A stock to own in a rising rate environment

The trend in global interest rates appears to be upwards in the foreseeable future driven largely by the US Federal Reserve’s stated interest rate normalisation strategy. Whilst the Australian economy is growing at a slower rate than the US at present and may not be as suited to rising interest rates, global financial markets are inter-connected and the upward trend in interest rates has also started in Australia and is likely to continue following the US lead for the same reason. Interest rate movements will clearly impact on ASX listed sector and stock performance looking forward, some more than others. In this article we look at which sectors are likely to out and under-perform, and we highlight one stock in particular from the DMX Capital Partners portfolio which is well placed to outperform in a higher interest rate environment.

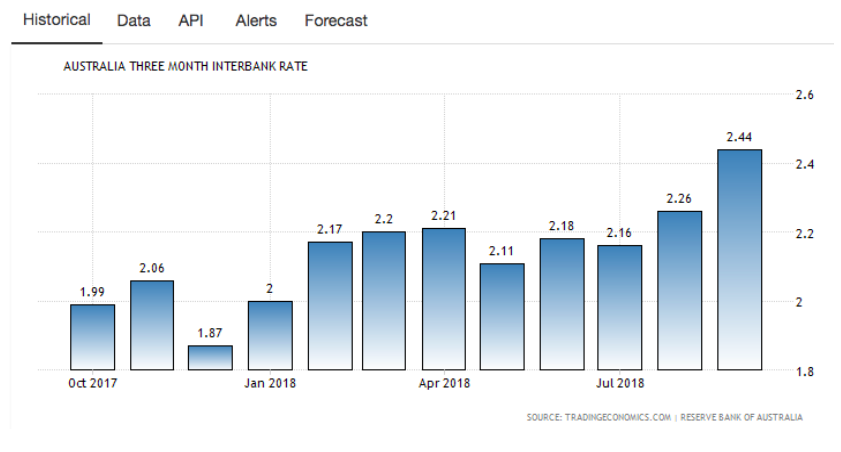

Australian interest rates finally on the move…

Global interest rates have been trending upwards in recent months and the Australian bank bill swap rate has been following suit in recent months albeit at a slower rate moving from its low almost a year ago of 1.87% to the current 2.44%. This 57 bp move is relatively small in an historical context, and current rates are still well below historical averages, but we believe the change in trend is meaningful…

Are higher interest rates positive or negative for markets in general?

The answer is, it depends.

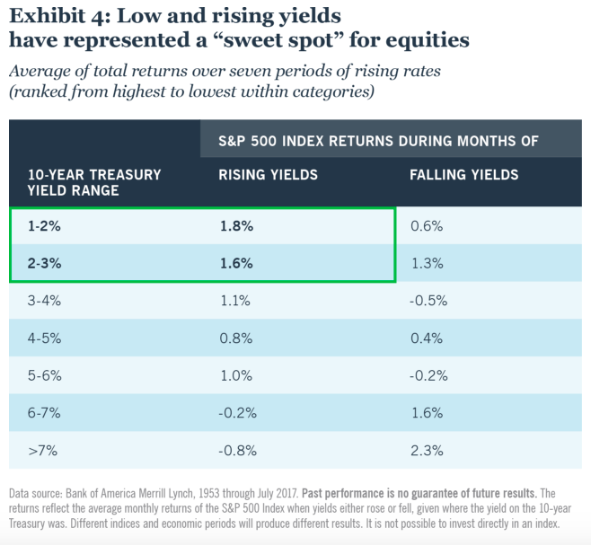

Higher interest rates are definitely not all doom and gloom for equity markets despite the negative messages the media keeps focusing upon. As shown below, S&P 500 returns have actually been very strong during months when yields rose whilst the 10-year Treasury yield remained below 6%. Historically, there has been a sweet spot in a rising but low yield environment in which higher interest rates are perceived by the equity market as a positive signal regarding current and future economic growth. Until recent days, the US equity market has reflected these supportive economic conditions. The Fed funds rate is currently only 2.25%, which is obviously well below the 6% level which becomes more problematic for equity markets, and the equity bull market has, until recently, continued unabated in the face of rising but low yields.

How will rising interest rates affect sector performance looking forward?

Whilst we are very much bottom up stock pickers, we also spend time ensuring we are aware of major global and domestic economic trends, and their implications at a sector and stock level, and interest rate trends are a major input when valuing stocks.

