TOL - 6th Nov, 2020

A high quality business hidden in plain sight

The Fairlight investment process is designed to identify high quality businesses, generally those with sustainably high returns on capital and a long runway for future growth. However, identifying quality alone is not enough to ensure investment success if an excessive price is paid. To tilt the probabilities in our favour Fairlight looks for underappreciated quality - businesses that have escaped the attention of the market. Often these businesses may have accounting peculiarities that obscure the true earnings power of the business, a misunderstood strategy or a large founder ownership that deters the capital market’s spotlight.

All of these characteristics are present at Morningstar, a high quality business that appears to be ignored by much of the market despite being a familiar name to nearly every financial analyst around the globe.

A high quality, long term compounder

Morningstar, founded in 1984, provides a vast array of investment related data, research and services to financial advisors and institutions. Importantly, Morningstar positions itself as an independent voice in the finance industry, providing conflict-free advice and recommendations to clients. This unique position is dependent on the trust and brand strength that has been cultivated over many decades by placing investors’ interests first and doing right by clients.

“Investors know that Morningstar will act in their best interests.” – Kunal Kapoor (CEO)

This hard-fought reputation of honesty and transparency now serves as a durable competitive advantage and is the foundation for its excellent financial characteristics:

- Over the last two decades Morningstar has increased revenues 15-fold, delivering investors a 15% p.a return since the IPO in 2005.

- 93% of revenues are recurring in nature and client retention is >95% each year. Pleasingly, Morningstar sailed through the COVID affected 2Q20 posting +6% organic growth.

- Morningstar’s products are primarily software based, meaning incremental margins are high and cash flow is consistently greater than profits given the negative working capital profile and low capex requirements.

- Management have proved themselves astute stewards of capital, consistently repurchasing shares and making value accretive acquisitions. Today, the business has a net cash balance sheet.

Ignored by sell side analysts, retail investors and passive funds

Despite Morningstar’s long track record of shareholder value creation and attractive financials, it is largely ignored by much of the market. Currently, not a single sell side analyst publishes research or earnings estimates on the business. To frame just how unusual this is; of the 8,200 listed stocks in the US with a market capitalisation >US$1bn only 24 have no sell side coverage. This lack of interest from Wall Street is driven by the Founder maintaining a 45% stake in the business (investment banks are less likely to cover a business with few prospects for M&A work) and the unusual approach to investor relations:

"Our goal is to communicate equally with all shareholders, without special treatment for large shareholders or research analysts. Instead of holding one-on-one meetings and conference calls, we’ll answer your questions in written form and make them available to all shareholders at the same time, in a way that treats everyone equally." – Morningstar Investor Relations

Given the rare focus on fairness towards smaller shareholders one might expect Morningstar to be a popular stock amongst retail investors. Yet Morningstar is ignored here too; out of 10m total account holders at the retail focussed US broker RobinHood, only 220 (0.002%) own a share of Morningstar.

Lastly, for a business that helped pioneer low cost ETF investing, Morningstar’s share register has ironically missed much of the boom in passive ownership. Currently only 1.5% of the shares outstanding are owned by passive funds. For reference this passive ownership is lower than any stock in the S&P500 and 5 times lower than the average.

