Why we still like OZ Minerals, Beach Energy and Wisr

After a very bullish session yesterday that saw the ASX 200 put on more than 150pts, the market has given back ~50% of those gains today as attention turned back towards the virus and the concerning case counts coming our of Victoria. The trend sets up the chance for more aggressive lockdowns across a state that accounts for about 23% of Australia’s GDP. Today it was healthcare and IT that felt the brunt of the selling, CSL, Ramsay (RHC) & Resmed (RMD) down 3.62%, 2.43% & 2.49% respectively. On the flipside, Energy the standout with Beach (BPT) putting out some good production numbers, Harry covers off on those below while we also take a look at Oz Minerals (OZL) after a good June quarter update that saw them deliver operationally across all metrics + they upgraded guidance for copper/gold production & (much) lower costs.

Around the region, Asian markets were mostly lower, down around -0.50% although China kept its head above water up +0.3%. US Futures were higher earlier although tapered off into the close of our session, trading around flat at the moment. The AUD remained strong, and is now trading US71.65…strength here implies we should not turn bearish equities despite todays fall.

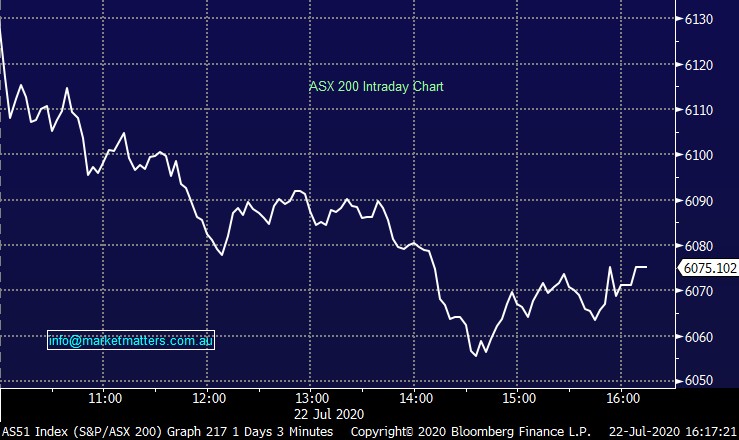

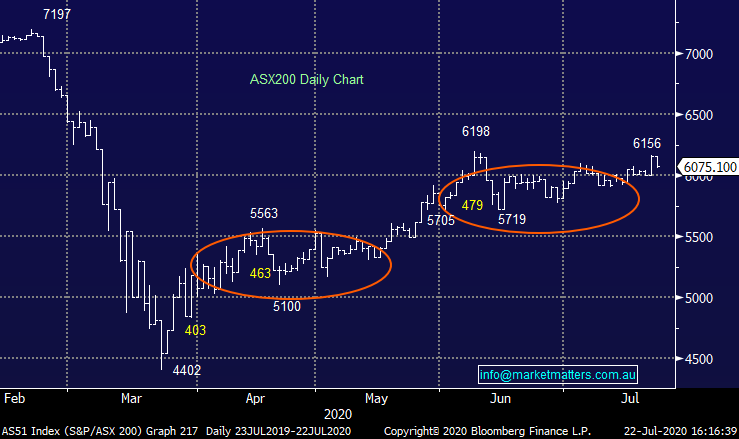

Overall, the ASX 200 lost -81pts / -1.32% to close at 6075. Dow Futures are trading up +39pts / +0.15%

ASX 200 Chart

ASX

200 Chart

CATCHING MY EYE:

Virus Headlines: The virus is dominating headlines again with Australia chalking up our worst daily case count yet underpinned by a +484 jump in Victoria. While the market was soft today, I thought it worthwhile revisiting some points we made early in the month about our interpretation of why the market was unlikely to fall out of bed as was the case in March. This still holds true.

1. The initial death rate was expected to be somewhere around 2-3%, however as more and more testing happens, and the case count goes up, the rate of deaths is going down.

2. Markets have a fear of the unknown and while there are plenty of things that we don’t know about COVID-19, we do know that reduced social interaction / lockdowns work. While we doubt that we’ll go back to widespread lockdowns due to the economic implications, instead outbreaks will be managed at a more local level as is the case in Victoria, having the knowledge that containment works is a comforting backstop for the market.

3. Globally we are now more set up to handle the virus, from tracking technologies to hospital beds, regime’s around containment, isolation, hand washing, sanitation / general hygiene, even handshaking is now taboo. The world is now a lot more prepared than it was in March.