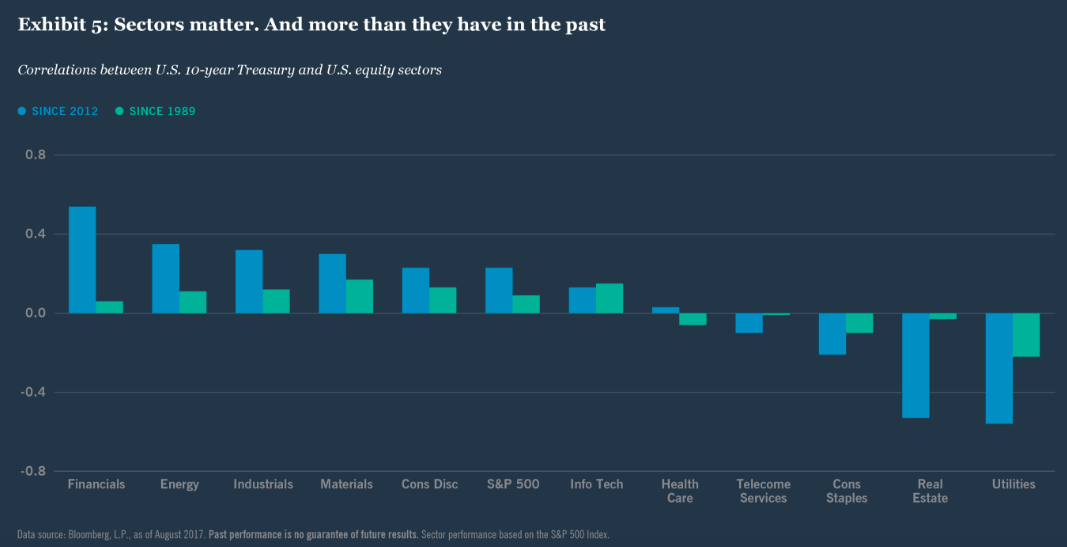

In terms of how the various sectors react to higher interest rates historical stock performance date provides a picture of what has happened in previous rate tightening cycles and may provide some guidance looking forward. The best available data comes from the US market…

As the chart above shows, the sectors which have historically outperformed are:

- Financials – As yields increase so do the margins in the financial sector.

- Energy – A cyclical sector which benefits from strong economic growth.

- Industrials – A cyclical sector which benefits from strong economic growth.

- Materials – A cyclical sector which benefits from strong economic growth.

And the sectors which have historically underperformed are:

- Utilities – A sector which is highly sensitive to interest rate movements given the generally high levels of debt and the Discounted Cash Flow basis of all investments in the sector.

- Real Estate – Another highly sensitive sector for the same reasons.

- Consumer Staples – Consumer staples are generally considered a defensive sector and defensive sectors are likely to underperform during periods of strong economic growth.

Which stocks are likely to outperform in a rising rate environment?

We are not economists and do not profess to know where interest rates will move from here but we believe if the risk to interest rates remains on the upside looking forward, this is likely to create great stock picking opportunities for savvy investors.