Accounting obfuscates true business value

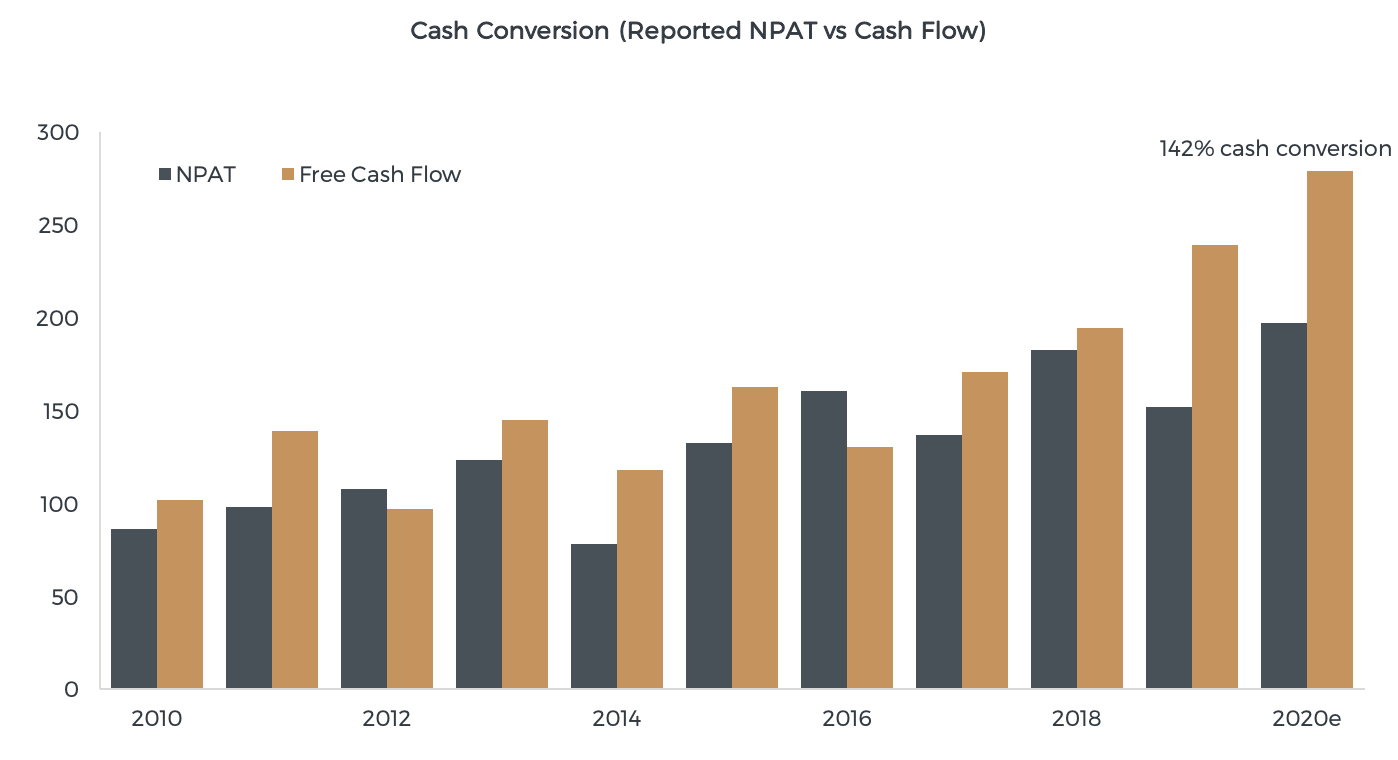

Further pushing Morningstar into investing obscurity is the perceived expensive valuation. However, our analysis indicates that the reported earnings do not align with the fundamental cash generating power of the business (see Figure 1). After making several adjustments to align accounting with reality, Fairlight believes Morningstar is trading on a very attractive multiple of cash earnings.

The Fairlight View

Whilst identifying quality in an important first step in the Fairlight investment process, to be considered for portfolio inclusion a business must also demonstrate an attractive valuation. Often this involves identifying a specific nuance or characteristic of a business that the market may have misunderstood or underestimated. In the case of Morningstar, it appears to not just be misunderstood but has slipped through the cracks of financial markets entirely.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Will is a partner and Portfolio Manager for the Fairlight Asset Management Global Small and Mid Cap Fund. He has ten years data analytics and investment experience with previous positions at EY and Evans & Partners.

Will is a partner and Portfolio Manager for the Fairlight Asset Management Global Small and Mid Cap Fund. He has ten years data analytics and investment experience with previous positions at EY and Evans & Partners.

Expertise

Will is a partner and Portfolio Manager for the Fairlight Asset Management Global Small and Mid Cap Fund. He has ten years data analytics and investment experience with previous positions at EY and Evans & Partners.

Expertise

Comments

Comments

Sign In or Join Free to comment