4. Growth in case numbers does not scare the market, uncertainty does. The market bottomed on March 23, the day domestic lockdowns were imposed. At that time, global cases were 300,000, now cases are above 11m.

5. Stimulus was quick and large. During the GFC, domestic stimulus equated to about 4% of GDP, COVID-19 stimulus now accounts for more than 13% of GDP.

6. Markets had gone more than 10 years without a big shakeout. During that period, large, leveraged positions build up in the system and a shock like the one we’ve just had created mass / forced liquidation of leveraged risk positions. Funds implode which amplifies moves in the market. We’ve spoken to many trading desks that had large liquidations to manage. These positions are largely gone and it takes years for them to build up again.

While we believe the virus will remain a major market influence until a vaccine is discovered, we don’t think March volatility will be repeated.

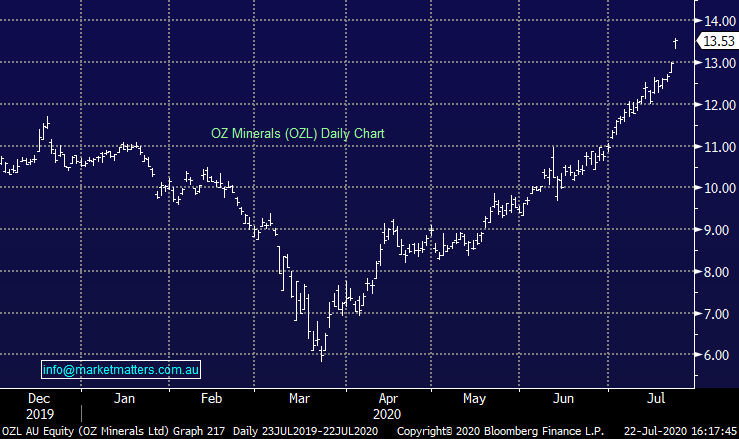

Oz Minerals (OZL) +4.24%: The rally continued for OZL today on a strong set of June quarter production numbers, the short take is that operations are running well with FY20 guidance upgraded on better copper and gold output from their Australian assets. Future growth comes from continued ramp up at Carrapateena which is progressing well while financials are very sound (net cash $15m +$400m facility). All in all, OZL has have been delivering since 2015 so todays’ very good quarterly and upgraded guidance should be seen as the continuation of a very impressive trend. We remain overweight this stock in our growth portfolio.

Oz Minerals (OZL) Chart

Beach Energy (BPT) +4.71%: Out with quarterly production this morning and broadly speaking production was as expected at 26.7mmboe for the year with the final quarter seeing 6.8mmboe, slightly lower than the previous quarter. As with all energy names in the current climate, price received saw a big hit in the quarter, falling to $A44.90/bbl, down 26% on the third quarter which had a similar effect on revenue. The company is reviewing it’s 5 year plan given the hit to energy markets which will likely see growth projects put on hold. Capex for the full year came in below guidance after the company intentionally limited spend into the end of the year. They will release an updated plan at the full year earnings result at 17 August. We own Beach.

Beach Energy (BPT) Chart

Wisr (WZR) +8.33%: A smaller cap finance company we’ve written about a few times which did well today. We’ve been seeing good demand for this across the desk and a stock that can rally +8% in a weak market is worth keeping an eye on. A good speccy, too small for the current MM Portfolios however this is the sort of stock that will be in the Emerging Companies portfolio soon to be launched.

Wizr (WZR) Chart

BROKER MOVES:

- Silver Lake Cut to Sell at EL & C Baillieu; PT A$1.83

- Silver Lake Raised to Outperform at Macquarie; PT A$2.60

- Perseus Cut to Underperform at Macquarie; PT A$1.25

- Credit Corp Raised to Overweight at JPMorgan; PT A$20

- Perseus Cut to Underperform at Credit Suisse; PT A$1.30

- Saracen Mineral Cut to Sell at EL & C Baillieu; PT A$4.71

- BHP Group PLC Cut to Neutral at Citi; PT 1,800 pence

- Saracen Mineral Cut to Hold at Argonaut Securities; PT A$5.45

Register for a free trial to Market Matters

At Market Matters, we write a straight-talking, concise, twice daily note about our experiences, the stocks we like, the stocks we don’t, the themes that you should be across and the risks as we see them.

To sign up for a free trial to Market Matters, leave your email and phone number through the 'CONTACT' button below

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

........

Any advice provided is of a general nature only.

3 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment