A megatrend shaping the world

Todd Hoare

LGT Crestone

With more than 50 per cent of the global population under 30 living in emerging market countries, the emerging market story is expected to remain a compelling investment opportunity for years to come. Strong growth in working-age populations, urbanisation and a rising middle class are expected to underpin one of the most important megatrends of the next decade.

In this article, we take a look at what will drive the emerging market story over the next 10 to 20 years, and which areas of the market are likely to provide the most compelling investment opportunities.

The case for economic growth in emerging markets

According to the International Monetary Fund, economic growth across emerging markets is projected to grow at least two percentage points faster than what we will see in the developed world for the foreseeable future (1). By 2020, this would see emerging markets account for around 40 per cent of global consumer spending (up from 20 per cent two decades earlier) (2). The region’s share of global output is set to reach 55 per cent by 2050 and its equity and corporate bond markets are on course to assume close to 30 per cent of the global market by 2030 (3).

The demographic dividend

Underpinning this is a ‘demographic dividend’ that, quite simply, the developed world, cannot match. The United Nations (UN) projects that the world’s population will increase by 41 per cent to 8.9 billion by 2050, with nearly all this growth in developing countries.

Going forward, global consumption is expected to be increasingly dominated by the emerging markets middle class. According to the Brookings Institution, in developed countries, middle-class consumption is about 44 per cent of the global total, averaging around USD 19,000 per person per annum. The growth in consumption is essentially flat at 0.5-1 per cent per annum.

In developing countries, however, consumption is growing far more rapidly at rates of around 6-10 per cent per annum, although this is from a much lower base of only USD 8,500 per person per year. This divergence means that, by 2030, global middle-class consumption could be USD 29 trillion more than in 2015—yet only USD 1 trillion of that increase will come from more spending in developed economies (4).

A combination of rising incomes and rising populations

Emerging market economies are transforming from commodity-intensive, domestic-infrastructure and export-manufacturing economies to services-based economies. Large pools of domestic savings are now able to fuel consumption as the primary driver of economic growth. This combination of rising incomes and rising populations is likely to propel strength in consumer spending on goods and services for decades to come. By 2025, emerging market consumption is expected to reach USD 30 trillion per annum, which is nearly 50 per cent of the world total (5). This is up from USD 12 trillion in 2010.

A very large and intertwined opportunity set

When it comes to emerging market consumption, it is not uncommon for investors to default to retail or ecommerce opportunities, particularly reflecting Chinese consumption. However, there is a myriad of other emerging market consumption opportunities that are prevalent for investors. These range from education (where an estimated 100 million children have never attended school) to tourism (where less than 10 per cent of the Chinese population holds a passport). Indeed, as data becomes more globalised, tech-savvy millennials are expected to open up investment opportunities not only across traditional and online retail, but also in payment gateways, healthcare, services, education and gaming. The real difficulty lies in how one allocates a finite investment dollar to a seemingly endless stream of investment opportunities.

Importantly, it is not uncommon for investment themes to be intertwined. For example, the consumption of food within emerging markets cannot be separated from a number of different yet inter-related themes, such as scarcity of arable land, water needs, changing diets, obesity and associated health care needs.

Within these themes, there are directly investable opportunities in agricultural equipment, genetics, seeds and crop protection, livestock and produce farming, water treatment, drug development and treatment, convenient eating and home delivery. Indeed, it can be an overwhelming exercise to identify all the opportunities!

The driving force behind emerging market consumption

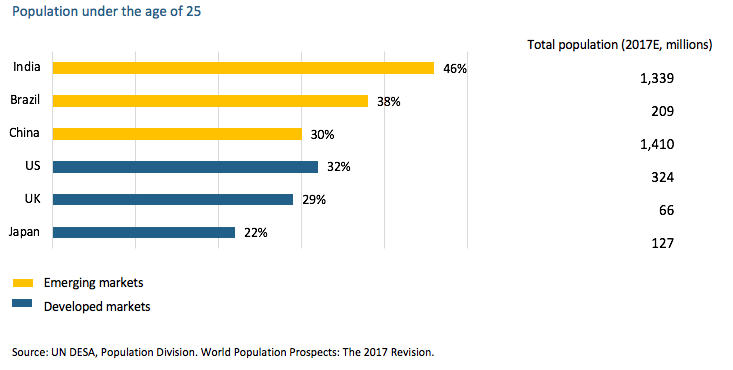

While baby boomers are generally the largest demographic in developed regions, millennials are the largest demographic in emerging markets. As a percentage of the total population, millennials already outnumber baby boomers in Brazil, China and India (6). And globally, of the approximate two billion millennials in the world (i.e. those born after 1980, or Generation Y), over 85 per cent live in emerging markets (6). This is important because it suggests that the younger cohort will be the driving force behind consumption in emerging markets.

