A wild ride for inflation expectations

Inflation risk is an important consideration for fixed income investors and something we aim to mitigate through active management. Rising inflation has a detrimental impact on bond prices as the value of their future coupon payments, along with the value of their principal investment are eroded.

Forecasting inflation

Inflation expectations are an intangible concept, an inexact science of forecasting and extrapolating data derived from a number of sources. Much the same as meteorologists forecasting the weather, there are many measures and signals to consider, some more telling than others, to help form a view. Inflation expectations can be derived from surveys, by drawing conclusions from actual data and by looking at what is implied by market pricing – such as the price of inflation linked bonds and ‘breakeven inflation’. In other words, the level of inflation that would make an investor indifferent (or breakeven) between owning nominal and inflation linked bonds.

While in normal market conditions these methods generally provide consistent results, the extreme market conditions in March saw these assumptions challenged.

What was the market signalling in March?

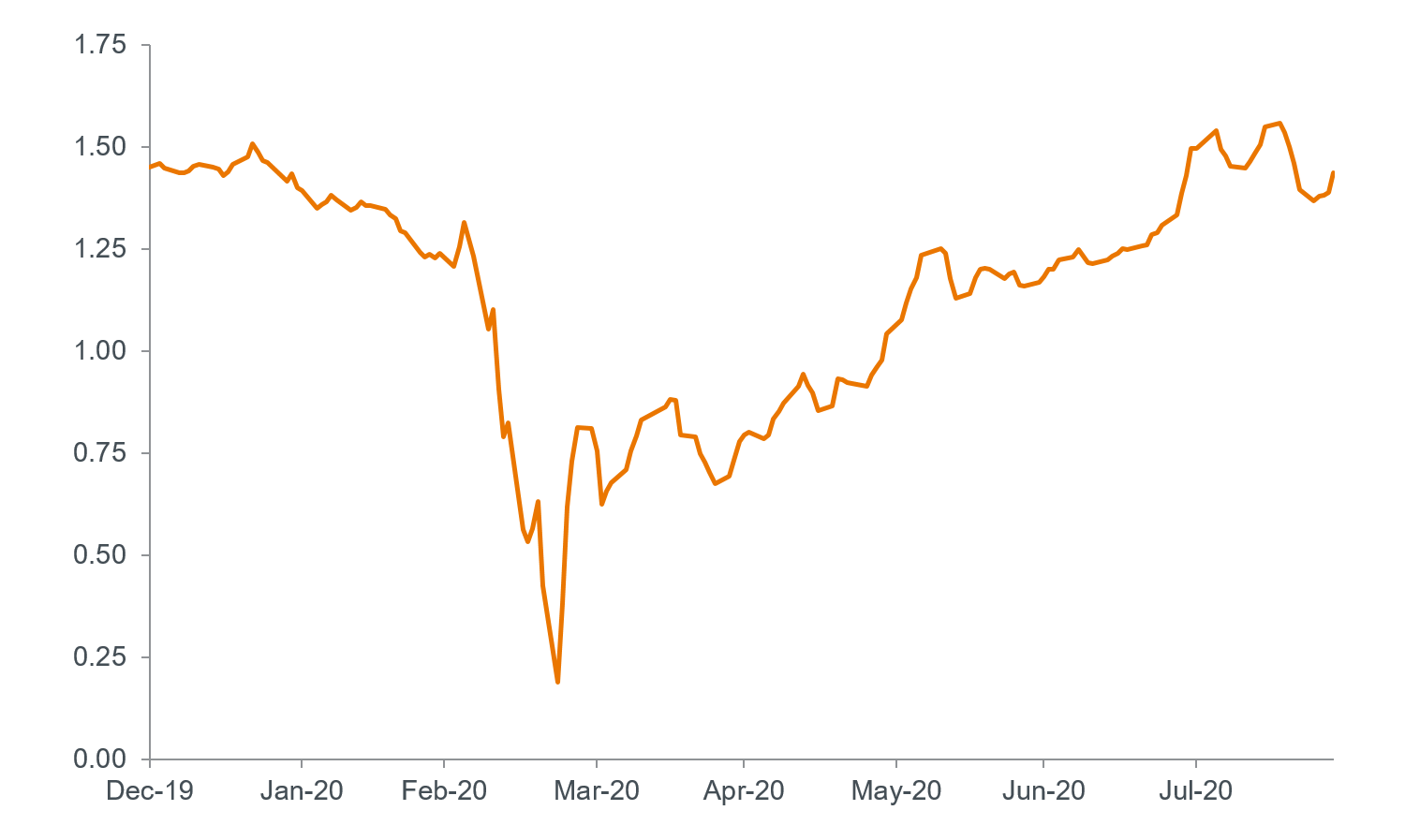

Through the severe market dislocation, inflation expectations, as measured by the yield of Australian Government inflation linked bonds with a maturity of 2035, suggested inflation would be practically non-existent over the next decade. But how accurately did this indicate inflation expectations, and, what were the factors that caused this dislocation?

Chart 1: Australian 15-year breakeven inflation rate (%)

Source: Bloomberg. Australian 15-year breakeven inflation rate (31 December 2019 – 28 August 2020).

Rather than indicating that inflation would be close to zero for the next decade – as panic selling commenced across asset classes and liquidity quickly dried up, inflation linked bonds were just one of the many assets caught up in the sell-off.

We believe a survey would not have resulted in the same insights, which is why it is valuable for us to have a range of measures to rely on.

In our view, three key factors drove the volatility in inflation expectations – each of them an extreme event in their own right:

- A once in one-hundred-year economic shock, where markets priced in negative oil prices, resulting in a strong disinflationary signal.

- A six standard deviation event in inflation expectations, driven purely by technical factors (which has never occurred in Australian inflation linked bonds previously).

