Afterpay's opportunity much bigger than the market realises

Joe Magyer

Lakehouse Capital

It’s hard to be indifferent about Afterpay Touch, which is one of the fastest-growing yet most divisive companies listed on the ASX. The market’s reaction this morning to the announcement of first-half results was no exception with the shares off by around 9% at lunchtime despite continued torrid growth.

As usual, the market’s initial response was caught up on how results stacked up relative to consensus expectations, and some of the headline numbers were already in the market via a business update in January. Instead of rehashing those points, here’s what strikes me as the key takeaways from today’s report:

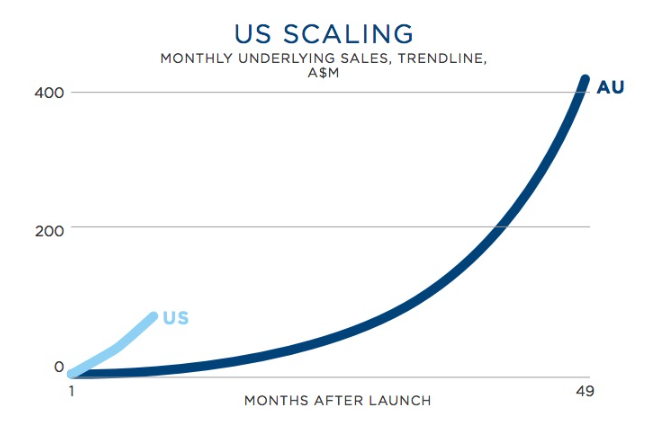

1. The US launch is going great guns. Afterpay expects that it will reach more than 1 million active users in the US by the end of March, which is far ahead of the Australian experience (which itself was wildly successful). This chart showcasing the trajectory of underlying sales by market sums it up it nicely:

Source: Afterpay Touch investor presentation 26 February 2019.

No doubt the US push will hit some bumps along the way as competitors and regulators take increasing notice. More capital might also be required to help support growth. Still, I can think of worse things than raising additional equity for a network-powered business where success begets success, and while regulatory risk remains real, it also comes with the territory of investing in disruptive companies. Plus, as the recent experience with regulators in Australia and New Zealand highlights, not every brush with regulators proves a showstopper.

2. Late fees and gross losses are moving in the right direction. Afterpay probably silenced some critics today by revealing that late fee income as a percentage of Afterpay’s total statutory income shrank from 22.5% to 17.6%. Gross losses as a percentage of underlying sales also fared well as they shrunk from 1.6% to 1.1% on a pro-forma basis. Combined with other gives and takes, the net transaction margin stayed flat year-on-year at 2.3% on a pro-forma basis, which is striking considering the capping of late fees and rapid scaling into the US and new verticals in the Australian market.

3. Afterpay UK is set to launch soon. The company plans to launch Afterpay into the UK during the current half, which could provide another serious leg up of growth as Statista scopes the UK as the third-largest ecommerce market in the world behind the US and China. Helping the business get a running start will be Urban Outfitters, as the US-based retail giant who helped propel the impressive US launch has committed to be a launch partner into the UK. Watch this space.

Our view is that, while Afterpay Touch is a business and stock with a wide range of outcomes, the market is underestimating the scope of Afterpay’s opportunity here and abroad.

According to Australia Post, online shopping in Australia only amounted to 8% of total traditional retail sales at the end of 2017, while Goldman Sachs estimates that the US online fashion market in 2017 was around 20 times the size of Australia’s. Meanwhile, Afterpay has also successfully expanded into physical stores and new verticals such as travel and healthcare.

On top of new markets, channels, and verticals, Afterpay has call options around new products for both merchants and consumers. For example, it isn’t hard to picture Afterpay creating an ad business at some point given that Afterpay is now already the second-largest traffic driver behind Google in Australia. We also think Afterpay could leverage its strong brand equity to follow the lead of US rival Affirm by offering savings accounts to its users, around 85% of whom plug debit cards into their Afterpay accounts.

Many investors are skeptical of how Afterpay would navigate an Australian recession, which is a valid concern considering the business model has not been tested across an economic cycle. The business is no longer a purely Australian story, though, and grows more global by the day. For that matter, because the payback periods on Afterpay purchases are so short, the company can quickly adapt to a softening environment by tightening its standards, simultaneously reducing default rates and gross leverage.

Again, this is a business with a very wide range of outcomes, and they don’t all have happy endings. Still, we think the business could grow faster and for longer than many expect, and as patient investors with a tolerance for a good deal of volatility we are willing to wait and see what happens. How about you?

The Lakehouse Small Companies Fund owns shares of Afterpay Touch. Both Joe Magyer and the Lakehouse Global Growth Fund owns shares of Alphabet, the parent company of Google.

Never miss an update

Stay up to date with the latest news from Lakehouse Capital by hitting the 'follow' button below and you'll be notified every time I post a wire.

Lakehouse’s unique investment approach focuses on key themes of Intellectual Property, Network Effects and Loyalty. Find out more here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Joe is the former co-founder. Please visit and follow Donny Buchanan and Nick Thomson for the latest insights around Lakehouses’s unique concentrated investment approach that focuses on the key themes of Intellectual Property, Network and Loyalty to find the best long-term opportunities.

1 topic

1 stock mentioned

Joe Magyer

Former Co-Founder

Lakehouse Capital

Joe is the former co-founder. Please visit and follow Donny Buchanan and Nick Thomson for the latest insights around Lakehouses’s unique concentrated investment approach that focuses on the key themes of Intellectual Property, Network and Loyalty...

Expertise

Joe Magyer

Former Co-Founder

Lakehouse Capital

Joe is the former co-founder. Please visit and follow Donny Buchanan and Nick Thomson for the latest insights around Lakehouses’s unique concentrated investment approach that focuses on the key themes of Intellectual Property, Network and Loyalty...

Expertise

Comments

Comments

Sign In or Join Free to comment