Chinese and Indian millennials will, quite possibly, be the key driving force behind emerging market consumption over the next decade, with close to 900 million millennials in the two countries. With a median age of nearly 28 years, India is one of the youngest major economies globally and is expected to stay so in the foreseeable future (7).

As has been seen in other economies, the periods where the 18-35 working age cohort increases (or the dependency ratios fall) is usually associated with accelerating income and consumption rates. In Asia, Japan experienced this after World War II, followed by other ‘Tiger economies’ and, most recently, China. In India, its millennial population, which is predicted to be 500 million by 2020, is already the largest in the world and would represent over one third of India’s total population.

Significantly, according to the UN, India's millennial population is expected to keep growing at an average of 0.5 per cent per annum until 2032. China’s millennial population growth is already contracting, and it expects the US' millennial population to decline from 2027.

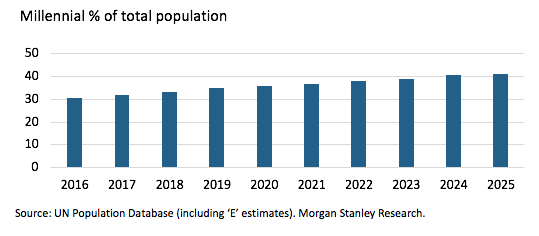

Millennials are expected to account for more than one third of the population

Where to for India?

In many respects, the experience of China’s consumption boom over the past decade provides a pathway for what we might expect from India. The impact of millennials on Chinese ecommerce growth has been very significant. China’s millennial online shopper population grew from 37 million people to 211 million people between 2007 and 2013—and although per capita income grew approximately 2.5x, per capita online spend grew more than 5x (8)

Purchasing power lags its emerging market peers

Significantly, Indian purchasing power lags its emerging market peers, with a per capita income of USD 1,700, which offers room to double by 2025. For India, this growth powerfully combines with a millennial cohort that comprises more than 60 per cent of the country’s internet base and approximately 80 per cent of its ecommerce user base.

India’s very high smartphone penetration and availability of mobile broadband infrastructure makes it a very compelling emerging market consumption opportunity—and one that is likely to drive Indian consumption patterns for decades to come.

A shift towards a consumption economy

According to a 2018 Deloitte report (9), millennials in India differ from previous generations in terms of their lifestyle choices, consumption patterns, need for convenience and brand preferences. Beyond what is needed on housing, education and utilities, incremental income is directed towards eating out and entertainment (32.7 per cent), apparel and accessories (21.4 per cent) and electronics (11.2 per cent) etc. Savings account for around 10 per cent of any incremental income, well below savings rates of the past. This indicates a shift towards a consumption economy rather than a savings economy, which was a predominant feature of the earlier demographic cohort.

Deloitte contends that as internet penetration continues to grow, online retail as a share of total retail sales is expected to increase from 3 per cent in 2017 to a still low 7 per cent by 2021. (By way of comparison, this would be less than half of China and US online sales penetration.)

Gaining exposure to the emerging market theme

We prefer active management in emerging markets, where experienced managers can address the inefficiencies that often exist in less researched markets. Such an approach is best able to efficiently access growth opportunities across a broad spectrum of emerging markets, while addressing any potential governance issues more easily than a passive approach. Further, for a number of these markets (such as India, and to a lesser extent China), accessing listed equities directly in these countries is complex or, in some cases, restricted.

__________________________________________________________________

(1) Haver Analytics: International Monetary Fund

(2) International Monetary Fund Data Mapper

(3) Credit Suisse Research Institute: Asia in Transition

(4) Brookings Institution: The Unprecedented Expansion of the Global Middle Class

(5) Brookings Institution; Kharas, Homi and Geoffrey Gertz: The New Global Middle Class: A Cross-Over from West to East

(6) UN Population Division

(7) Central Intelligence Agency: The World Factbook

(8) Morgan Stanley: The Next India

(9) Deloitte: Trend-setting millennials: Redefining the consumer story

Never miss an update

Stay up to date with the latest news from Crestone Wealth Management by hitting the 'follow' button below and you'll be notified every time we post a wire.

Want to learn more about Crestone Wealth Management? Hit the 'contact' button below to get in touch with us or head to our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Todd joined Crestone in June 2017 and he is responsible for global equities investment and advice. He has over 15 years experience covering fixed income, Australian and global equities both domestically and internationally.

1 contributor mentioned

Todd Hoare

Head of Equities

LGT Crestone

Todd joined Crestone in June 2017 and he is responsible for global equities investment and advice. He has over 15 years experience covering fixed income, Australian and global equities both domestically and internationally.

Expertise

Todd Hoare

Head of Equities

LGT Crestone

Todd joined Crestone in June 2017 and he is responsible for global equities investment and advice. He has over 15 years experience covering fixed income, Australian and global equities both domestically and internationally.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management