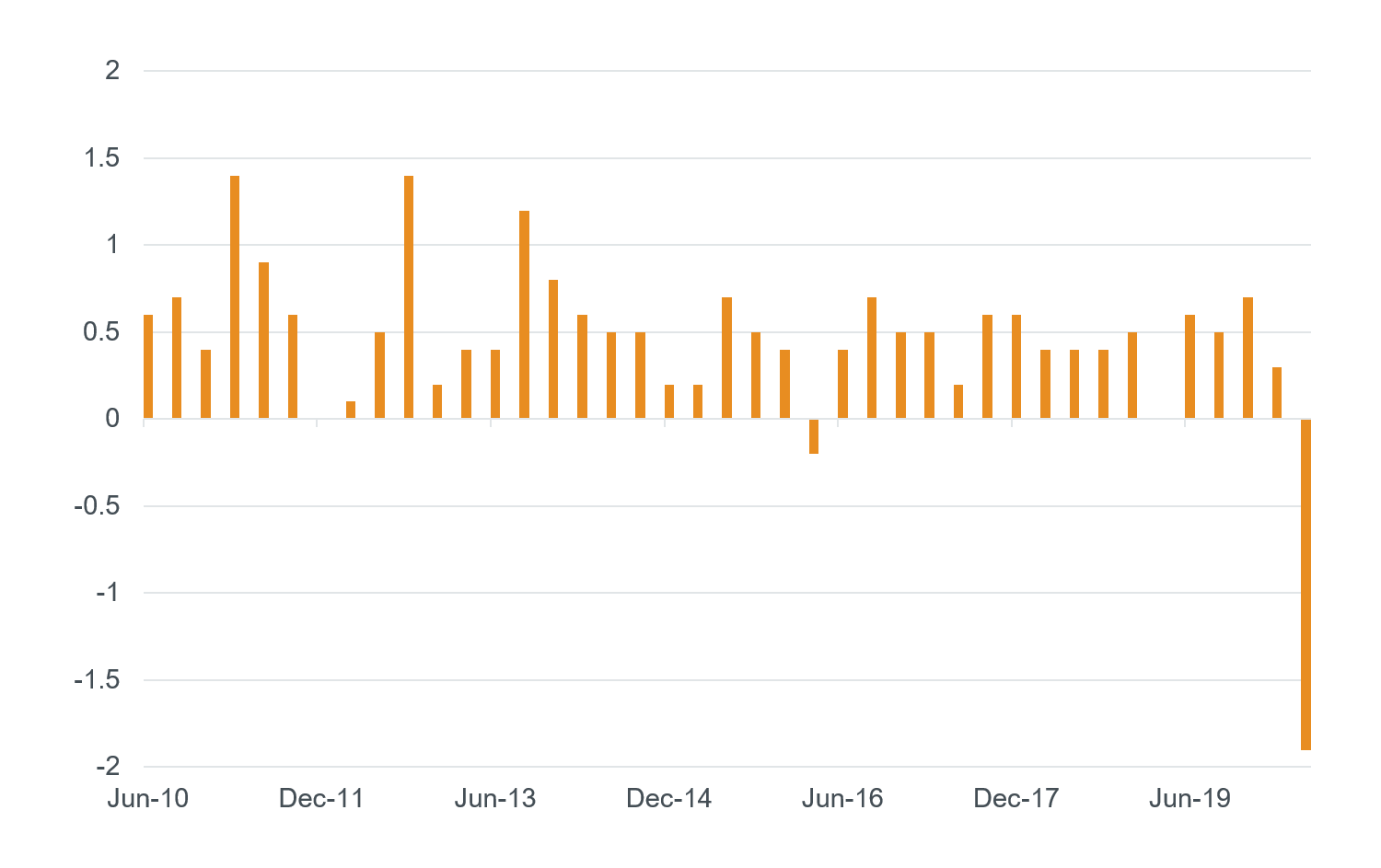

- A rapid recovery like no other, at a time when we’ve had one of the worst inflation readings in history – a quarterly change of -1.9%.

Chart 2: Consumer Price Index

Source: Australian Bureau of Statistics. As at 29 July 2020.

What is the opportunity for investors?

The opportunity presented to investors during this scenario was not so much about needing to take a view on inflation over the next decade, but rather it was about realising that the cost of inflation protection at that time was very low (and at times almost free). While we are currently in a recession and expect inflation to remain quite low for the next two to three years, buying inflation linked bonds means these assets should outperform nominal government bonds if and when inflation starts rising, especially when taking a 10-15 year view.

Learn more

Stay up to date with all our latest views but clicking the follow button below, and you'll be the first to read all our wires.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jay Sivapalan is Head of Australian Fixed Interest and a Portfolio Manager at Janus Henderson Investors. He contributes to both interest rate and sector strategies employed within portfolios and has 22 years of financial industry experience.

........

This content has been created by Janus Henderson Investors (Australia) Institutional Funds Management Limited (AFSL 444266, ABN 16 165 119 531). This content shall not in any way constitute advice or an invitation to invest. It is solely for information purposes. This content does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

No warranty or representation is given that as to the accuracy or completeness of the contents and no responsibility can be accepted by Janus Henderson Investors (Australia) Institutional Funds Management Limited for any action taken on the basis of this content. All opinions and estimates expressed in this content are subject to change without notice. Janus Henderson Investors (Australia) Institutional Funds Management Limited is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect.

.png)

1 topic

.png)

Jay Sivapalan is Head of Australian Fixed Interest and a Portfolio Manager at Janus Henderson Investors. He contributes to both interest rate and sector strategies employed within portfolios and has 22 years of financial industry experience.

Expertise

Jay Sivapalan is Head of Australian Fixed Interest and a Portfolio Manager at Janus Henderson Investors. He contributes to both interest rate and sector strategies employed within portfolios and has 22 years of financial industry experience.

Expertise

Comments

Comments

Sign In or Join Free to comment