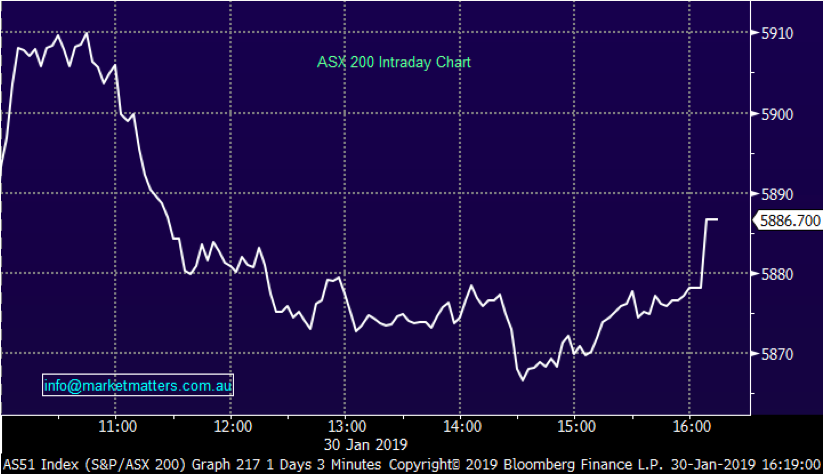

A tired looking market gives up morning's gains

The local market once again failed around the 5900 level as it continues to struggle to find the next leg higher. The market jumped out of the blocks early to crack the key 5900 level before giving back all of the gains before lunch and chopping around par for the afternoon. A flurry of buying on the close did help the index close just in the black. Financials dragged again today, with the market keeping one eye on the final Royal Commission report due out on Monday. Local inflation data saw 4th quarter CPI slightly beat estimates with +0.5% quarter on quarter, yet the market didn’t seem too phased although the AUD did see a nice rally against the green back.

A downgrade by Air New Zealand (ASX: AIZ) sunk the travel names today with another revision to guidance citing recent booking trends as the reason for the 20% downgrade to pre-tax earnings. Auckland International (ASX: AIA) down -3.88%, Qantas (ASX: QAN) off -5.09% and Flight Centre (ASX: FLT) giving up -2.13% Iron ore names continued yesterday’s pop with another strong performance today. Short sellers seemed to cause a flurry of buying early in the day before each of the names edged lower throughout the day, although still finishing strongly higher. We sold Rio Tinto (ASX: RIO) in the Platinum Portfolio today, which reached an early high of $89.65 / +7.3% before easing to close at $87.30 / +4.51%. Credit Corp (ASX: CCP) sunk on some poor analysts updates despite what seemed like a decent result yesterday. The stock gave back yesterday’s gains and some in today’s session. Newcrest (ASX: NCM) jumped with the gold price, but also a strongly quarterly with gold production up 19% and costs falling. The stock was up 3.57% to $24.34.

Overall, the ASX 200 closed up 12points or 0.21% to 5886. Dow Futures are currently trading up 42pt.

ASX 200 Chart

ASX 200 Chart

CATCHING OUR EYE

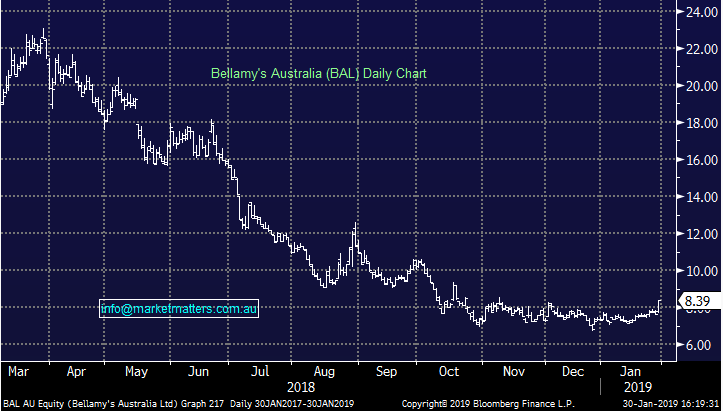

Broker Moves; Bellamy’s is the place to be for your China exposure, and not A2 Milk according to Morgan Stanley today. The broker moved to positive on BAL while moving to negative on A2M given the divergence in performance of each over the past 12 months.