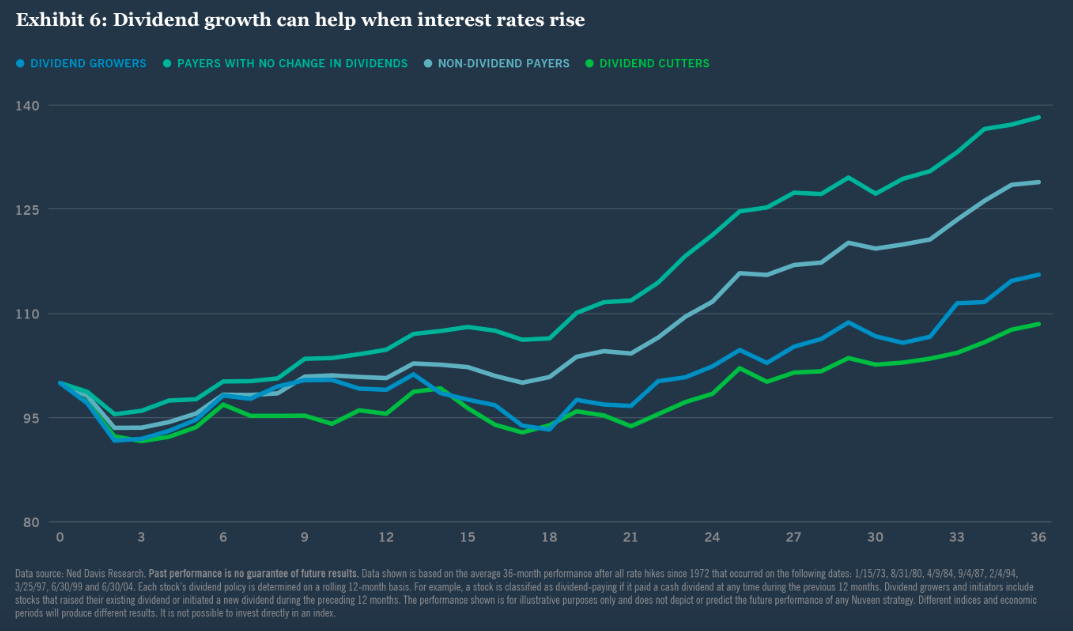

As Warren Buffet famously said “it’s only when the tide goes out that you see who’s swimming naked”. Companies which carry a lot of debt are obviously far more vulnerable to rising interest rates than companies with strong balance sheets. When we invest in listed smaller companies we like to know that most if not all of the company’s EBIT will go to equity-holders rather than debt-holders who by their nature will take an increasing share of EBIT during periods of rising interest rates.

The US historical data provides compelling reinforcement of this principle as show in the chart below – companies which increase their shareholder returns in the form of rising dividends during periods of rising interest rates, tend to strongly outperform, and vice versa…

This is not rocket science – investors who are receiving a growing dividend yield during times of higher interest rates, which normally occurs during periods of higher inflation, know that their real income is at least being protected, if not increased.

Bringing it all together = the right sector + the right business model

We are comforted to know 80% of the DMX Capital Partners equity portfolio is currently invested in dividend paying companies from which we expect growing dividends looking forward.

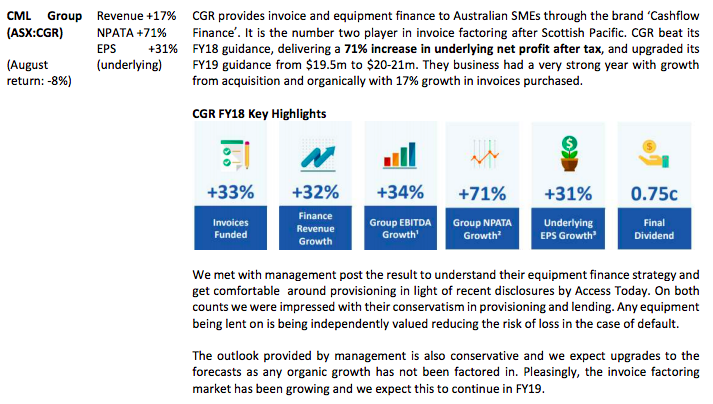

As noted above, the financial sector historically has been a beneficiary of rising interest rates. In the DMX Capital Partners portfolio we believe there is one financial stock that is very well positioned to continue to grow its earnings and thus pay out growing dividends looking forward and thus worthy of mention: CML Group (ASX:CGR).

By way of background, here is our recent summary on the company after it’s FY18 results were announced…

CML Group is well placed to grow its earnings in a rising interest rate environment as it has the ability to pass on any increase in interest rates to its customers - and given CGR’s financial assets are greater than its financial liabilities, there is, over time, a positive impact on profits. CGR also has recourse to the end debtor, the financing client and a debtor insurance policy, making it somewhat insulated against any emerging default risks resulting from higher interest rates.

CGR trades on c.10x FY19 profit, whilst Scottish Pacific (ASX:SCO), its larger listed competitor, has recently received a private equity takeover offer implying a~16x FY19 acquisition multiple.

So this is fast growing, undervalued. high quality smaller company which we expect to pay out a growing stream of dividends in the face of higher interest rates looking forward. We believe the odds of long term outperformance are in our favour.

CONCLUSION: With 80% of DMX Capital Partners’ portfolio in companies which pay growing dividend streams, we believe we are well positioned to benefit from a rising interest rate cycle should that eventuate. And CML Group is a stand out example from our portfolio of a company which we believe can benefit from a rising rate cycle and will pay higher dividends in the coming years to investors as a result.

REFERENCES

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

DMX Asset Management Limited is an investment manager focussing on nano and micro-cap value opportunities on the ASX.

1 topic

1 stock mentioned

DMX Asset Management Limited is an investment manager focussing on nano and micro-cap value opportunities on the ASX.

Expertise

DMX Asset Management Limited is an investment manager focussing on nano and micro-cap value opportunities on the ASX.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management