investment and securities markets. Tim was a partner of Goldman Sachs and during his 16-year tenure at the firm had senior experience across all areas of equities investing.

Expertise

Tim Hannon

Managing Director

Conrad Capital Group

Tim has 25 years’ experience in the investment and securities markets. Tim was a partner of Goldman Sachs and during his 16-year tenure at the firm had senior experience across all areas of equities investing.

Expertise

Comments

Comments

Sign In or Join Free to comment