ELSEWHERE:

- Fortescue Upgraded to Buy at HSBC; PT A$5.75

- Fortescue Downgraded to Hold at Morgans Financial; PT A$5.45

- Fortescue Downgraded to Sell at Morningstar

- Credit Corp Downgraded to Sell at Morningstar

- Credit Corp Downgraded to Hold at Baillieu Holst Ltd; PT A$23.90

- Credit Corp Cut to Neutral at Evans and Partners; PT A$22.95

- Credit Corp Downgraded to Neutral at JPMorgan; PT A$23

- GPT Group Downgraded to Sell at Morningstar

- AMP Downgraded to Hold at Morningstar

- TPG Telecom Upgraded to Hold at Morningstar

- Rio Tinto Upgraded to Neutral at Evans and Partners; PT A$70

- Spark NZ Downgraded to Sell at Goldman; PT NZ$3.65

- Resolute Mining Downgraded to Underperform at RBC; PT A$1.10

- Regis Resources Downgraded to Hold at Bell Potter; PT A$5.35

- Redbubble Upgraded to Add at Morgans Financial; PT A$1.27

- Bellamy’s Rated New Overweight at Morgan Stanley; PT A$11

- Blackmores Rated New Underweight at Morgan Stanley; PT A$104

- A2 Milk Co Rated New Underweight at Morgan Stanley; PT A$9.60

G.U.D. Holdings (ASX: GUD) $11.10 / -9.02%; The automotive parts business printed profit of $29.3m for the 6 months to December 2018, up ~$1m yoy, but fell well short of the markets expectations. With the consensus of analysts pricing a full year profit of $63.5m, it would now take a blockbuster second half to achieve market expectations, particularly given they often have a first half skew to earnings. GUD has been on a big acquisition spree which is yet to drop down into earnings however the CEO is standing firm, looking for further expansion

Whilst the automotive business is growing, the water products company slumped in the first half in tough conditions caused by the drought. Recent acquisitions are yet to bear fruit and the market is (understandably) getting nervous around integration risk. We do see the water business adding more to the second half, however the automotive side may continue to struggle. The stock set new 52-week lows today. Often seen as a barometer of the local economy, hopefully the soft result isn’t a sign of things to come in reporting season.

G.U.D. Holdings (ASX: GUD) Chart

Zip Co (ASX: Z1P) $1.135 / -2.58%; followed Afterpay’s (ASX: APT) efforts with new records of their own at the 2nd quarter update released today. The alternative credit provider noted that platform had surpassed 1mil users in the period, while also posting record revenue at $19.2m, up 28% on the first quarter.

The records really shouldn’t come as a surprise with Q2 including the Christmas shopping period, as well as a number of retailers launching on the platform, both of which helped the company add $4.6m profit. Despite all the positive trends, the Zip share price has fell today after opening strongly higher. It seems shareholders are looking to take profits off the table, but the announcement does give credit to the business model and the longer term trajectory of the company. We like Zip, but not one for us at this stage. Risks remain around regulation and credit markets, particularly with some of the profits driven by falling bad debts – this can’t remain forever.

Zip Co (ASX: Z1P) Chart

Never miss an update

Stay up to date with the latest news from Market Matters by hitting the 'follow' button below and you'll be notified every time I post a wire.

Want to learn more about Market Matters? Hit the 'contact' button to get in touch with us.

Market Matters publishes daily market reports and sends SMS alerts when we transact on our portfolio. To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and Partners heading up a team that manages direct domestic and international equity & fixed-income portfolios for wholesale investors.

2 stocks mentioned

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 2 standout ASX names for FY26

Livewire Markets

Equities

Buy Hold Sell: The best and worst performers of FY25

Livewire Markets

Equities

The critical mineral no one's watching (and our #1 ASX small cap pick)

Seneca Financial Solutions

Property

The property opportunity offering 7% yield

Livewire Markets