Afternoon note: Markets hit on virus concerns, although buyers again prevalent into weakness (FPH, JIN)

While it was clearly a risk off session following the -730pt slide by the Dow Jones on Friday, the selling wasn’t aggressive and Futures have rallied strongly into / after the close of cash trading to be up around the daily highs. The rise in COVID-19 cases has clearly accelerated which is generating a lot of negative headlines internationally, particularly in the US, and although I never want to be accused of being a ‘Trump mouthpiece’, the rise does correlate with increased testing. In any case, the stats are concerning, hence the market is on edge, however I get the feeling that the easy call of cases rising / sell equities will prove too simplistic this time around. As we suggested this morning, the stock markets largest fear is often uncertainty and if the COVID-19 journey while tough and unpredictable doesn’t throw up too many nasty surprises it might just ”get used to it” in its own optimistic way, an outcome we’ve seen before and will see again.

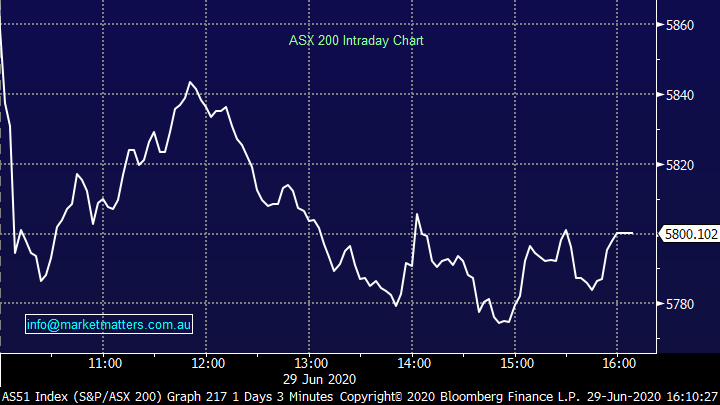

It was a choppy session overall today with early weakness bought into only for the sellers to get the upper hand by midday. Property stocks hit hardest, although a number of them traded ex-dividend making the Energy stocks the weakest overall. While the cash market closed at 5800, futures have rallied since. Asian markets all traded lower today while US Futures have been in and out of positive territory, currently trading flat.

Overall, the ASX 200 down -90pts / -1.51% today to close at 5815 - Dow Futures are trading flat

ASX 200 Chart

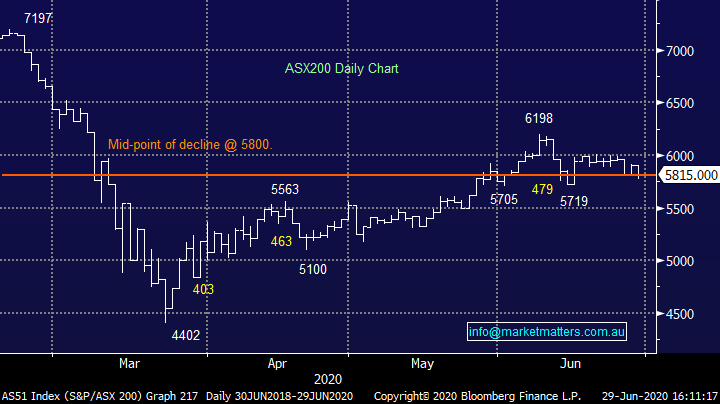

ASX 200 Chart

CATCHING MY EYE:

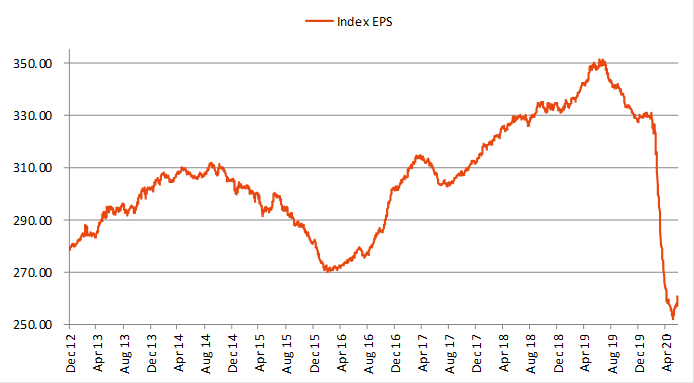

Earnings Expectations: This chart caught my eye this morning which looks at index earnings per share (EPS) estimates, in other words, what analysts expect the index as a whole to earn on a per share basis. The large deterioration in EPS expectations has underpinned the rise in valuations, hence the growing calls that the market is very overpriced given prevailing conditions. That argument relies on analysts getting earnings right, and from what I can tell, analysts have cut hard on the back of companies pulling guidance (i.e. companies don’t have a handle on what it means, let along analysts!) The chart below shows a slight uptick here which is stemming from a number of larger caps coming out with reinstated guidance which has been better than feared (retailers an example). In any case, we can clearly see that EPS expectations are bearish, but are showing some tentative signs of bottoming / moving higher.

Source: Shaw and Partner

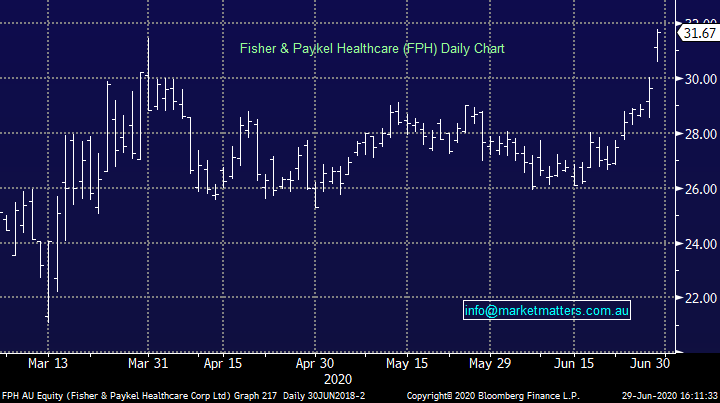

Fisher & Paykel (FPH) +6.88%:After a period of consolidation, FPH traded strongly higher today + broke out of its range on the back of a strong full year update (31st March yearend). Revenue was up 18% on last year to $NZ1.26b, ahead of the $NZ1.24b expected while after tax profit was also a beat at $NZ 287m v $NZ 277m expected by the market. They put in all the usual caveats about uncertainty for FY21 then guided to $NZ1.48b revenue dropping to $NZ 340m in after tax profit, which was in-line with current expectations.

Fisher & Paykel Healthcare (FPH) Chart

Jumbo Interactive (JIN) -13.23%: Hit hard after resuming from a prolonged suspension following a new 10-year reseller agreement with Tabcorp, the terms mean more for TAH, less for JIN hence the sell-off in JIN (TAH added +0.91%). It seems to me there was a lot of back and forth here in a deal that is important for JIN and while it provides some certainly, the terms are clearly less attractive that the mkt implied. Hard to get excited about JIN.

Jumbo Interactive (JIN) Chart

BROKER MOVES:

· Altium Rated New Buy at Jefferies; PT A$40.66

· 3P Learning Raised to Overweight at Morgan Stanley; PT A$1.10

· Galaxy Resources Cut to Neutral at Credit Suisse

· QBE Insurance Raised to Buy at Bell Potter; PT A$9.70

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and Partners heading up a team that manages direct domestic and international equity & fixed-income portfolios for wholesale investors.

........

Any advice provided is of a general nature only.

2 stocks mentioned

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

21 ASX stocks that should be on your radar

Livewire Markets

Equities

Wisetech tanks 17% on earnings miss but margins shine

Livewire Markets